OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

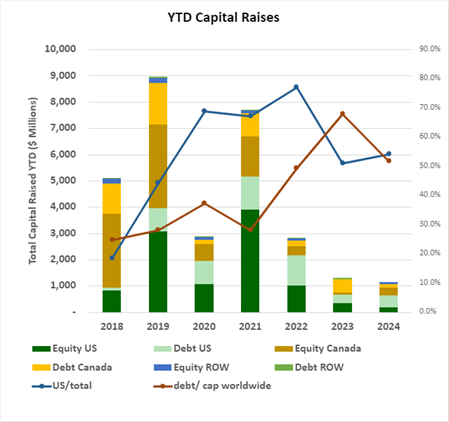

- YTD capital raises totaled $1,168.31M, down 11.0% from the same period in 2023. Debt as a percentage of capital raised dropped to 51.7% from 67.8% in the previous year on a worldwide basis. The U.S. bucked this trend with 70.1% of capital raised in debt compared to 50.6% in 2023.

- U.S. raises accounted for 54.2% of total funds, the lowest percentage since 2019. Conversely, raises from outside the U.S. represented a historically high 8.1% of the total funds raised.

- YTD raises by public companies accounted for 62.8% of total funds, the lowest percentage since before 2018.

VIRIDIAN INSIGHTS

- THE VERANO PURCHASE OF PORTIONS OF CANNABIST’S VIRGINIA AND ARIZONA ASSETS FOR A TOTAL VALUE OF $105M IS A SIGN OF RENEWED VIGOR IN THE CANNABIS M&A MARKET.

- Verano is purchasing six dispensaries and one cultivation and production facility in Virginia. Verano will become the sole cannabis operator and retailer for the HAS 5 in Eastern Virginia. Cannabist (CBST: Cboe) will retain its assets in the Richmond region with five dispensaries and 80k square feet of cultivation and manufacturing space.

- The total transaction value for the Virginia assets is $90M: $20M in cash, $40M in Class A shares, and $30M in a seller note.

- Verano is purchasing all of Cannabist’s assets in Arizona, including one cultivation facility, one production facility, and two dispensaries.

- The total transaction value for Arizona is $15M, payable in cash.

- We are not surprised that Cannabist continues to sell assets. The company has weak liquidity and excess leverage.

- We ARE surprised by the timing of the transaction, having believed that a re-acceleration of M&A would not unfold until after a rescheduling ruling.

- We do not have enough information on the acquired properties to calculate purchase multiples. Still, as a whole, Verano is trading at around 5.75x 2024 EBITDA while Cannabist is trading closer to 7.4x, so this is a strategic transaction, not one motivated by accretiveness.

- Granted, Cannabist may be a motivated seller, but Verano is using $40M of its stock in the deals at pre-S3 pop levels! Verano must feel it is getting a good enough deal to make up for potentially leaving some stock on the table. This is the sort of compromise that it takes to get deals done in this complicated environment. Congratulations to both companies!

