OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

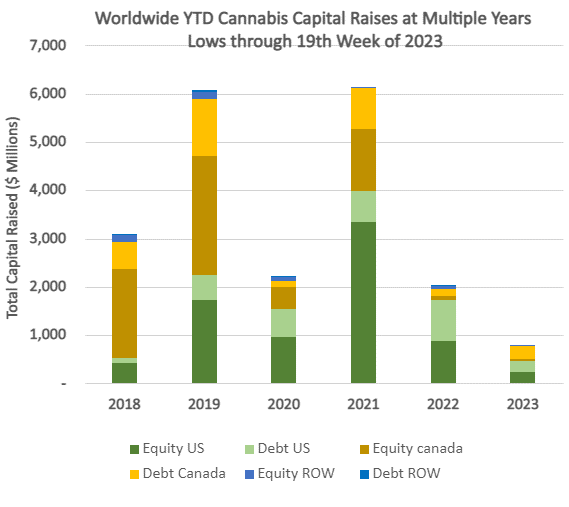

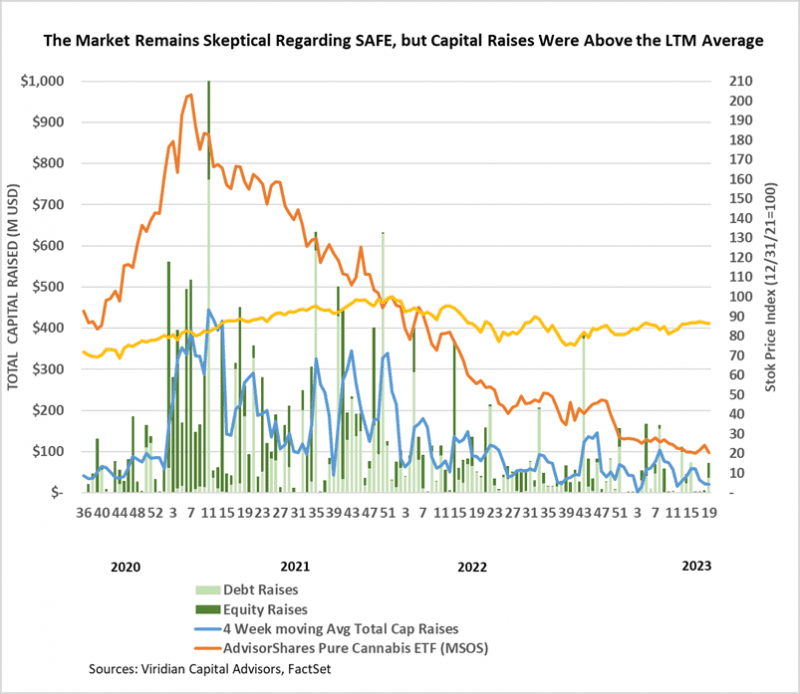

- Cannabis capital raises are off to a multi-year low. Only $860.82M closed through the first nineteen weeks of the year compared to $2,023.24M last year.

- Debt represents 61.1% of total capital raised, higher than in any other comparable period since 2018.

- Public companies have raised only 60.7% of total capital YTD, down from 76.0% last year.

