OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

- The U.S. raises accounted for 51.6% of total funds, the lowest percentage since 2019. Conversely, raises from outside the U.S. and Canada, spurred by a sizeable psychedelic equity raise in the U.K., represented a historically high 12.7% of the total funds raised.

- YTD raises by public companies accounted for 76.9% of total funds.

VIRIDIAN INSIGHTS

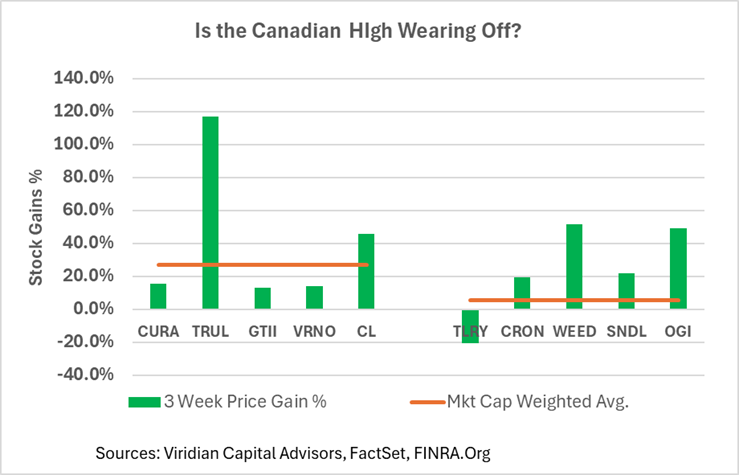

- IS THE CANADIAN LP HIGH WEARING OFF?

- The chart below now shows the YTD percentage gain in the top five U.S. MSOs versus the top five Canadian L.P.s.

- Two weeks ago, this chart looked dramatically different. The Canadian L.P.s were soaring to levels that frankly made us believe the Canadian L.P. investors were smoking too much of the product.

- The bubble-piercing moment seemed to be the lackluster earnings report from Tilray, which took down the whole complex. After being up 180% for the YTD period, Canopy is now up only 57%, and the average return for the Canadian L.P.s is now below the U.S.

- However, if we take out the spectacular returns from Trulieve and the loss from Tilray, we continue to see a better average return from Canada.

- We have discussed in prior weeks the likely reasons for this: the opening of Germany, the report recommending changes in Canadian regulation, and the perception that the U.S. may be opened soon. We are unconvinced.

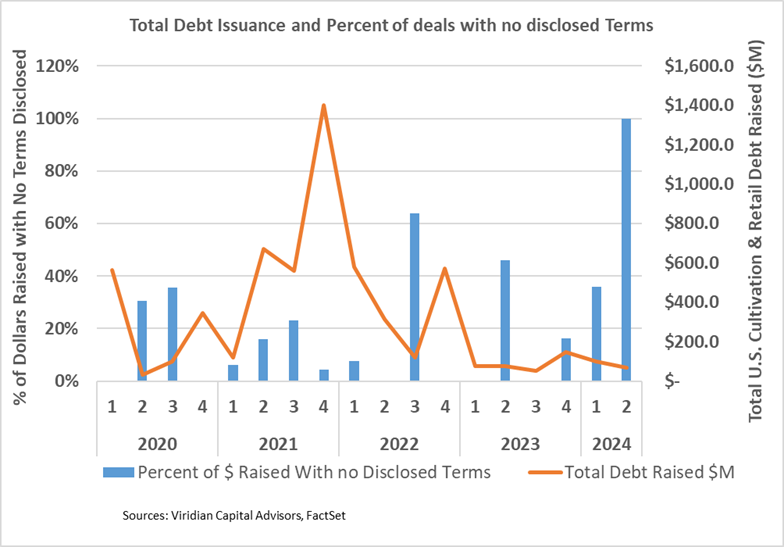

- RUN SILENT RUN DEEP?

