OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

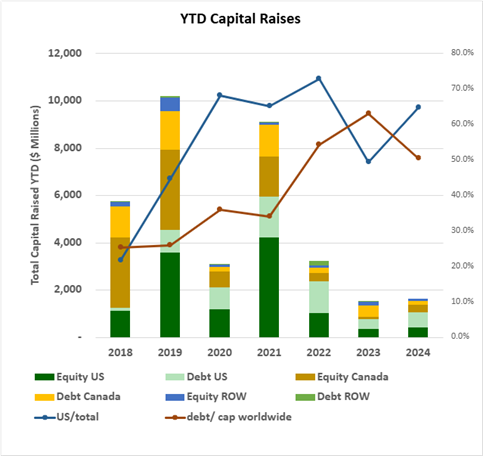

- YTD capital raises totaled $1,838.47, up 18.1% from the same period in 2023. Debt as a percentage of capital raised dropped to 56.1% from 62.7% in the previous year on a worldwide basis. The U.S. bucked this trend with 68.1% of capital raised in debt compared to 54.6% in 2023.

- U.S. raises accounted for 68.8% of total funds, up from 49.5% at the same point in 2023. Raises from outside Canada and the U.S. represented 5.2% of the total funds raised, in line with the average of 5.9% for the six previous years.

- YTD raises by public companies accounted for 75.3% of total funds, the highest since 2021.

VIRIDIAN INSIGHTS

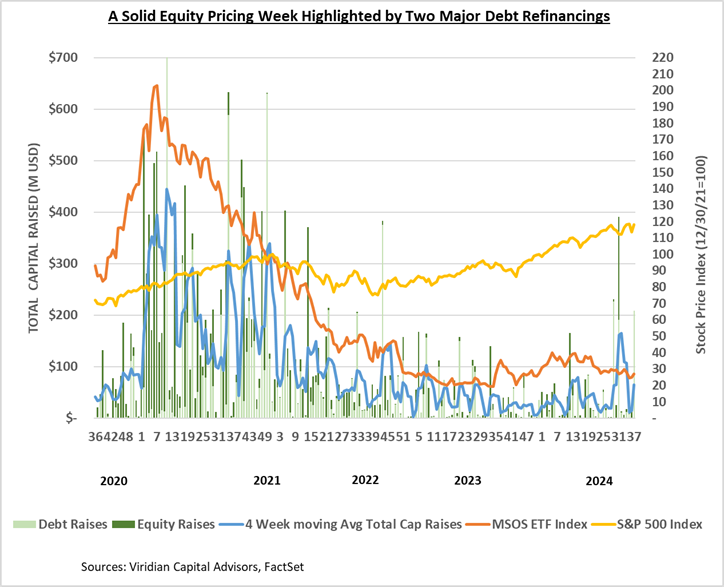

- THE CANNABIS DEBT CAPITAL MARKET IS HOT!

- This week’s two refinancing deals by Green Thumb (GTII: CSE)(GTBIF: OTCQX) and Acreage Holdings (ACRG.A: CSE)(ACRDF: OTCQX) demonstrate the breadth of the debt capital markets:

Green Thumb

- We are not surprised by the execution on the $150M GTI refinancing. As the highest-ranked credit in the Viridian Credit Tracker model, we always thought GTI would achieve an attractive rate on its refinancing. At 500bps over SOFR, the initial rate of 10.31% is equivalent to a fixed rate of 9.06% using the 5-year SOFR swap curve.

- The fixed equivalent rate on the GTI loan represents a 560bps point spread to treasuries, which is still relatively high given our perception of GTI as a solid B.B. credit. The BofA BB US High yield index of effective yield is now at 5.32%, representing a spread of about 186 basis points over Treasuries. This gap demonstrates that cannabis debt still has a significant amount of potential tightening, particularly on the best credits like GTI, Trulieve, and Verano.

- The all-bank investor syndicate is the first syndicated bank loan in cannabis and a precursor to future debt developments, including a high-yield bond market for cannabis companies.

Acreage Holdings

- The $58.5M Acreage Holdings refinancing tells quite a different story about the cannabis capital markets: even a credit that we rank near the bottom of our rankings can get refinanced today.

- The terms were relatively ugly. A 13.5% coupon with a 10-point OID on a 3-year maturity produces a yield of 17.9%, nearly 1445 basis points over the equivalent Treasury, well over the classic 1000bps definition of distressed debt.