VIRIDIAN INSIGHTS

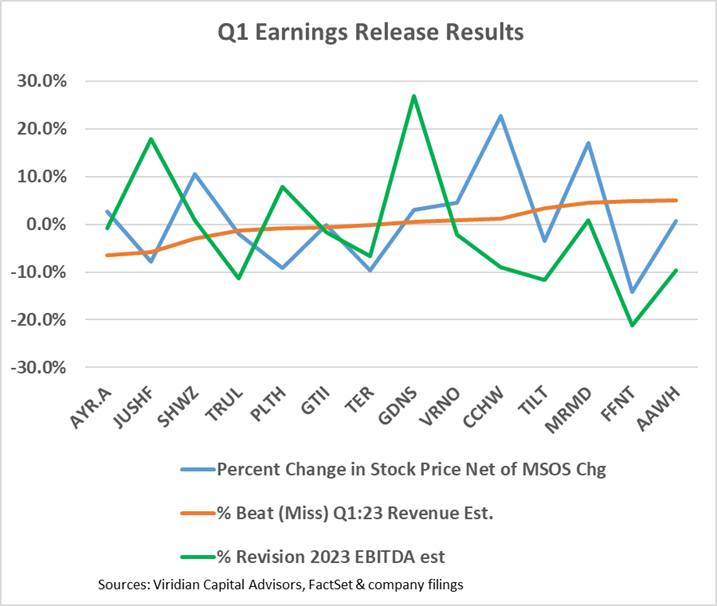

- Earnings releases for Q1:23 are nearly completed, and the graph below displays the results. The red line shows the percent difference between actual revenues and consensus analyst estimates. The surprises were modest, with the worst miss at 6.4% and the biggest beat at 5%. The blue line shows the percentage movement in the stock after netting out the percentage movement of the MSOS ETF. Note the lack of correlation between revenue misses and stock performance. This is unsurprising and is why we focus little on these quarterly misses. The green line shows the percentage revision of consensus 2023 EBITDA estimates over the last week. Note that only three companies, Jushi (JUSHF: OTC), Planet 13 (PLTH: CSE), and Goodness Growth (GDNS: CSE), had positive 2023 EBITDA revisions. We focus more on the longer term revisions since we find them more closely correlated with stock price movements. Four companies had greater than 10% downward revisions this week, Trulieve (TRUL: CSE), Tilt (TILT: NEO), 4Front (FFNT: CSE), and Ascend Wellness (AAWH: OTC). We believe that slowing downward EBITDA revisions is required for the market to find a solid bottom.

- Last week the New York Office of Cannabis Management introduced proposed new rules that would allow medical license holders (Ros) to enter the market this year rather than having to wait until 2025. The proposal would allow one collocated store by year-end, with second and third stores after June 2024. The new proposal also changed the timing of the payment of $20M per company, stretching it out over four $5M payments rather than one upfront payment. The fee has been a massive bone of contention, and the New York Medical Cannabis Association commented, “We believe that the proposed $20M licensing fee for each medical cannabis provider to enter the adult-use market is illegal and subject to legal challenge.” Nonetheless, the new proposal appears to have been positively received by investors. The graph below shows the one-week net gain in the RO stocks after subtracting the percentage movement in the MSOS ETF. The disastrously slow pace of New York’s adult-use rollout has allowed thousands of illicit pop-up dispensaries to become deeply entrenched where they will be difficult to uproot. Hopefully, the changes announced last week are a sign that rational economic reasoning is coming forward.

- On May 8, 2023, New Jersey Governor Phil Murphy signed legislation that allows legal cannabis businesses to deduct operating expenses from taxable income. New Jersey joins Virginia, Massachusetts, Missouri, and Maryland as states that have recently decoupled IRS code 280e from their tax code, according to a recent article by the accounting and consulting firm Armanino. These changes only affect state taxes, but the impact can still be considerable. We estimate that in a state with a 9% corporate tax rate like New Jersey, this change could improve cannabis company cash flows by between 2 and 3%.

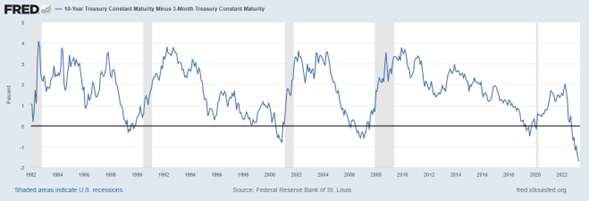

- Over the last week, the 10-year minus 3-month yield spread at -169bps has become less inverted by seven basis points. Is this a positive sign or an ominous one? We have no crystal ball, but we expect a significant recession in the year ahead. The graph below shows that the inverted curve has correctly predicted the last five recessions, and typically, the curve becomes normal and then steepens as the recession commences.

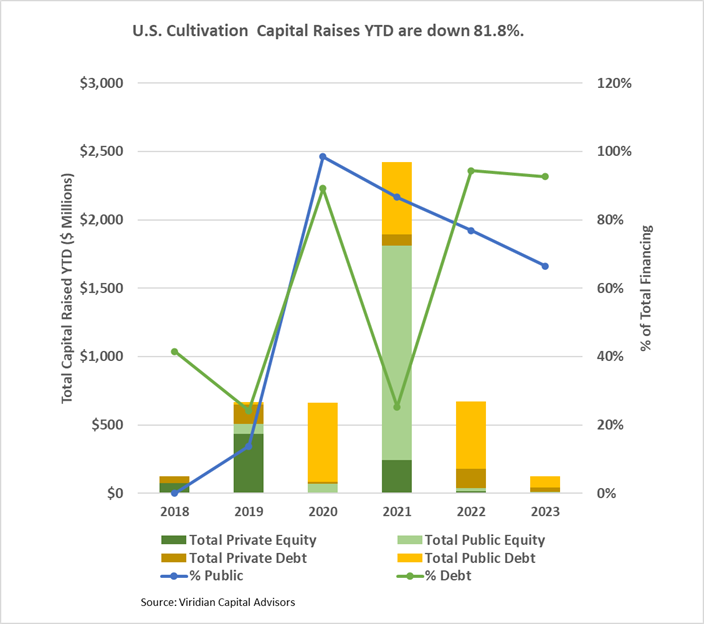

- YTD, U.S. Cultivation & Retail sector capital raises are down 81.8% from 2022.

- Debt is still the only game in town, accounting for 92.6% of all cultivation sector capital raised. All the debt raised YTD has been for public companies.

