OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

VIRIDIAN INSIGHTS

-

- Rumors of potential dissent within the DEA were enough to send the market into a headlong retreat, with the MSOS down 8.6% for last week and an additional 8.4% for the first two days of this week. It clearly shows how single-minded the market has become regarding rescheduling. While we cannot handicap what is happening behind closed doors at the DEA, we have pointed out that several significant MSOs like GTI, Verano, and Trulieve are not dependent on a kick save from 280e relief. That may not save the stocks in the event of an adverse rescheduling announcement (which we continue to view as unlikely) since the entire market would likely trade off sharply; it at least means that these companies are not facing a fiscal cliff or a need to dilute shareholders to pay off debt

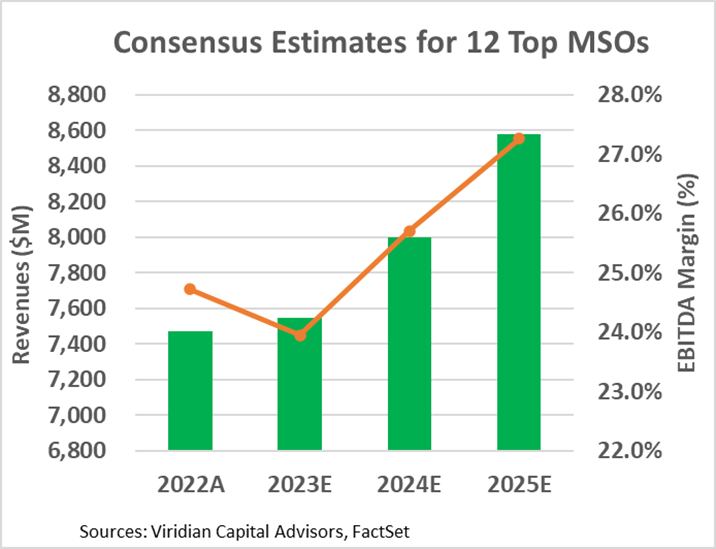

- ANALYSTS MAY BE UNDERSHOOTING ON 2024 EBITDA PROJECTIONS

- The Chart below shows consensus revenue and EBITDA margin estimates for the top twelve MSOs.

- Analysts may be too cautious with the group’s 2024 revenue growth projection of 6.0%. A year of Maryland and Ohio and near-term price stability in several key markets suggests a higher growth expectation may be in order.

- Similarly, we believe the 25.7% 2024 consensus EBITDA margins may be too low as they are only 100bp higher than the 2022 figures. The industry found religion in 2022 and 2023, stringently managing costs and tightening working capital controls. The industry is poised to be more efficient and profitable as growth returns.