- Acreage ranks as #28/31 on the weekly credit ranking of MSOs contained in the GIVING CREDIT WHERE CREDIT IS DUE section below, a level generally indicative of distress. The ranking is likely to improve based on greater liquidity from the financing, and the implicit support of Canopy is a credit factor that doesn’t factor into our numerical scoring.

- Even though the 17.9% rate seems painful, it pales in comparison with the pain that AYR had to endure to close their refinancing earlier in the year. AYR gave up a 13% coupon with a 20-point OID plus around 25% of the company’s equity. Without the equity, that equated to over 22%, but with the equity, we calculated a rate well over 30%. We believe AYR is (and was) a significantly better credit, which demonstrates how far the market has come.

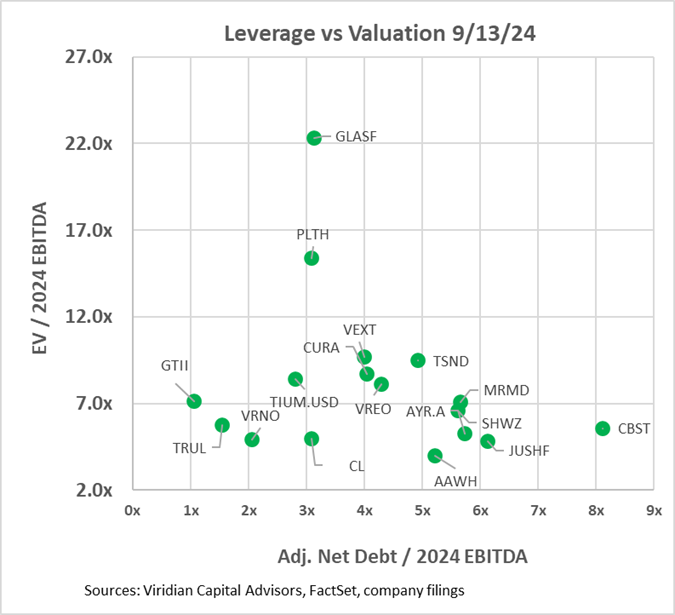

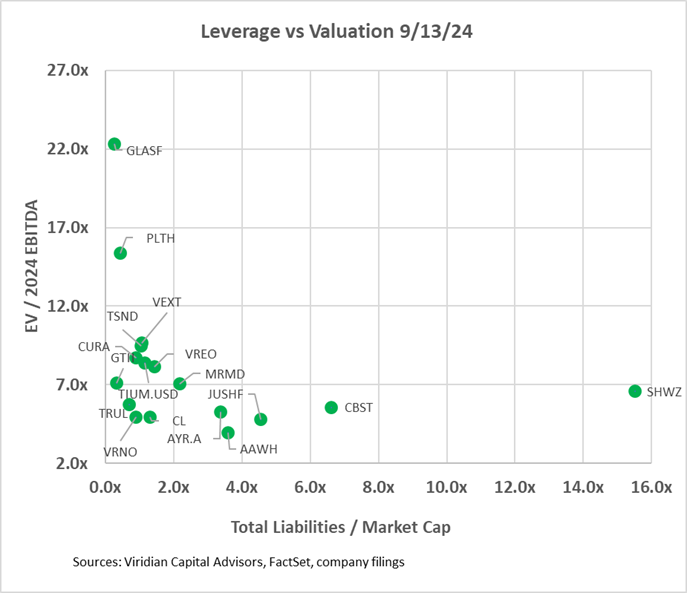

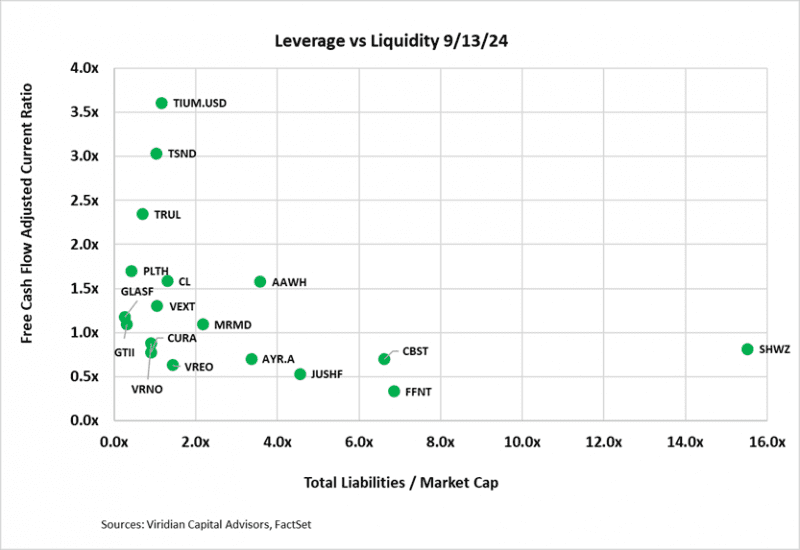

- MSO FINANCIAL STRENGTH BY PICTURES

- The three graphs below seek to map the financial options available to eighteen of the largest MSOs based on their Valuation, Leverage, and Liquidity.

