OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

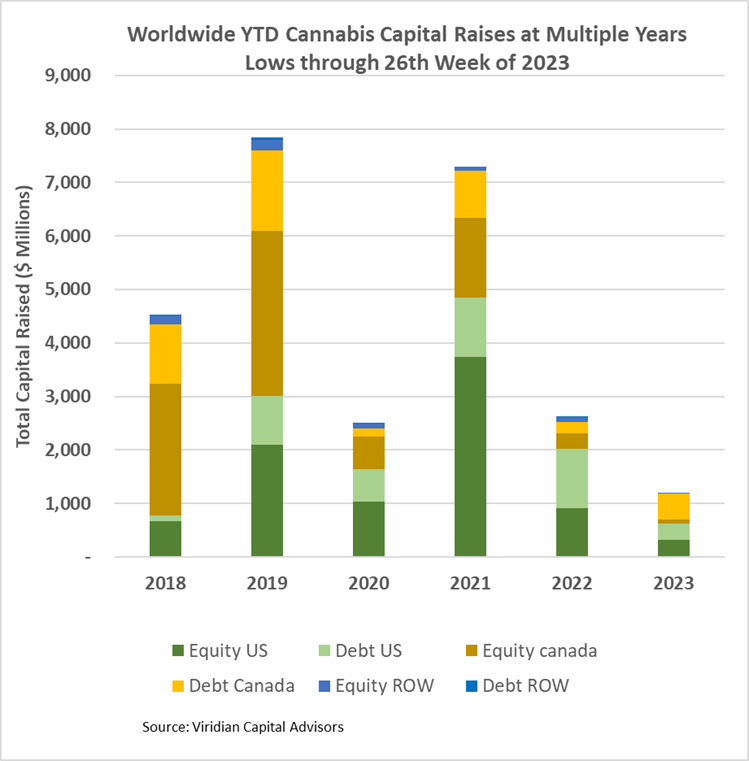

- Cannabis capital raises are off to a multi-year low. Only $1.085B closed through the first twenty-six weeks of the year compared to $2.612B last year.

- Debt represents 66.1% of total capital raised, significantly higher than in any other comparable period since 2018.

- Public companies have raised 69.4% of total capital YTD, down from 73.5% last year and lower than any comparable period since 2018.