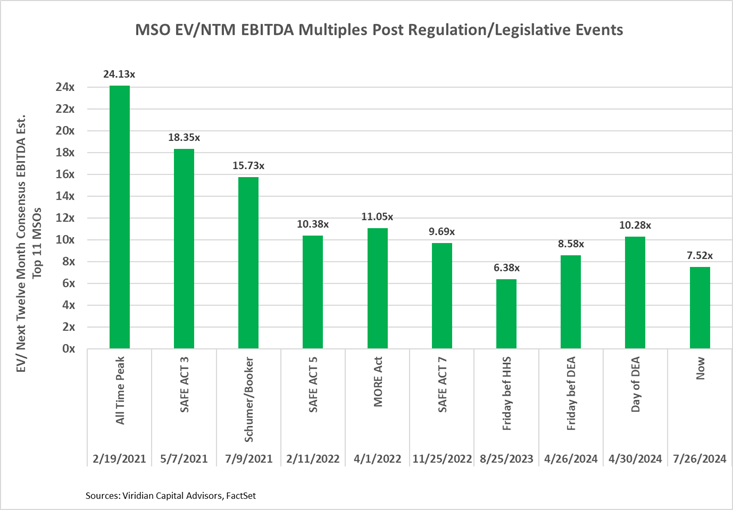

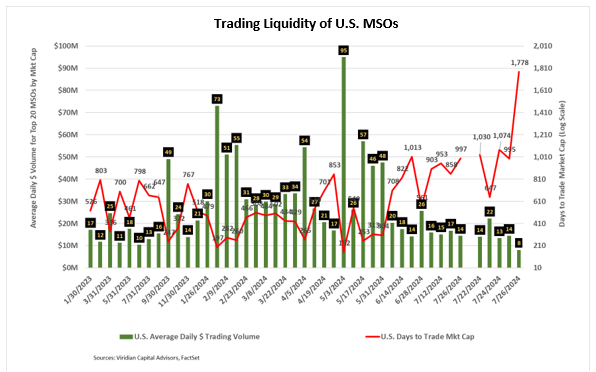

- NEITHER THE ASCENDANCY OF HARRIS TO THE PRESUMPTIVE DEMOCRATIC PRESIDENTIAL CANDIDATE NOR THE END OF THE DEA COMMENT PERIOD HAD MATERIAL POSITIVE IMPACTS ON EITHER MSO STOCK PRICES OR TRADING VOLUMES LAST WEEK

- It seemed a sure bet that these events would produce pops in stock prices and trading volumes, but the Viridian Chart of the Week proved that this was not the case.

- One intriguing issue is whether there will be a hearing before an Administrative Law Judge prior to the final rule. Evidently, more than 90% of the comments were pro-rescheduling, but that does not preclude the possibility that a comment might lead to a hearing delaying the final ruling. It doesn’t seem likely that a hearing will be required.

- A more serious issue was raised by Curaleaf Chairman Boris Jordan, who believes that S3 will almost certainly result in lawsuits. Such lawsuits would come either after the DEA issues a ruling. Jordan expressed belief that such a lawsuit would be unlikely to result in an injunction that delays the implementation of the ruling and, most importantly, 280e relief. Still, this is a risk that might help to explain why the cannabis stocks have not reacted more positively.

- We continue to believe that at current levels, U.S. MSOs have enormous upside potential. The graph below shows the multiples reached after a number of past legislative/regulatory events. The graph makes clear that a doubling of prices is a reasonable assumption. We recommend a balanced portfolio that leans toward the companies in the top half of the Viridian Credit Tracker model ranking.

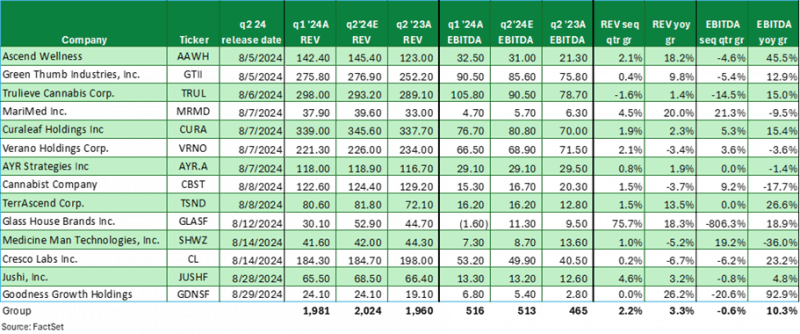

- ARE ANALYSTS STILL TOO CONSERVATIVE ON 2024 EARNINGS?

- The table below shows consensus estimates of Q2: 2024 revenues and EBITDA for 14 MSOs in order of release date. Revenues for Q1:24 and Q2:23 are presented for comparison purposes.

- Analysts are projecting a 10.2% y/o/y EBITDA growth for Q2 and full-year 2024 EBITDA growth of 9.8% compared to 2023. However, 1st half of 2024 results, including the Q2 estimates, are 14.2% higher than the 1st half of 2023, implying that second-half growth will only be around 6.0%. Are analysts expecting dramatic slowing, or have they just not updated their 2024 estimates?

- IR spokesmen for several companies have spoken of tightening consumer spending, price declines in New Jersey and other markets, and a generally competitive retail environment.

- We think the more likely expectation is that sell-side analysts have not fully reflected the 1st half strength in their numbers and are not giving 2nd half catalysts like Ohio sufficient weight.

- IS THE CANSORTIUM DEAL IN TROUBLE?

- The risk arb spread remained at a troubling 95.8% on 7/26/24, up from the mid-30% range a couple of weeks before (see the chart in the M&A section below). The spread is equal to the percentage profit an investor would make if they could purchase RIV stock, instantly exchange it into Cansortium at the announced deal exchange rate, and sell the Cansortium stock. We have been following the spread since the deal was announced, and the dramatic widening shows a significant change in investors’ rating of the likelihood of the deal closing.