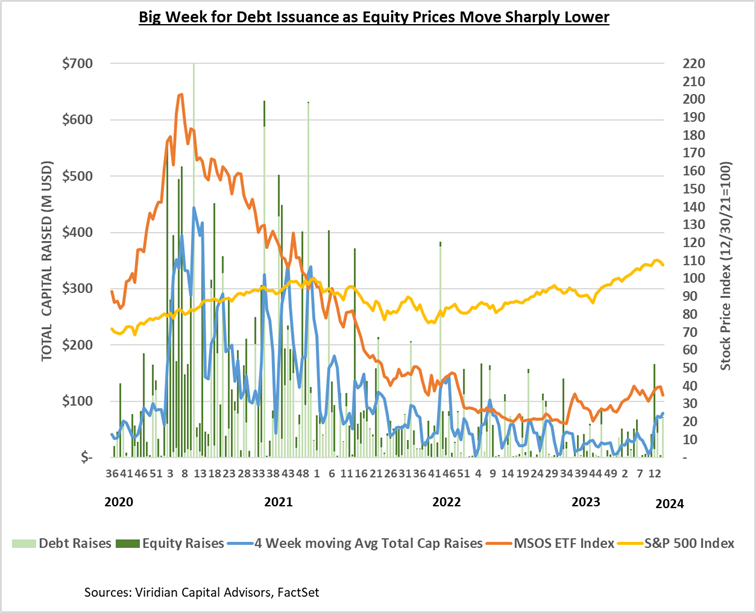

- Debt financing is heating up in the U.S. Cultivation and Retail sector. So far in the second quarter, $95M of debt has been raised, compared to $100M in the first quarter. All of it has been raised in transactions in which no specific deal terms were disclosed: no coupon, no maturity date, no information about warrants, etc.

- The chart shows that this is the highest percentage of deals done with no deal terms since 2020.

- Why?

- All of the deals have either been private REG D deals like the Pharmacan raise chronicled in this week’s tracker or loans from Chicago Atlantic or AFC Gamma. It’s pretty typical for these shops not to disclose the terms. But historically, many of the borrowers have.

- One has to wonder if what’s happening here is that the all-in-deal terms are not really something the borrowers are anxious to publish. We believe credit quality is not the issue as we respect the due diligence work done by these lenders, but rather the scarcity of capital pushing the price of debt upward. Note we have no hard data to prove this; it’s just a judgment call.

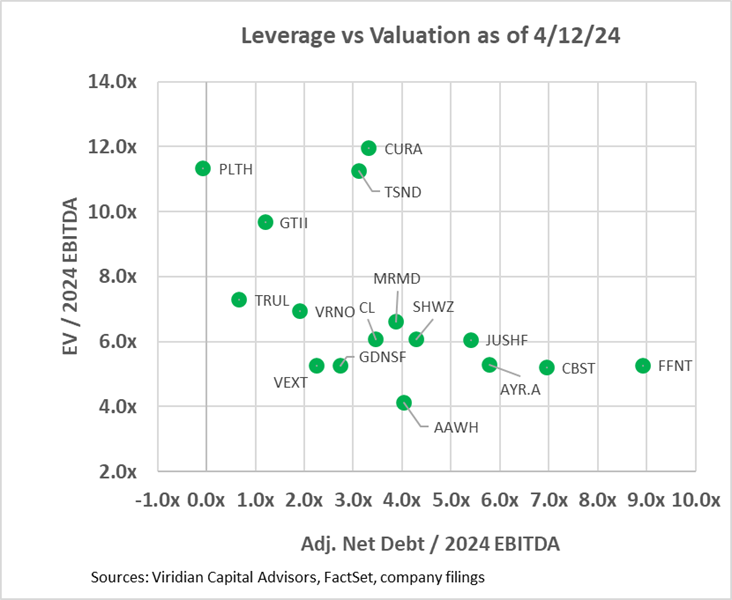

- VALUATION, LEVERAGE, AND LIQUIDITY

- The two graphs below show the Enterprise value to 2024 EBITDA multiples against two leverage measures. In the first graph, we have calculated an Adjusted Net Debt/ 2024 EBITDA figure by adding any accrued taxes over 90 days of tax expense to debt before subtracting cash to arrive at Adjusted Net Debt. We would expect any regular company to have accrued taxes equal to their last quarterly tax expense and consider that a standard working capital item. Several companies on the chart have far greater than 90 days of accrued taxes, and we consider the excess to be debt. Verano’s excess tax liabilities equal nearly 40% of its debt. Other companies with relatively high imputed tax debt include Curaleaf (CURA: CSE) and 4Front (FFNT: CSE) at 19%, and Terrascend (TSND: TSX) at 17%.