- In the first graph, E.V./ 2024 EBITDA is plotted against Adjusted Net Debt/ 2024 EBITDA. In calculating Adjusted Net Debt, we make several key assumptions: 1) Leases that are included on the balance sheet are considered debt. We view most leases in the cannabis space as equivalents to equipment loans or mortgage loans. While it is true that a lease default does not necessarily trigger a cascade of events leading to bankruptcy, the distinction is often meaningless in cannabis due to the mission-critical nature of many long-term leases. 2) We consider any accrued taxes (including uncertain tax liability accounts listed as long-term liabilities) in excess of the most recent quarterly tax expense to be debt.

- The graph shows that thirteen of the eighteen companies have net debt / 2024 EBITDA over 3x, which we view as the cutoff of sustainability in a 280e world. We view 4x as sustainable in a post-280e environment, and ten companies are now over that threshold.

- Companies like Green Thumb (GTII: CSE), Trulieve (TRUL: CSE), and Verano, with less than 2x Debt / EBITDA and relatively low E.V./ 2024 EBITDA valuation multiples, are good candidates for debt-funded Equity repurchases and/or acquisitions using relatively high percentages of debt financed cash consideration.

- Companies like TerrAscend, with relatively high leverage but also high valuations, should look to complete acquisitions using their stock as consideration.

- Finally, companies like Cannabist (CBST: Cboe) and 4Front, with low valuations but excessive debt loads, are probably best served by asset sales.

- The second graph looks at leverage through the lens of total liabilities to market cap. We believe this is the single best measure of leverage because it is a direct reflection of the market’s assessment of the value of a company’s assets in excess of its liabilities and is sensitive to changes in market perception of a company’s future.

- On the bottom left are companies with low valuation multiples but also less than 2x total liabilities to market cap. The group includes GTI, Verano, Trulieve, and Cresco. Companies in this quadrant are right to consider stock repurchases or using cash in acquisitions. They can afford some additional debt and can take advantage of the ongoing dislocation in equity prices.

- In the middle, between 2x and 5x total liabilities/market cap, we see Ascend, AYR, Jushi, and MariMed. Each of these has more than 4x debt/ EBITDA, which is borderline in terms of sustainability, even in a non-280e world. However, each also has significant upside catalysts that could mitigate or exacerbate the excess leverage. For example, Jushi is levered to potential adult rec developments in Pennsylvania and Virginia, and AYR has significant Florida torque.

- On the right lies Cannabist and Schwazze. We applaud Cannabist management. They have seen the writing on the wall: too levered to issue equity or debt, its only option was asset sales. Its exit from Florida and agreements to sell out of Arizona and portions of Virginia are further ratification of this. The debt market recognized the company’s progress this week with significant credit spread tightening.

- At the top left are companies with high valuation metrics and low leverage. These companies should look to do an equity issuance depending on their positioning in the liquidity graph below.

- The third graph introduces the free cash flow adjusted current ratio liquidity measure into the mix. Companies with less than 1x on this measure will likely have to raise capital next year. Surprisingly, eight of the companies fall into this bucket. This graph also breaks the sector into three distinct groupings. The bottom left group has low leverage but also modest liquidity. Some of the companies, including Verano, MariMed, and Cresco, have sufficient but not comfortable levels of liquidity, while others, including Curaleaf, Verano, and Vireo, are below the critical 1x liquidity line. TerrAscend’s recent refinancing has moved the company into a comfortable liquidity position. Companies on the lower right generally have constrained liquidity and high leverage, a potentially dangerous combination in a capital-constrained environment.