- What could be wrong? Perhaps there is something about the plan for Scott’s Miracle Grow subsidiary Hawthorne to convert its RIV debt into exchangeable shares of Cansortium, that has hit a snag? That feature is fundamental to the deal economics, in our view, and it is absolutely critical to the credit improvement we see the deal creating.

- The announced merger with RIV Capital enhances Cansortium’s credit profile, and the Viridian Credit Tracker model ranking improves from #18 to #8,

- Cansortium’s net cash position goes from -$60.7M to $5.1M, dramatically improving its Viridian Capital Liquidity ranking from #23/30 to #9/30.

- Leverage is also significantly reduced, predominantly from the conversion of $175M of Hawthorne debt into Cansortium equity. The conversion also demonstrates support from Hawthorne’s parent, Scotts Miracle Grow.

- The combined company will jump to a #10 size ranking compared to the #21 ranking Cansortium had prior to the announcement.

- Cansortium is “all in” in Florida, and the transaction significantly improves the combined company’s ability to attack the potential conversion to rec of the State.

- We caution debt investors that the current risk arb spread says the deal is in danger, and cancellation of the deal would have significantly negative impacts on Cansortium’s credit rankings.

- VALUATION, LEVERAGE, AND LIQUIDITY

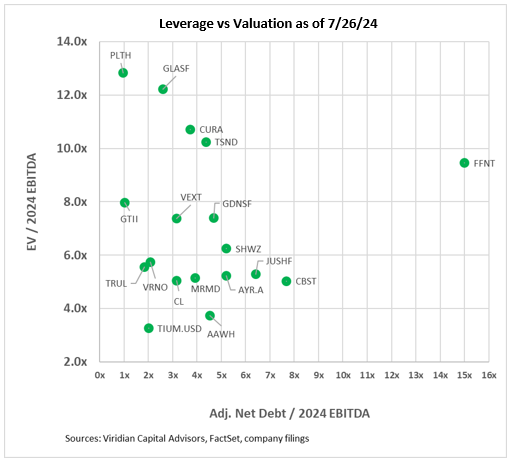

- The two graphs below show the Enterprise value to 2024 EBITDA multiples against two leverage measures. In the first graph, we have calculated an Adjusted Net Debt/ 2024 EBITDA figure by adding any accrued taxes over 90 days of tax expense to debt before subtracting cash to arrive at Adjusted Net Debt. We would expect any regular company to have accrued taxes equal to their last quarterly tax expense and consider that a standard working capital item. Several companies on the chart have far greater than 90 days of accrued taxes, and we consider the excess to be debt. Verano’s excess tax liabilities equal nearly 40% of its debt. Other companies with relatively high imputed tax debt include Curaleaf (CURA: CSE), 4Front (FFNT: CSE), and Terrascend (TSND: TSX). We have adjusted our accrued tax liabilities for comparability by adding back the tax liabilities that Trulieve, TerrAscend, and AYR moved into long-term liability accounts.

- The first graph shows that twelve of the eighteen companies have net debt/ 2024 EBITDA over 3x, which we view as the cutoff of sustainability in a 280e world. We view 4x as sustainable in a post-280e environment, and nine companies are now over that threshold.

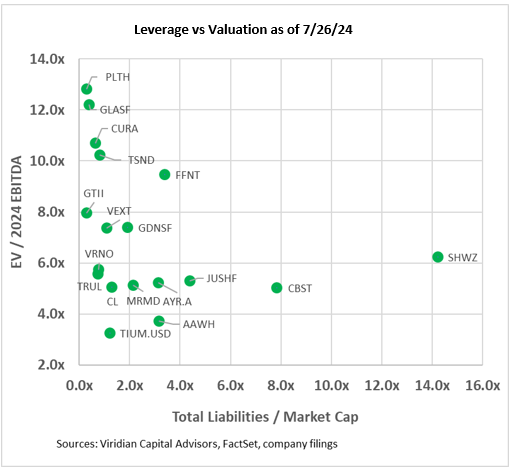

- The second graph looks at leverage through the lens of total liabilities to market cap. This measure separates the companies into four groups:

- On the bottom left are companies with low valuation multiples but also low market leverage. The group includes Verano, Trulieve, Cresco, and MariMed. The other three show that the market is not yet willing to fully embrace the Florida rec story.