- The first graph shows that ten of the seventeen companies have net debt/ 2024 EBITDA over 3x, which we view as the cutoff of sustainability in a 280e world. We view 4x as sustainable in a post-280e environment, and five companies are now over that threshold.

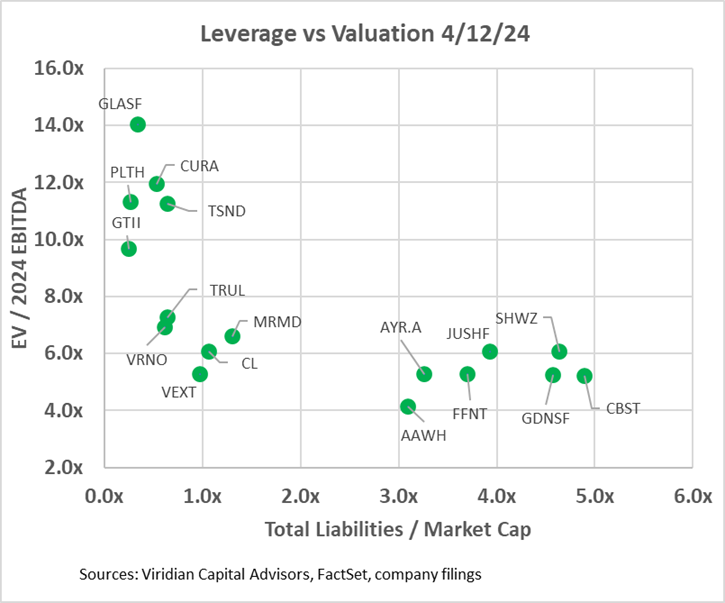

- The second graph looks at leverage through the lens of total liabilities to market cap. This measure separates the companies into two groups based on the market’s belief on whether a company can discharge its liabilities without highly dilutive actions, like discounted stock sales or refinancing debt with a heavy warrant or share consideration.

- Companies that have too much debt but have low liabilities to market cap are candidates for stock sales or debt for equity exchanges. These companies include Cresco and TerrAscend. Alternatively, these companies may de-lever by using their high valuation to buy cash flow. TerrAscend spoke to this possibility on its earnings call.

- Goodness Growth is in precisely the opposite situation. It is not as levered as Curaleaf on an adjusted Debt to EBITDA basis. Still, its stock is trading at such low multiples that the prospect of issuing equity to reduce debt seems unlikely. This is why we anticipated an asset sale like the company’s recently announced sale of its New York licenses and properties.

- Jushi, AYR, Cannabist, and 4Front appear significantly overleveraged in both an EBITDA and Market Cap sense. However, each has some element of optionality that might prove 2024 EBITDA estimates too conservative. For Jushi, it is Pennsylvania and Virginia (although Virginia’s hopes are stymied for the time being by the governor’s veto of legislation that would open adult sales). For AYR, it is Florida. Cannabist is in Ohio, New York, Pennsylvania, and Florida. 4Front is levered to Illinois.