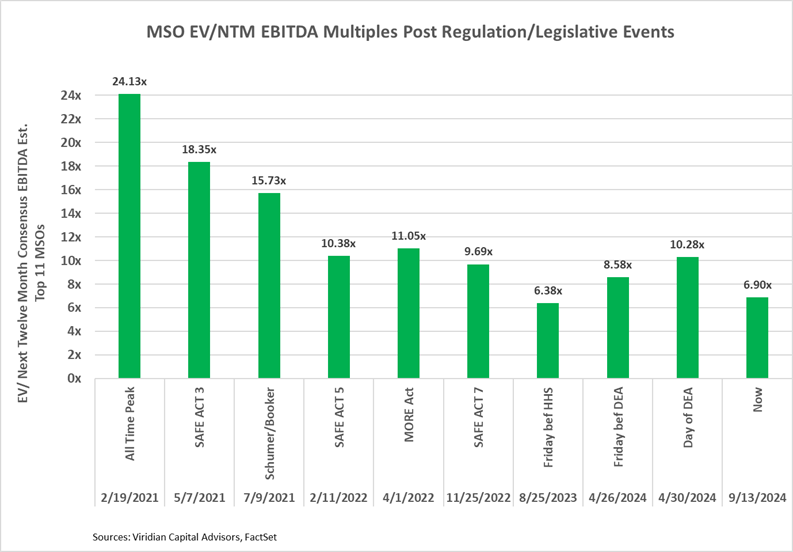

- MASSIVE UPSIDE STILL EXISTS FOR INVESTORS WILLING TO WITHSTAND ELECTION-YEAR VOLATILITY

- We continue to believe that at current levels, U.S. MSOs have enormous upside potential. The graph below shows the multiples reached after a number of past legislative/regulatory events. It makes clear that a doubling of prices is a reasonable assumption. We recommend a balanced portfolio that leans toward the companies in the top half of the Viridian Credit Tracker model ranking.

- Notably, the discussion of SAFER has begun again. We hesitate to put much stock in such debate in an election year. Still, the ongoing talks do point to another critical catalyst, one that many institutional investors believe is more important than S3.

-

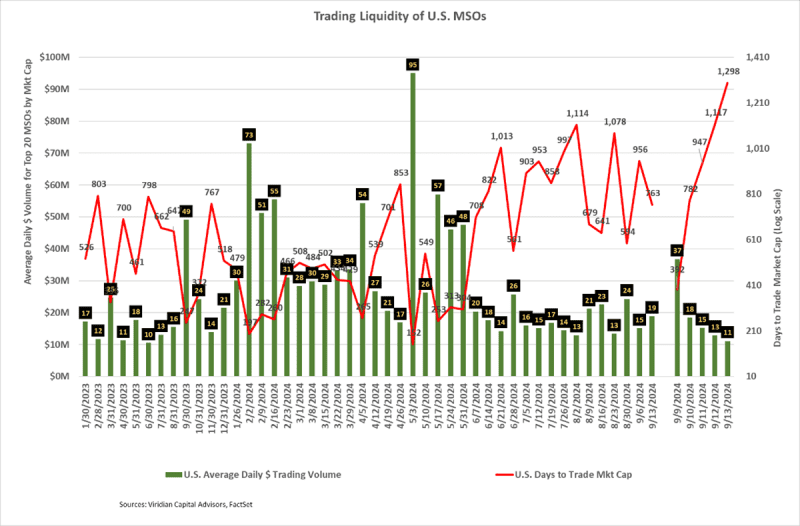

- CANNABIS STOCK LIQUIDITY IS TRENDING LOWER

- The average daily dollar volume of $19M for the week ended 9/13/24 is close to the $18M trailing 12-week average. Volume trailed off as the week wore on, ending at an $11M trading day on Friday the 13th.

- The Days to Trade Market Cap (DTTMC) series depicts the number of days it would take to trade the market cap of a stock or group of stocks. The current DTTMC of 763, a significant improvement over last week’s reading of 956, implies that an investor who acquired a 5% position in the stock, assuming he wanted to be less than 25% of the average daily dollar volume, would require 153 days to trade out of his position.

- As the presidential election cycle accelerates, we expect more trading volume and price volatility.