- Large transactions are still absent from the market. There have been no debt or equity deals over $100M YTD.

- Cannabis equities (as measured by the MSOS ETF) were down 15.05% for the week due to the controversy surrounding the SAFE Act hearings. The loss was the largest since 2022, following last week’s record gains.

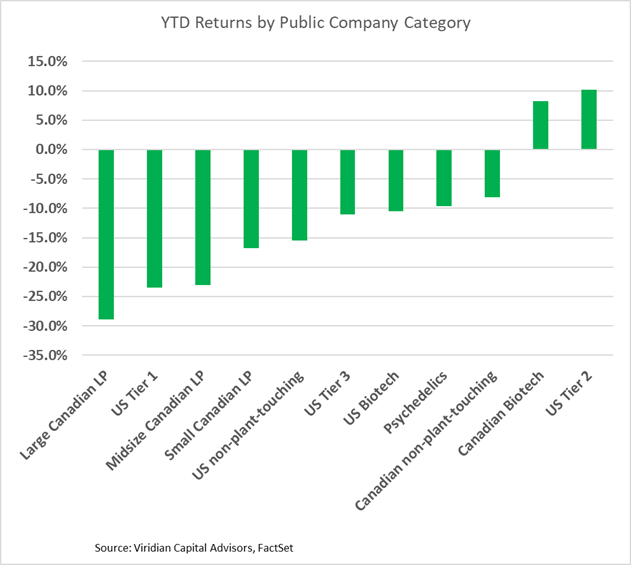

YTD Returns by Public Company Category

- Tier one MSOs fell sharply as the SAFE Act hearings became contentious last week. Senator Schumer’s pledge to add social equity provisions to the bill adds uncertainty.

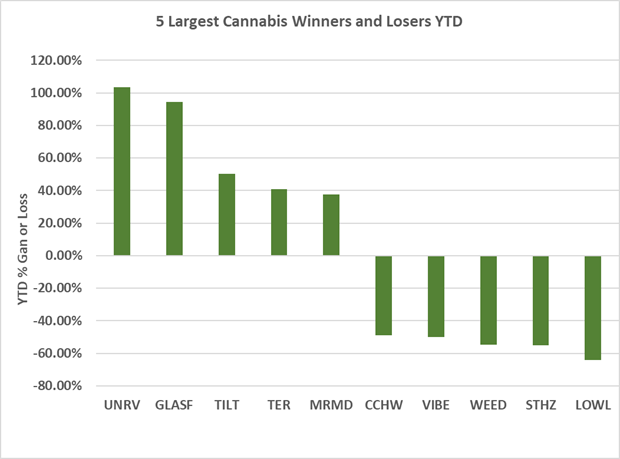

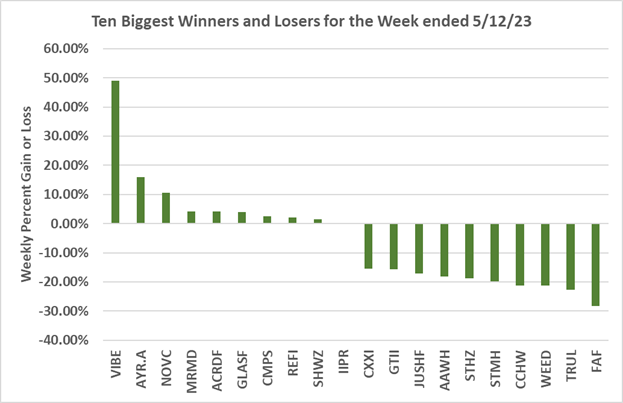

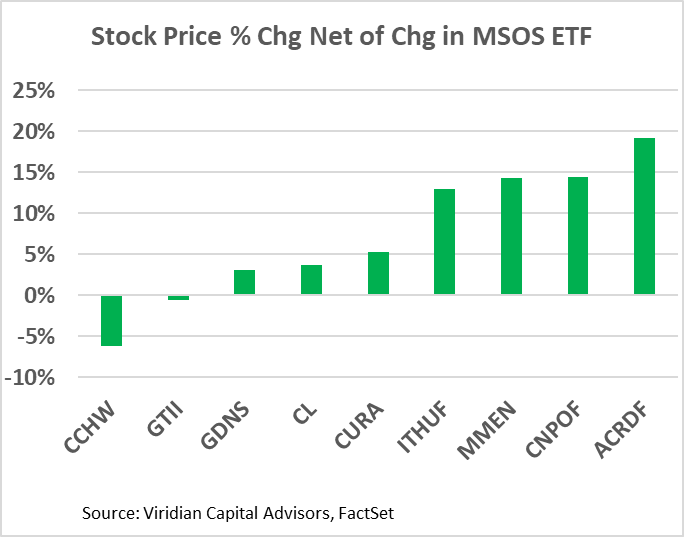

Best and Worst Performers of the last week and YTD