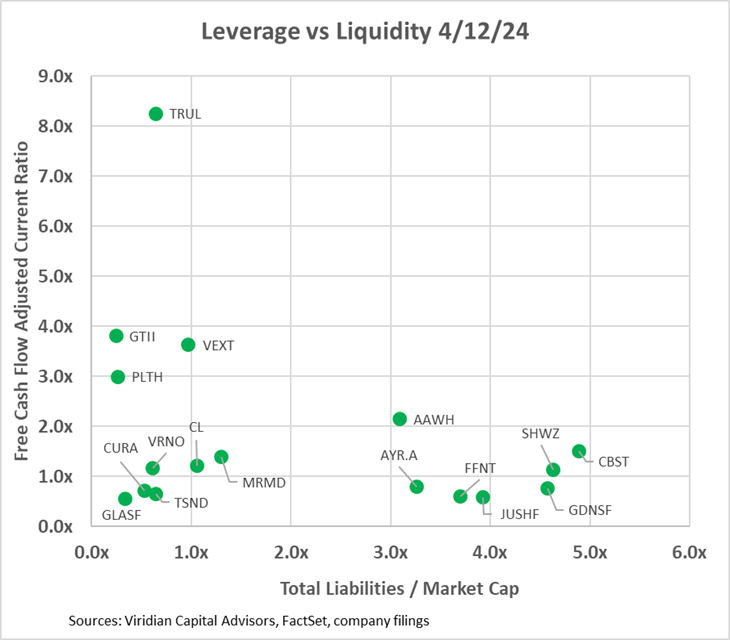

- The third graph introduces the free cash flow adjusted current ratio liquidity measure into the mix. Companies with less than 1x on this measure will likely have to raise capital next year. Six of the companies fall into this bucket.

- Looking at leverage in two ways and having a comprehensive measure of liquidity can give investors a good idea of possible scenarios for today’s overleveraged companies. Companies with low valuation metrics, high EBITDA, market cap basis leverage, and low liquidity include Jushi, 4Front, AYR, and Goodness Growth. Cannabist appears to have reasonable near-term liquidity; however, it is very highly leveraged and trading at discounted multiples.

-

-

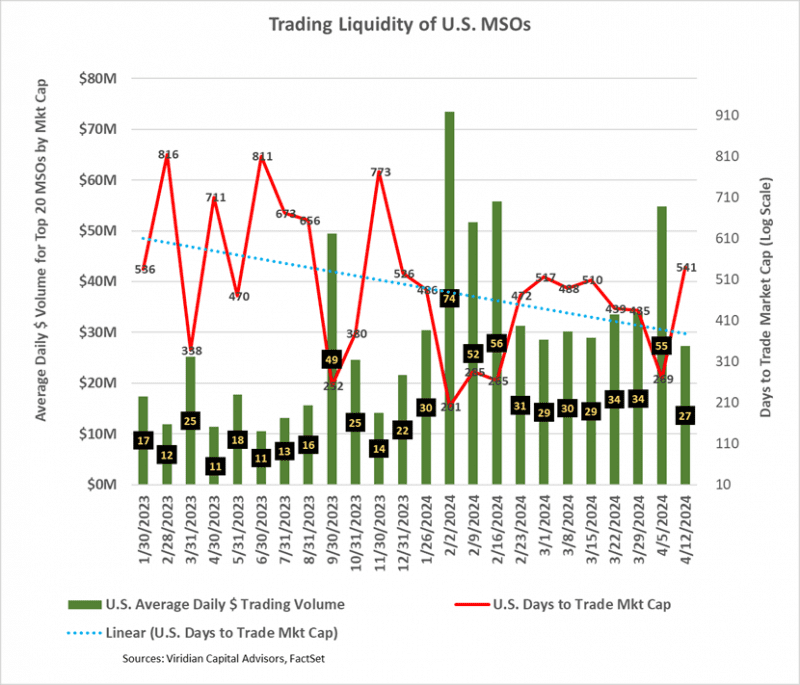

- CANNABIS STOCK LIQUIDITY DETERIORATED IN THE MOST RECENT WEEK TO ITS LOWEST LEVEL YTD

- The Days to Trade Market Cap (DTTMC) series depicts the number of days it would take to trade the market cap of a stock or group of stocks. Its most recent reading of 541 days is above the downward trend line shown on the graph. A 541 DTTMC implies that an investor who acquired a 5% position in the stock, assuming he wanted to be less than 25% of the average daily dollar volume, would require 108 days to trade out of his position.