VIRIDIAN INSIGHTS

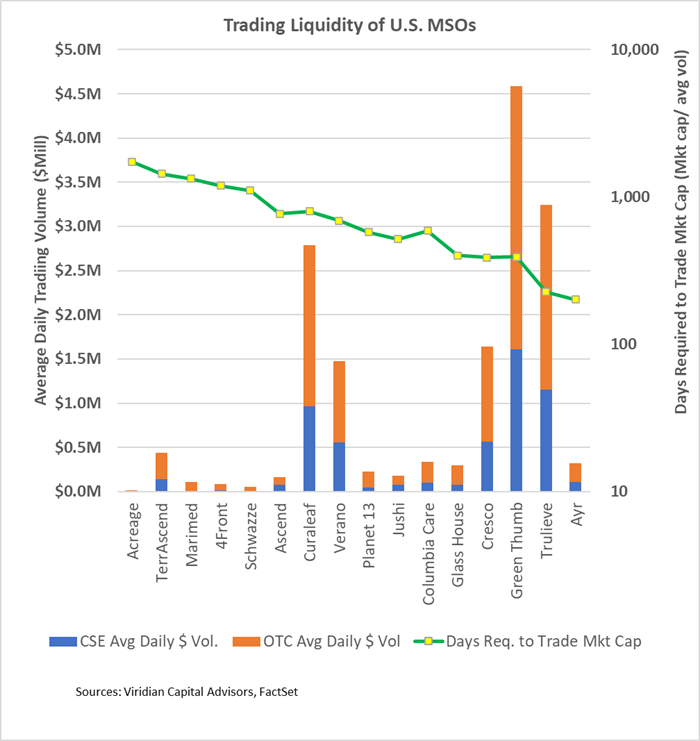

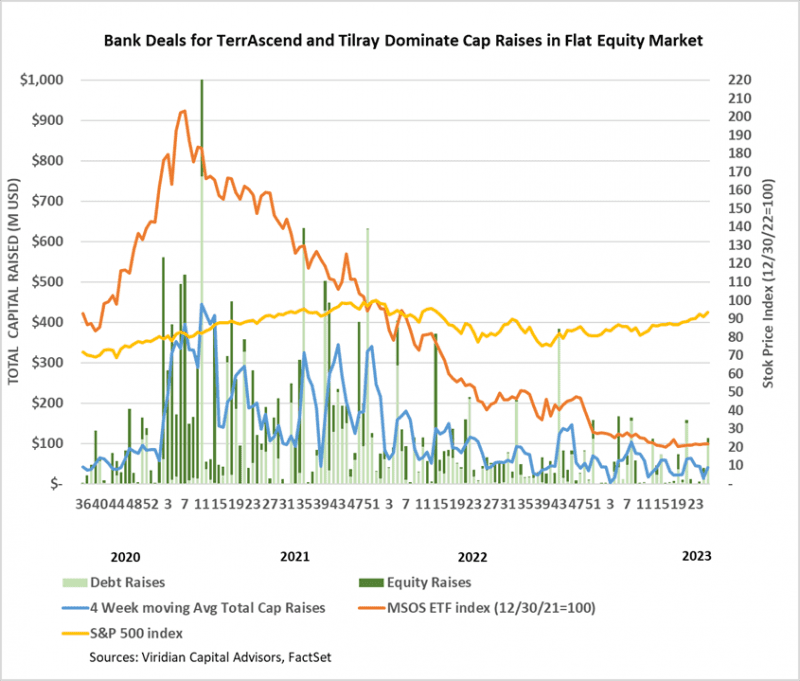

- On June 21, 2023, TerrAscend Corp. (TER: CSE)(TRSSF: OTCQX) announced that it had received approval to trade on the TSX exchange. Its first day of trading on July 4 wasn’t a fair test, but for the record, the company traded approximately 50.8k shares at average prices of about $1.82 for a dollar volume of around $92.5K

- The graph below shows updated evidence of the stock trading volume and relative liquidity of U.S. MSOs versus the top Canadian LPs. The charts’ bars indicate the average daily dollar trading volume for the first half of 2023. The blue bars indicate CSE volumes, while the orange bars indicate OTC volumes. Interestingly, every company had a higher dollar trading volume on OTC than CSE.

- The green line shows the company’s market cap divided by the average daily dollar volume, the number of days it would take to trade its market cap. TerrAscend has the second highest measure (worst liquidity) with 1,331 days. TerrAscend is correct to worry about the trading liquidity of its stock. We would expect that trading on the TSX would increase its volume, but how much?

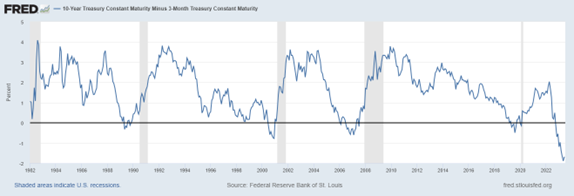

- The three-month-10-year spread became about 3bp less inverted over the last week. At -162 basis points, it is more inverted than any period over the previous 40 years, pointing solidly toward recession. Despite Powell’s hawkish rhetoric, the market is looking for a pivot. The market is misreading Powell’s true intentions; reducing goods and services inflation is only one of his goals and perhaps not the most important one. Powell aims to deflate the all-asset bubble that a decade of zero interest rates established, and it seems pretty clear that it will take a recession to do that. The alternative is to back off prematurely and live with stagflation, which may be even more damaging in the long term.

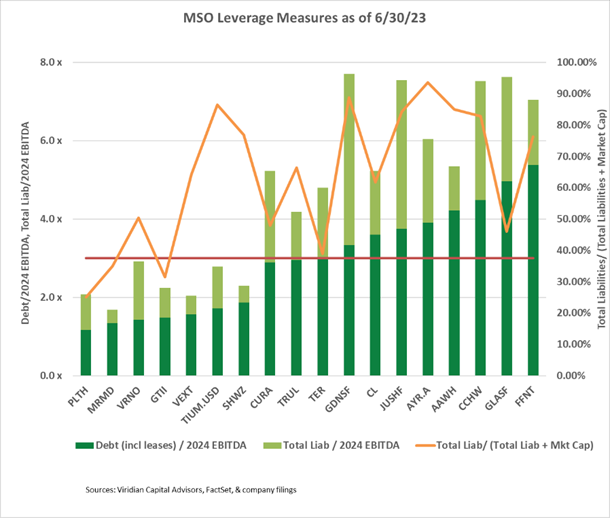

- Debt is now unsustainably high for many of the largest MSOs. Ten of the nineteen U.S. MSOs with market caps over $5M and sell-side analyst coverage now have Debt/ 2024 Consensus EBITDA estimates of over 3x. We have calculated 3x to be the approximate sustainable level of debt in the 280e environment using some simple math: If average interest rates equal 10% and effective tax rates on EBITDA equal 40%, then $1 of EBITDA for a company levered 3x debt/EBITDA will result in $.3 of free cash flow. The $3 of debt we assumed divided by the $.3 of FCF would give a payback period of 10 years!