- In the middle, between 2x and 4x total liabilities/market cap, we see 4Front, Ascend, AYR, Goodness Growth, and Jushi. Each of these has more than 4x debt/ EBITDA, which is borderline in terms of sustainability, even in a non-280e world. However, each also has significant upside catalysts that could mitigate or exacerbate the excess leverage. FFNT is ramping up production at its mammoth Illinois cultivation facility. Jushi is levered to potential adult rec developments in Pennsylvania and Virginia.

- On the right lie Cannabist and Shwazze. The high level of market leverage tells us that the market questions whether they can discharge their liabilities without significantly dilutive actions, and doubts are also shown by their 22/31 and 20/31 positioning in our weekly credit ranking. Cannabist has seen the writing on the wall: to levered to issue equity or debt, its only option was asset sales, and its exit from Florida was a recognition of this. The announcement of the sale of its Arizona properties and portions of Virginia are further ratification of this.

- At the top left are companies with high valuation metrics and low leverage. These companies should look to do an equity issuance depending on their positioning in the liquidity graph below.

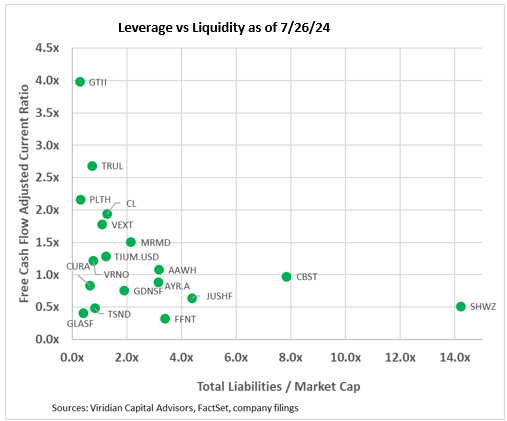

- The third graph introduces the free cash flow adjusted current ratio liquidity measure into the mix. Companies with less than 1x on this measure will likely have to raise capital next year. Surprisingly, eight of the companies fall into this bucket. This graph also breaks the sector into three distinct groupings. The bottom left group has low leverage but also modest liquidity. Some of the companies, including Verano, MariMed, and Cresco, have sufficient but not comfortable levels of liquidity, while others, including Curaleaf, TerrAscend, and Glass House, are below the critical 1x liquidity line. Companies on the lower right generally have constrained liquidity and high leverage, a potentially dangerous combination in a capital-constrained environment.

- Schwazze has alleviated some, but not all, of its near-term liquidity problem by extending the maturities of $32M to its debt. Its free cash flow adjusted current ratio remains under 1x, indicating additional financing may be required. The market is still skittish about the Company, as is evidenced by its 14x total liabilities to market cap, the highest in the group.

- CANNABIS STOCK LIQUIDITY SINKS TO ITS LOWEST

- The average daily dollar volume of $14M is tied for the lowest of the year. Liquidity in terms of Days to Trade Market Cap (see below) was worse than the corresponding period in 2023 despite several uplistings in the interim.

- The Days to Trade Market Cap (DTTMC) series depicts the number of days it would take to trade the market cap of a stock or group of stocks. The weekly reading of 997 days on 7/26/24 was the second-worst reading of the year. A 997 DTTMC implies that an investor who acquired a 5% position in the stock, assuming he wanted to be less than 25% of the average daily dollar volume, would require 199 days to trade out of his position. The age-old chicken and egg question: are there no institutional investors because market liquidity is so low, or is market liquidity so low because there are no institutional investors?

- We are firmly in the grip of the summer doldrums, but exciting macro events seem likely for the month ahead. Will trading volumes accelerate accordingly?

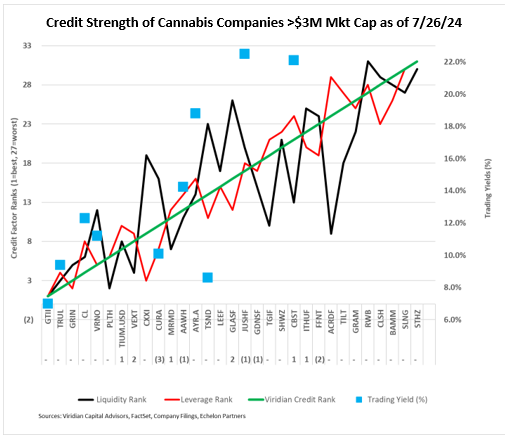

- GIVING CREDIT WHERE CREDIT IS DUE

- The chart below shows our updated 7/26/24 credit rankings for the 31 U.S. cannabis companies with over $3M market cap. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement.

