OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: 2025 Looks Like a Generally Stress-Free Year In Cannabis Credit

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 07/05/2024

Viridian Capital Chart of the Week: 2025 Looks Like a Generally Stress-Free Year In Cannabis Credit

-

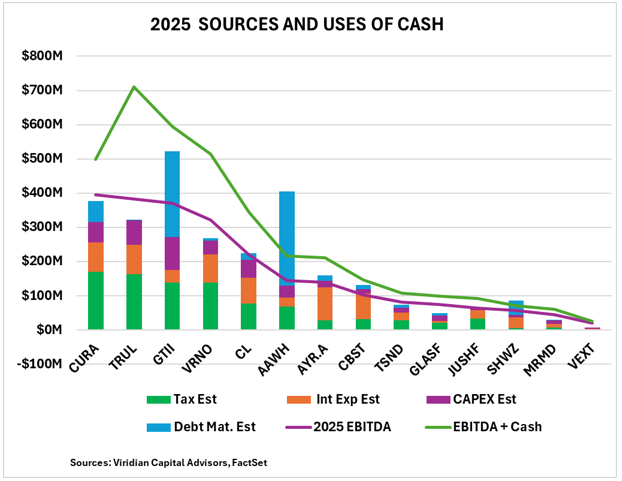

- The Viridian Chart of the Week explores the ability of major MSOs to cover their 2025 cash requirements with internally generated cash flow.

- The purple line shows consensus analyst estimates for 2025 EBITDA with the highest EBITDA companies on the left. The green line shows the sum of 2025 EBITDA and current cash.

- The bars in the graph show critical uses of cash, including taxes, interest expense, CAPEX, and debt maturities.

- Taxes for 2025 are conservatively estimated, assuming 280e lingers on through the year. The aggregate tax expense for the group of $911M is approximately $500M higher than our estimates of taxes without 280e.

- Most of the companies on the graph have EBITDA that covers or nearly covers all of their cash requirements.

- There are several exceptions and conditions, however.

- Green Thumb (GTII: CSE) has a $250M 7% Senior Secured Note that matures in May 2025. GTI’s cash on hand, in addition to its projected EBITDA, should be enough to retire the debt. Nonetheless, we expect the company to refinance the debt and do not anticipate it having much difficulty doing so. GTI has consistently topped the Viridian Capital Credit model rankings as the strongest credit in the industry, and its existing bonds are trading near par.

- Ascend Wellness faces a slightly more challenging situation with the maturity of its $275M 9.5% Senior Secured Term Loan in August 2025. The loan will clearly need to be refinanced as the company’s cash flow and cash on hand will not be sufficient to retire the issue. The issue is quite significant at nearly 140% of Ascend’s market cap. Ascend’s debt is trading in the context of a 96-98 bid/asked spread, which suggests the market is not overly worried about the company’s ability to extend or refinance the issue.

- One significant condition of the graph is that several of the companies have substantial debt maturities to negotiate in 2024 that are not included in the 2025 maturities in the graph. For example, TerrAscend still has over $100M of debt maturing in 2024 that needs to be extended or refinanced. Jushi has approximately $80M of remaining 2024 maturities, and $29M of Schwazz’s $42M is already due.

- Debt investors can look forward to a relatively stress-free 2025 in preparation for a more tense 2026 with more sizeable and more challenging debt maturities. If S3 remains on track, we expect to see a re-opening of cannabis capital markets to facilitate refinancings.