- Interestingly, several of the companies with the highest dollar trading volume, like Curaleaf, appear to be among the most illiquid when viewed through the DTTMC lens.

- CANNABIS STOCK LIQUIDITY DETERIORATED IN THE MOST RECENT WEEK TO ITS LOWEST LEVEL YTD

-

-

-

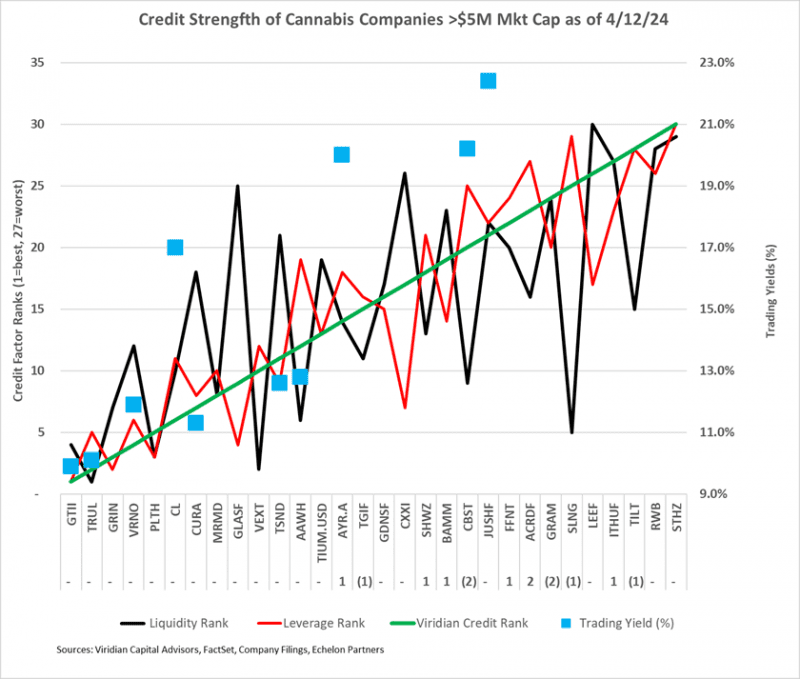

- GIVING CREDIT WHERE CREDIT IS DUE

- The chart below shows our updated 4/12/24 credit rankings for the 30 U.S. cannabis companies with over $5M market cap. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement.

- The blue squares show the offered-side trading yields for each company. Trading yields have declined significantly since the HHS rescheduling announcement.

- The rankings spread between Trulieve and Curaleaf appropriately widened this week.

- Based on this week’s rankings, Curaleaf debt now looks fairly priced, trading at a reasonable spread to GTI and Trulieve, which we believe are superior credits. Trulieve should trade at a bit wider spread to GTI. Cresco’s senior secured term debt continues to appear too cheap, so trading out of Curaleaf into Cresco seems like a good trade. Jushi’s debt has traded off, appropriately given the governor’s veto of adult rec in Virginia. AYR has significantly more leverage to a Florida rec event, and we believe it should trade at a lower yield relative to Cannabist.

- Jushi trades at a higher yield than comparable credits because the debt is 2nd lien rather than the first lien.

