OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

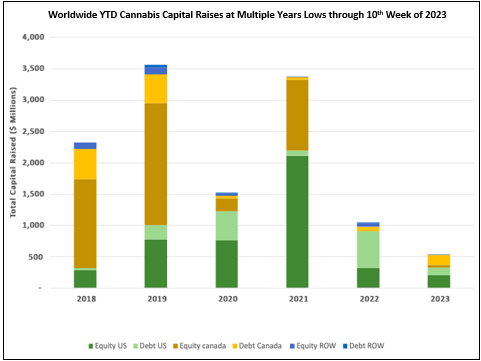

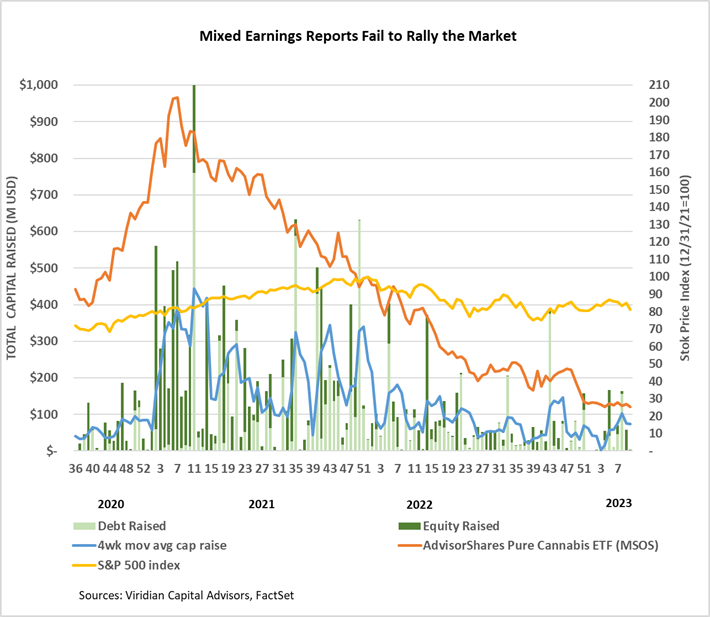

- Cannabis capital raises are off to a multi-year low. Only $540.55M closed through the first ten weeks of the year compared to $1,037.34M last year. Debt represents 53.1% of total capital raised. There has only been one week since the beginning of 2021 when less capital was raised than this week.

- Public companies have raised only 65.1% of total capital YTD, down from 79.1% last year.

VIRIDIAN INSIGHTS

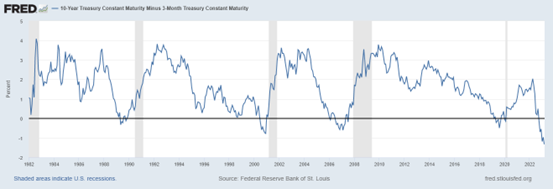

- The Silicone Valley Bank Failure seemed to appear in nearly every news story this week. We find it fascinating that with an inflation-pummeled consumer, a steepening downturn in housing, and the approach of what must be the most well-anticipated recession in history, what did in SVB had nothing to do with credit. Although the bank’s loan portfolio tilted towards riskier tech credits, by all measures, their loan loss reserves and loss experience were quite good. Indeed one might think they did the right thing by parking so much cash in “riskless” government bonds instead of extending more startup loans. They failed, however, because of factors in the graph below depicting the 3-month vs. 10-year treasury spread. We watch this spread versus the more commonly monitored 2–10 year spread precisely because it better mirrors the economics of bank lending and is a more accurate predictor of recessions.

- The inverted curve shows that the primary activity of borrowing short-term and lending long is unprofitable at times like now when the curve is steeply inverted. That might have weakened SVB over time, but it wouldn’t have killed it like the forces of a crowd stampede, and make no mistake about it, no bank can’t live through a run like SVB experienced.

- Why did it happen? Bank risk management was lacking in not having secondary sources of liquidity and locking up so much of its assets in low coupon high duration bonds. There also seems to be some guilt on the part of Peter Thiel, who loudly advised depositors to withdraw funds, apparently after his own Founder’s Fund had withdrawn all of its cash. There is blame to be shared by the large number of companies that maintained deposits greatly exceeding the FDIC limit. These companies were responsible for monitoring the health and risks of the institutions where they put cash. The fact that these depositors will be made whole strikes us as bad policy. Fundamentally, we doubt that such a small nonsystematic bank would have caused a cascade of other failures. We do, however, understand that it may be better to be safe than sorry.

- A more important question at this point is what this means for Fed policy toward rates and inflation. The curve above is now more inverted than it’s been in twenty years, signaling a high recession risk. So does the Fed bail on inflation? We think not. The Fed is after more than just simple inflation. It is trying to correct the all-asset bubble caused by a decade of zero-cost money, and we don’t think Jay Powell will back down that quickly. He may not do 50bp, but we think 25 is still in the cards and may not be the last raise. The market believes the Fed will pivot, so look for some ugly price action when it figures out it was wrong.

- Luckily, we see no direct impact on cannabis.

- Today TerrAscend (TER: CSE) announced that it would seek uplisting from the CSE to the TSX exchange. We had been waiting for a large US MSO to make this move since Canopy’s roll-up of its U.S. operations.