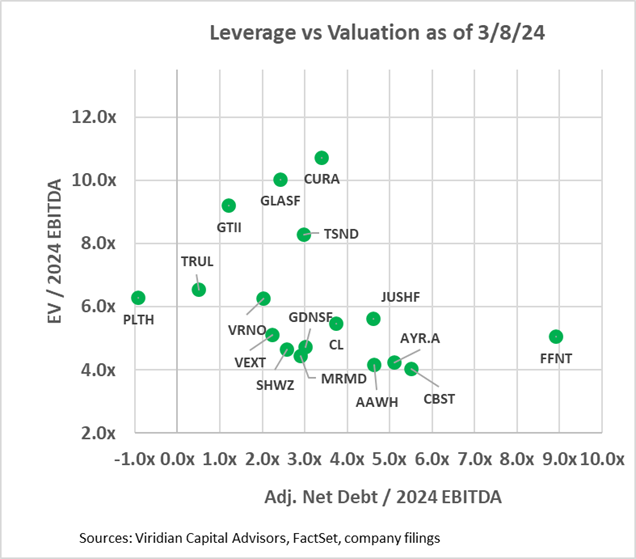

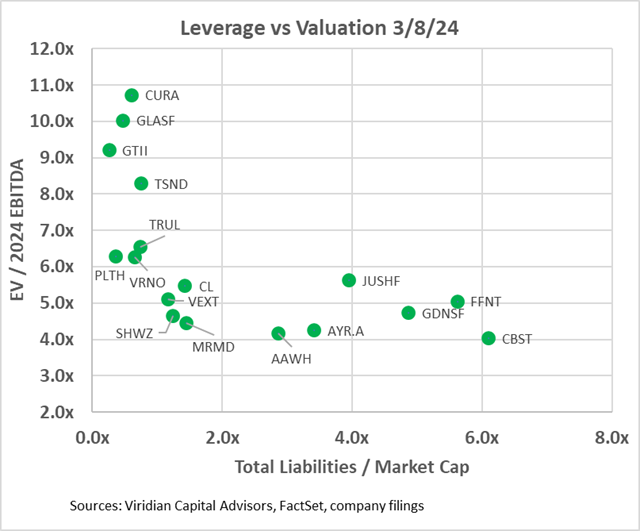

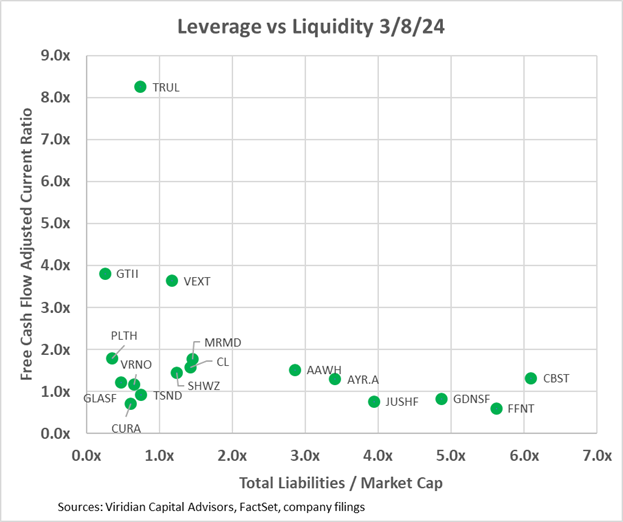

- VALUATION, LEVERAGE, AND LIQUIDITY

- The two graphs below show the Enterprise value to 2024 EBITDA multiples against two leverage measures. In the first graph, we have calculated an Adjusted Net Debt/ 2024 EBITDA figure by adding any accrued taxes over 90 days of tax expense to debt before subtracting cash to arrive at Adjusted Net Debt. We would expect any regular company to have accrued taxes equal to their last quarterly tax expense and consider that a standard working capital item. Several companies on the Chart have far greater than 90 days of accrued taxes, and we consider the excess to be debt. Verano’s excess tax liabilities equal nearly 40% of its debt. Other companies with relatively high imputed tax debt include Curaleaf (CURA: CSE) and 4Front (FFNT: CSE) at 19%, and Terrascend (TSND: TSX) at 17%.

- A comparison of the two top graphs is instructive. Some companies like TerrAscend, Goodness Growth, and Curaleaf appear to be directly on or slightly over 3x adjusted net debt to EBITDA, which we view as the demarcation line of long-term sustainability.

- TerrAscend and Curaleaf have relatively low total liabilities to market cap because the market is valuing their stocks at such high multiples. These companies should issue equity at these high multiples to directly fund debt reduction or use equity to purchase another company and increase EBITDA. An acquisition of one of the companies trading at much lower EBITDA multiples is likely to be accretive.

- Goodness Growth is in precisely the opposite situation. It is not as levered as Curaleaf on an adjusted Debt to EBITDA basis. Still, its stock is trading at such low multiples that the prospect of issuing equity to reduce debt seems unlikely. Goodness Growth will likely have to sell assets or sell itself to work out of its overleveraged situation.

- Jushi, AYR, Cannabist, and 4Front appear significantly overleveraged in both an EBITDA and Market Cap sense. However, each has some element of optionality that might prove 2024 EBITDA estimates too conservative. For Jushi, it is Pennsylvania and Virginia. For AYR, it is Florida. Cannabist is in Ohio, New York, Pennsylvania, and Florida. 4Front is levered to Illinois.