- The blue squares show the offered-side trading yields for each Company. Trading yields have declined significantly since the HHS rescheduling announcement.

- There were few significant changes in rankings this week. Curaleaf (CURA: TSX) dropped three ranking slots to #10. 4Front (FFNT: CSE) gave back the two notches it gained last week primarily due to worsened relative market leverage.

- We are expecting refinancing news from both TerrAscend (TSND: TSX) and Green Thumb (GTII: CSE).

- Cannabis equities (as measured by the MSOS ETF) ended up 1.47% for the week.

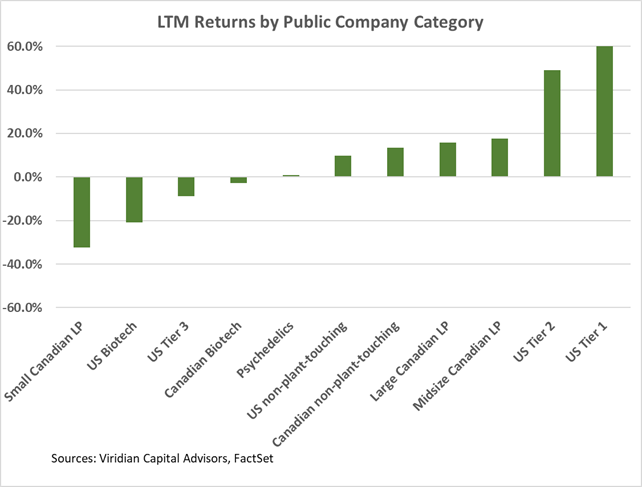

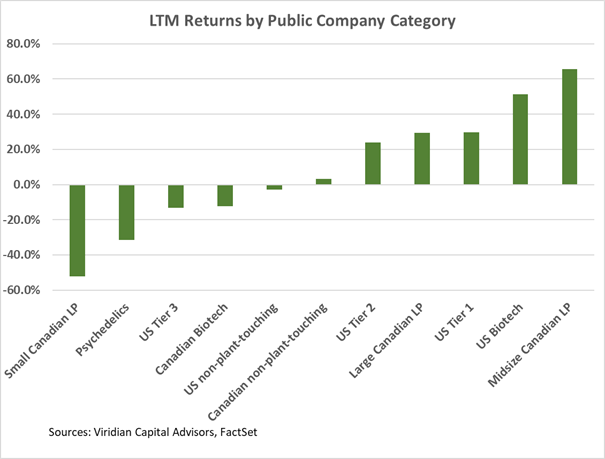

Trailing 52-Week Returns by Public Company Category:

-

- The only significant change in returns by category was the rise of U.S. Tier 2 into fourth spot, edging out Large Canadian LPs.

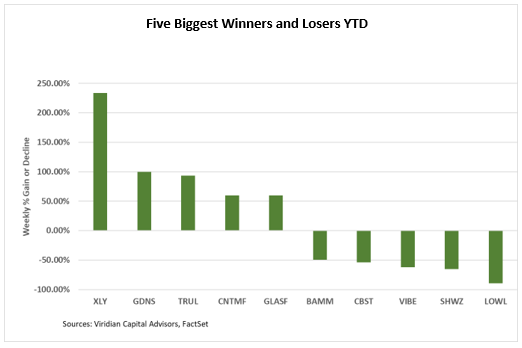

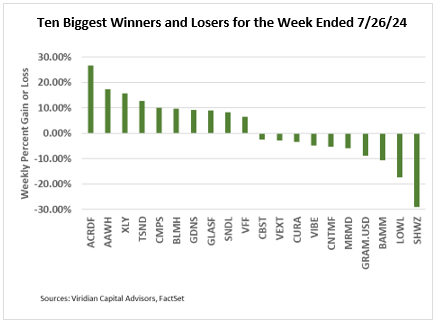

Best and Worst Performers for the week ended 7/26/24:

- Schwazze (SHWZ: CSE) was the biggest loser of the week, down 29%, as the company’s debt extension failed to calm markets worried about its continued tight liquidity even after the extensions and the possible ramifications of financial statement restatements.

- Acreage Holdings (ACRDF: OTCQX) was the largest gainer of the week, up 26.6%. We saw no news to account for the gain.