- GIVING CREDIT WHERE CREDIT IS DUE

-

-

-

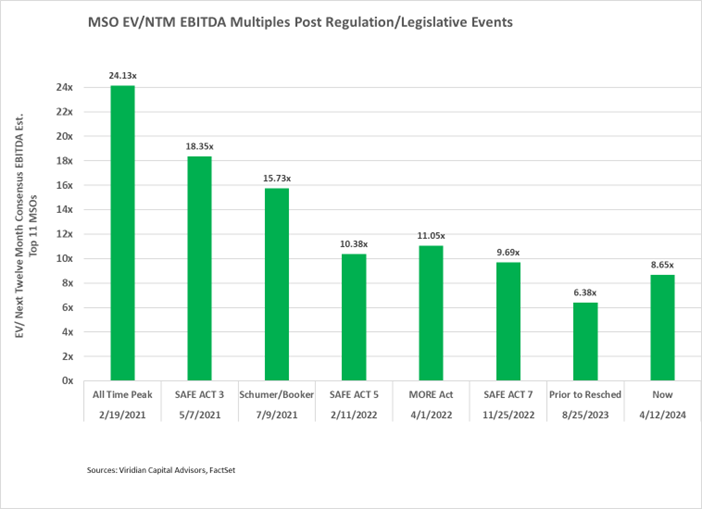

- THERE IS STILL CONSIDERABLE UPSIDE POTENTIAL

- The chart below shows enterprise to next-twelve-month valuation multiples now compared to previous times when positive regulatory/legislative news hit.

- THERE IS STILL CONSIDERABLE UPSIDE POTENTIAL

-

-

- The chart demonstrates a healthy investor skepticism regarding positive regulatory/legislative events in Washington, DC.

- EV/NTM EBITDA Multiples were up sharply this week and are now 16.7% below the levels after the 5th SAFE Act passage in the House in February 2022. Still, the rescheduling news is more significant as it dramatically impacts cash flows. If valuations multiples rose to where they were after the announcement of the Schumer-Booker bill, the incremental gains would equal 81.8%. We view a DEA announcement ratifying the HHS recommendation to be much more significant than introducing the Schumer-Booker bill, which most observers viewed as DOA and had no immediate impact on operator cash flows. Accordingly, we believe there is considerably more runway for price increases, perhaps reaching the 5/7/21 multiples of 18.35x, producing 112.1% returns from current levels.

- We also note, however, that the downside risk from an adverse DEA announcement has grown. If Schedule 3 were to go away (unlikely but possible) totally, we would expect stocks to go back to at least as low as they were before the HHS announcement, and this would imply a 31.8% loss. We think the downside could be a bit more.

- Probability weighting seems like a reasonable approach here, however subjective it may be. We ascribe a 60% chance of a positive DEA announcement that boosts stocks by 81%, a 20% chance of a doubling, and a 20% chance of a loss of 50%. The expected gain from this is approximately positive 59%.

- Cannabis equities (as measured by the MSOS ETF) were down 11.86% for the week.