- CANNABIS STOCK LIQUIDITY IS TRENDING LOWER

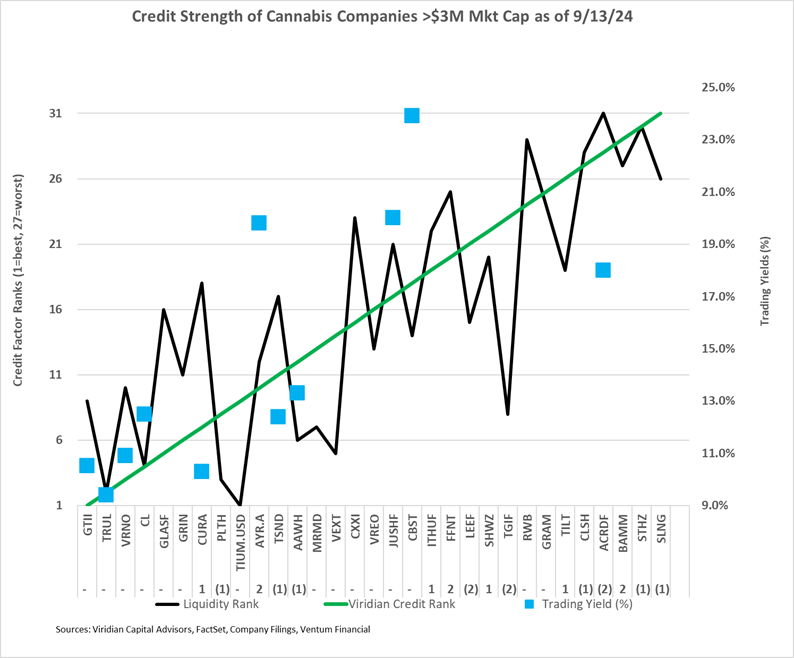

- GIVING CREDIT WHERE CREDIT IS DUE

- The chart below shows our updated 9/13/24 credit rankings for the 31 U.S. cannabis companies with over $3M market cap. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement.

- The blue squares show the offered-side trading yields for each Company. Trading yields have declined significantly since the HHS rescheduling announcement. We are expecting the round of recent refinancings to re-rate the landscape of cannabis debt. Specifically,

- We still believe that both Cannabist and AYR have significant potential for appreciation. AYR just obtained a Virginia license and has one of the highest Florida torques.

- The new Acreage deal at approximately 18% seems a bit rich to us, but it largely depends on the degree to which Canopy can and will support the company in the future.

- CANNABIST (CBST: Cboe)(CBSTF: OTCQX) ANNOUNCES DETAILS OF FLORIDA DIVESTITURES

- Cannabist announced a definitive agreement with an unnamed “leading MSO” for the sale of its Lakeland cultivation facility for $11.4M in cash. The asset includes a 40k+ square foot cultivation facility. The price represents about $285 per square foot, a level that strikes us as relatively low, given the importance of additional cultivation in driving the ability to add stores in Florida. Industry people who looked at the facility have told us that it may need retrofitting and that it is not big enough to move the needle for a major acquirer.

- It is interesting to speculate who the buyer might be. We would have thought that the buyer would want to announce the deal themselves and might even be required to announce a significant purchase like this. Verano and AYR both seem out because they are busy building their own additional cultivation capacity. The most likely candidate is GTI, which is building out stores in Florida and needs additional cultivation to continue its growth. But wouldn’t GTI want to or have to announce such a deal? Perhaps it is a private company that is not subject to any disclosure requirements.

- In a second transaction, Cannabist agreed to sell to a J.V. of Mint Cannabis and Shango 14 dispensaries, two cultivation and manufacturing facilities, and the company’s MMTC license for total gross proceeds of $5M, payable $3M in cash and $2M in notes. The transaction value seems relatively low. If all sales proceeds were credited to the 14 dispensaries, it would equate to about $357K per dispensary, which is only a bit higher than it would cost someone to bring up a new dispensary. That neglects any value for the cultivation/manufacturing facilities.

- One twist to the transaction is the fact that Cannabist is taking back the Mint/Shango license and has plans to divest the license to a third party. Does this mean that the Lakeland Transaction is with an MSO that is not in Florida currently and will, therefore, need the extra license?

- All in all, we read these transactions as positive for Cannabist. They are shedding money-losing operations, significantly improving liquidity, and focusing their attention on markets where the company is better positioned.

- Cannabis equities (as measured by the MSOS ETF) ended up 7.46% for the week.