- The companies on the graph significantly over the red line may have to contemplate a painful re-equitization to ensure their long-term survival.

- Interestingly, recently completed offerings by TerrAscend (TSND: TSX) and a planned offering by Ascend (AAWH: CSE)(AAWH: OTC) show that the pain doesn’t need to be severe. Both companies seem to have successfully priced equity issues close to pre-announcement prices.

- Greenlane (GNLN: Nasdaq) had a much uglier experience. On July 3, the company closed a $4.3M public units offering, selling 4.048M units at $1.05 per unit. Each unit consisted of one common share and two five-year warrants with an exercise price of $1.05 (0% premium). Units deals are relatively common; the company usually offers ½ warrant or one warrant per unit. The warrant life is generally two years but occasionally stretched to 3 or 4. Combining two warrants per unit with five-year lives and 0% premium is unheard of. These terms tell us that the deal was Challenging to get done. An at-the-money, 5-year warrant on a $1.05 stock has a Black Scholes value of $0.357 using 30% volatility. On this basis, the net share price of the Greenlane deal was $.336, a 68% discount!!. Greenlane’s stock has fallen 63% since the deal was announced. OUCH!

- Besides doing a painful equity issue, there is another way out of the over-levered problem- by getting acquired. Jushi just eliminated the 105% change of control put on its 12% second lien notes due 12/7/26. In return, Jushi reduced the exercise price on the roughly 16M warrants from the bond deal to $1.00 from $2.086. We calculate the value of the change in warrant exercise price to be approximately $430k, not immaterial. We may be wrong, but a company might want to make that change to look like a more attractive takeover target. We are likely to see more of the idea of reducing exercise or conversion prices to equitize debt.

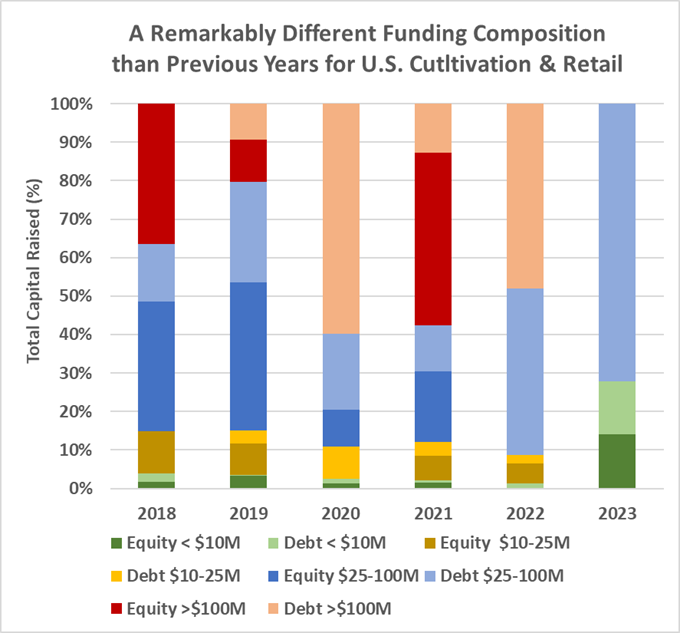

- YTD, U.S. Cultivation & Retail sector capital raises are down 81.3% from 2022.

- Debt is still the only game in town, accounting for 85.9% of all cultivation sector capital raised. 19.7% of the debt raised YTD has been for private companies.

- Large transactions are still absent from the market. There have been no debt or equity deals over $100M YTD. The graph below shows the strikingly different composition of U.S. Cultivation & Retail capital raises in 2023 compared to previous years, with small equity and midsized debt dominating raises.

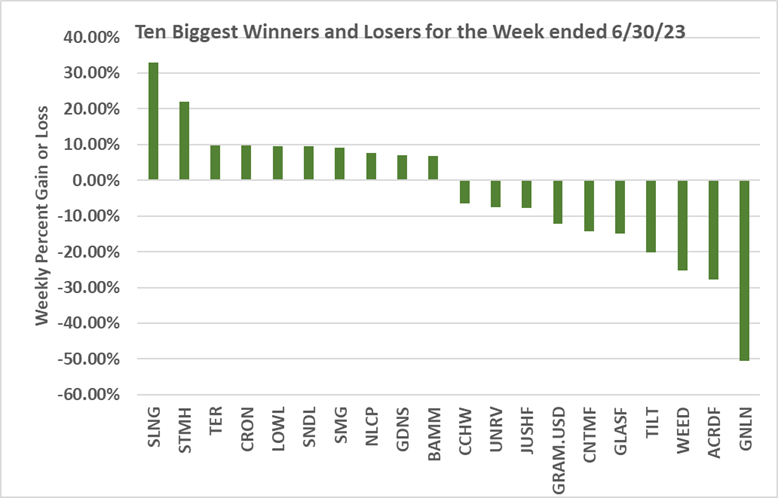

- Cannabis equities (as measured by the MSOS ETF) were up .54% for the week.