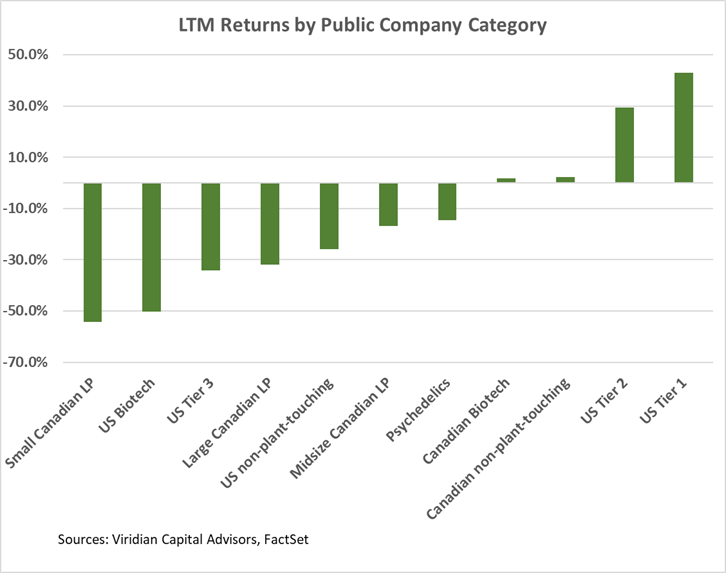

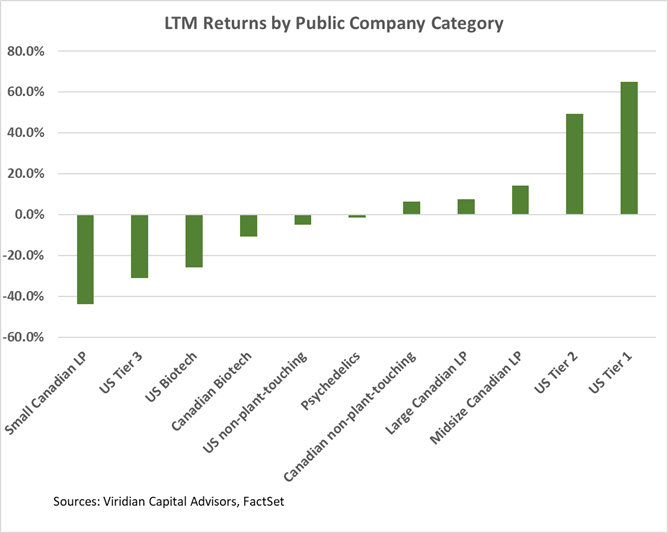

Trailing 52-Week Returns by Public Company Category:

- U.S. Tier One MSOs are now up over 60% for the LTM period, and Large Canadian L.P.s are now up around 17%. Canopy Growth is still down 36% for the period despite its 57% gain YTD.

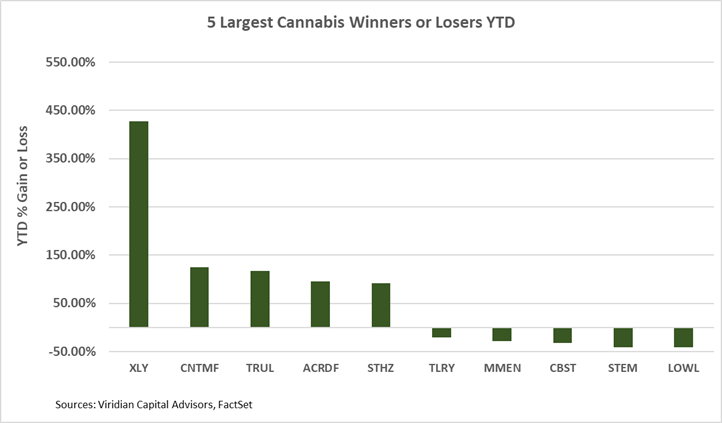

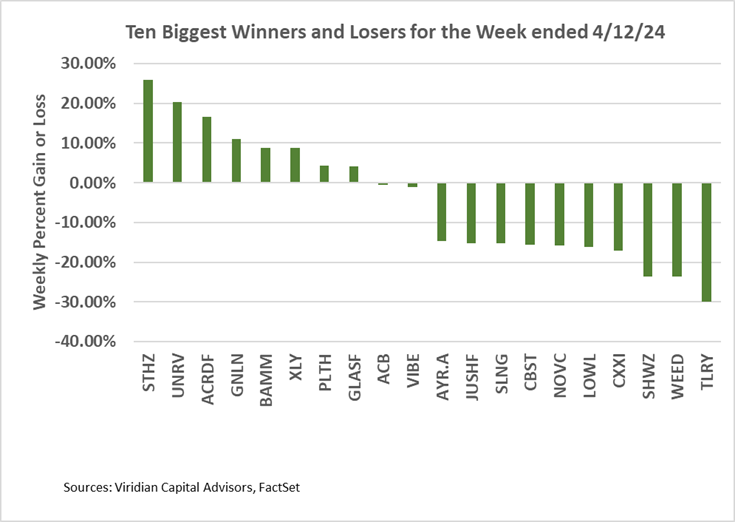

Best and Worst Performers of the last week and YTD:

- Trulieve and Cansortium are the top gainers YTD with over 100% increases. Both would be beneficiaries from Florida Adult Rec., but we think the potential is still much higher, potentially another doubling, without 280e relief!

- Big gainers for the week include many of the weakest-rated credits, including StateHouse, Blum Holdings, Acreage, and Greenlane.

- Big losers included Tilray and Canopy Growth as the market reassessed Canadian L.P. valuations relative to U.S. MSOs.