- It comes down to this: how do MSOs make their stocks more valuable? The SAFE Act doesn’t seem likely to happen. Margins continue to be compressed by wholesale price declines and inflationary cost increases. The capital markets are as tight as ever, making expansion funding difficult, if not uneconomic. Many, if not most, companies have laid off people and tightened their expenses. So what’s left? Greater stock liquidity! Institutional investors have stayed out of cannabis for many reasons: illegality, reputational risk, a horrendous period of declining prices, etc., but they are still on the sidelines looking. Cannabis stocks are also nearly uninvestable for prominent players due to their illiquidity. Imagine the impact on even the largest MSO if an institutional investor wanted to buy or sell $100M of stock. The TSX has multiples of the CSE’s trading volume, which will potentially get more institutions to invest in cannabis.

- So why not everyone jump into the pool? It’s not so easy!

- In 2017, the TSX issued a staff notice that listed issuers “with ongoing business activities that violate U.S. federal law regarding marijuana are not complying” with applicable listing requirements. Furthermore, the notice made it clear that “ongoing business activities” would be broadly interpreted.

- There may be ways to restructure the business that gets around these restrictions. One method involves creating a new listing company that only owns non-voting, non-participating shares of the plant-touching business that are exchangeable under certain conditions (like U.S. legalization) for ordinary shares. This avenue is what Canopy is pursuing.

- Despite the allure of uplisting, the process seems costly and potentially fraught with unintended consequences. For example, will these arrangements affect the attractiveness of the company’s stock as acquisition currency? Will it make the company less attractive as an acquisition target? What accounting or tax implications are there? It’s safe to say that only large companies are likely to burn the lawyer’s time to attempt this move soon. It will be fascinating to watch. Cynically speaking, maybe this is what it will take to get banking reform back on track.

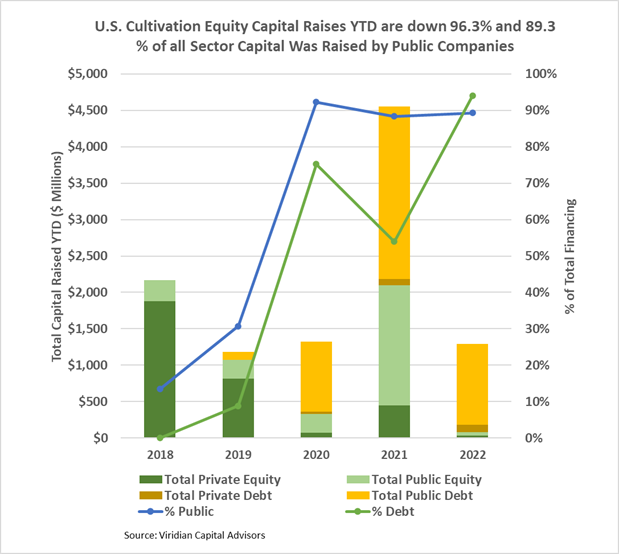

The U.S. Cultivation & Retail sector capital raises are down 71.6% YTD, but equity capital raised is down approximately 96.3%:

- Debt financing is down 50.6% YTD but accounts for about 94.0% of all capital raised; private companies raised 8.7% of it.

- 89.3% of total capital raises YTD were completed by public companies compared to 88.4% in 2021.

- In 2022, there have been no equity deals above $25M.

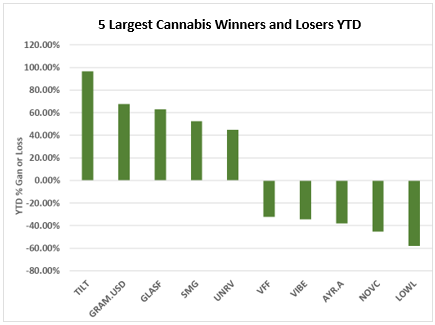

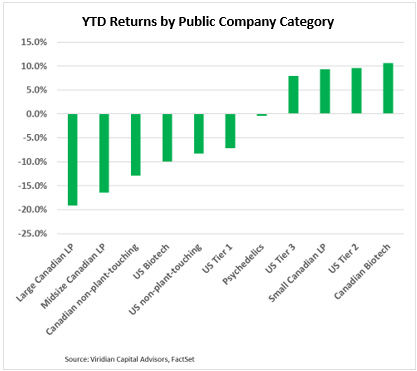

YTD Returns by Public Company Category

- The relative ordering of YTD returns by category is mostly unchanged from last week, except for U.S. Tier 1 MSOS, which have lost two ranking notches since the previous week.

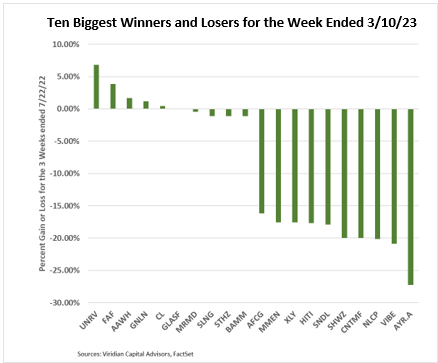

Best and Worst Performers of the last week and YTD