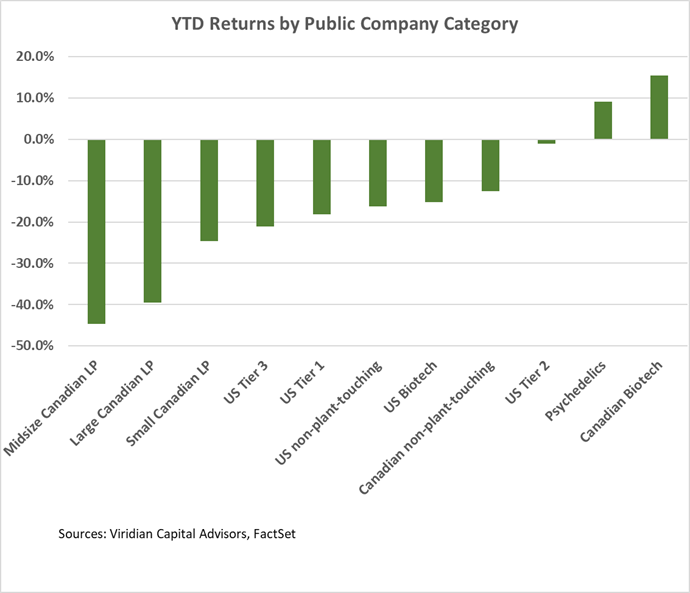

YTD Returns by Public Company Category

- The biggest change from last week was the increase in performance in the Psychedelic sector. ATAI (ATAI: Nasdaq), Mydecine (MYCO: CSE), Cybin (CYBN: Nasdaq), Mindset (MSET: CSE), and Red Light Holland (TRUFF: Nasdaq) were all up by more than 10% this week.

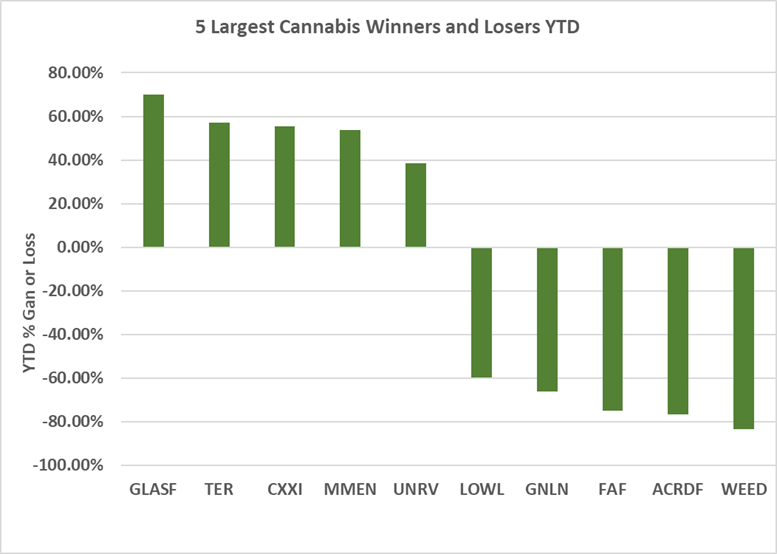

Best and Worst Performers of the last week and YTD

- Greenlane was the worst-performing stock of the week based on its horrific units, which we discuss in more detail in our Insights section.

- Other big losers include Canopy Growth (CGC: Nasdaq) and Acreage (ACRDF: OTC). Canopy’s woes appeared to accelerate after posting a qualified audit opinion on its financials and having its auditor quit. To the company’s credit, it is taking appropriate steps to ensure survival by aggressively pursuing the equitization of debt. Unfortunately for Acreage, association with Canopy is no longer a positive.

- TerrAscend (TSND: TSX)(TRSSF: OTCQX) is one of the week’s biggest gainers based on the completion of debt and equity financings, the closing of dispensary deals in Maryland, beginning to trade on the TSX. We closely monitor the average daily trading volume in TSND on the TSX.