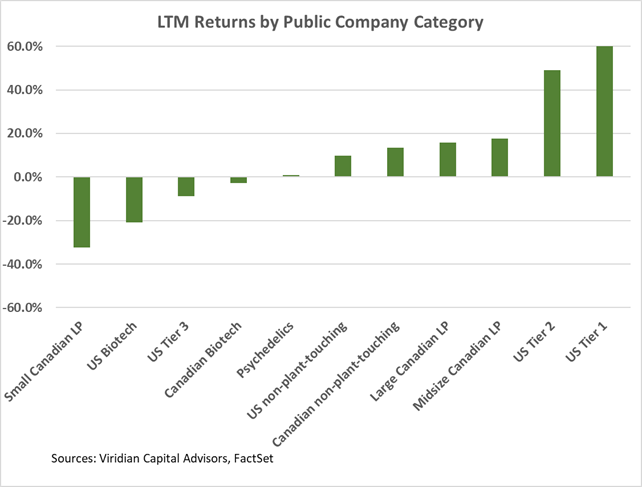

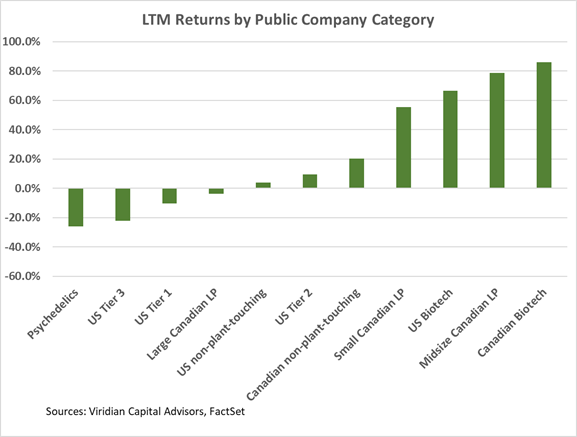

Trailing 52-Week Returns by Public Company Category:

-

- LTM returns are now being calculated in reference to the peaks achieved after the HHS announcement on 8/30/23 and are accordingly coming up quite negative.

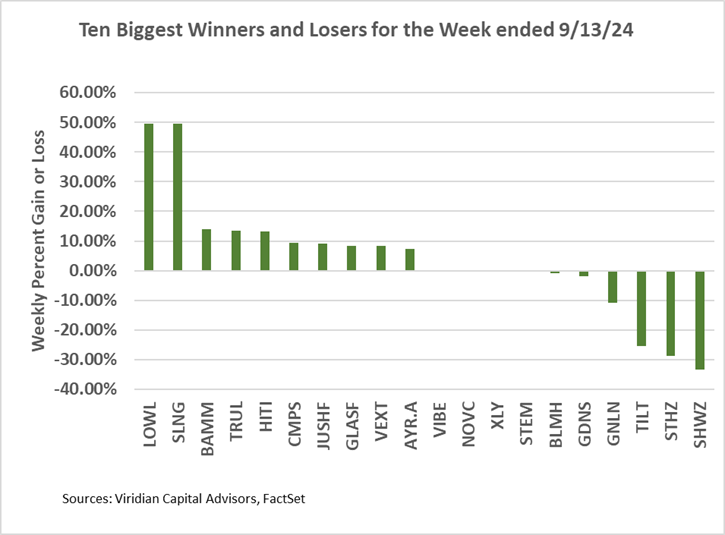

Best and Worst Performers for the week ended 9/13/24:

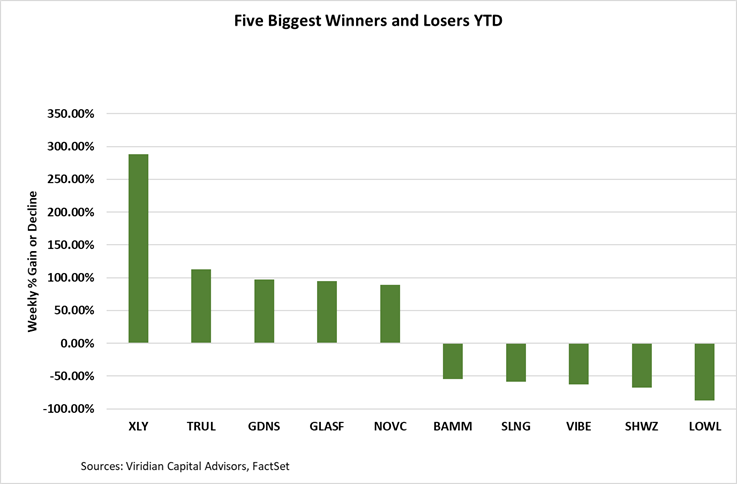

- Schwazze (SHWZ: CSE) was the week’s loser, down more than 33%, albeit on extremely light volume, as the company has still not filed its June 10q, awaiting restatements from the accounting review.

- Tilt (TILT: Cboe) was another big loser, down 25.3%. We saw no news to account for the decline.

- Both Slang (SLNG: CSE) and Lowell (LOWL: CSE) were up nearly 50% in a classic dead cat bounce fashion.