- The third graph shows that AYR and Cannabist have better liquidity than Jushi or 4Front and are less likely to need to push a highly dilutive equity deal or expensive debt deal into the market.

- Looking at leverage in two ways and having a comprehensive measure of liquidity can give investors a good idea of possible scenarios for today’s overleveraged companies.

-

-

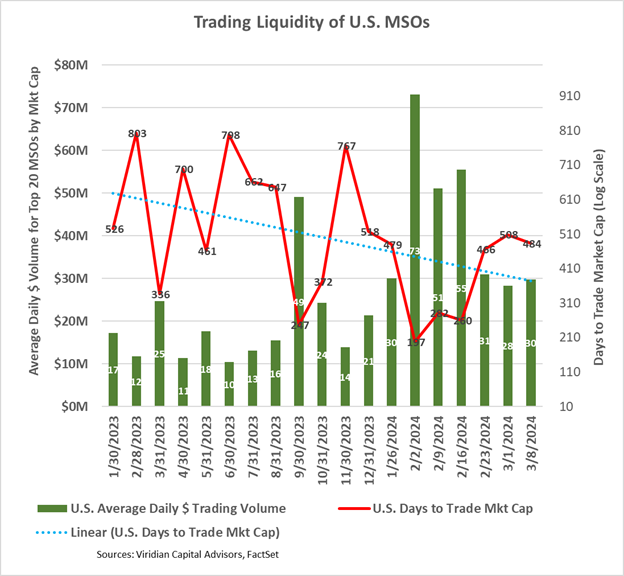

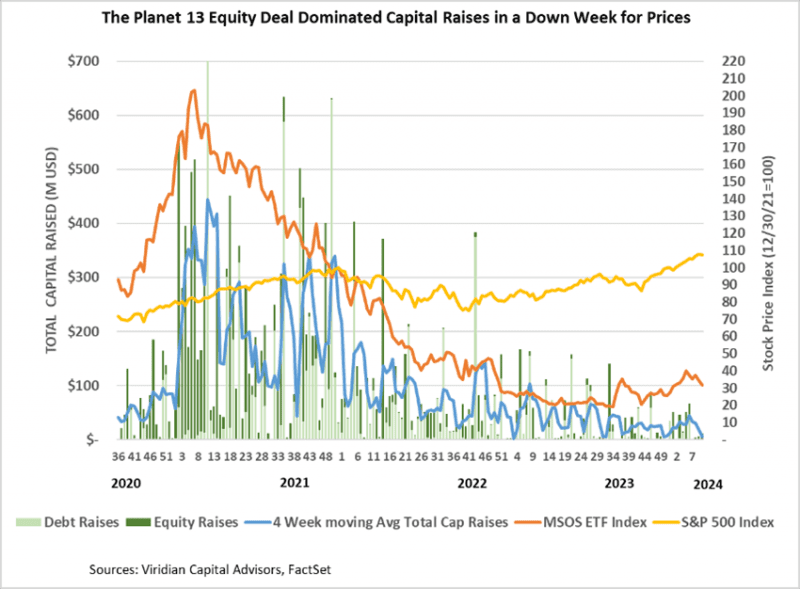

- CANNABIS STOCK LIQUIDITY DROPS

- After several unusually strong trading weeks in early February, primarily created by false rumors of imminent rescheduling announcements and the portfolio rebalancing by the MJUS ETF, trading volume has been off sharply in the last three weeks. More telling is the increases in the Days to Trade Market Cap (DTTMC) series, which eponymously depicts the number of days it would take to trade the market cap of a stock or group of stocks. Its most recent reading of 484 days is above the downward trend line shown on the graph. The reality is that very little new institutional capital has come into the cannabis market. The investors are still the same, and many are not committing additional funds to the industry until some of the regulatory smoke clears. Will rescheduling change this? Perhaps, but not directly. Still, at the margin, the cash-flow-enhancing impacts of Schedule 3 will make cannabis more investible and attract more capital.

- CANNABIS STOCK LIQUIDITY DROPS

-

-

-

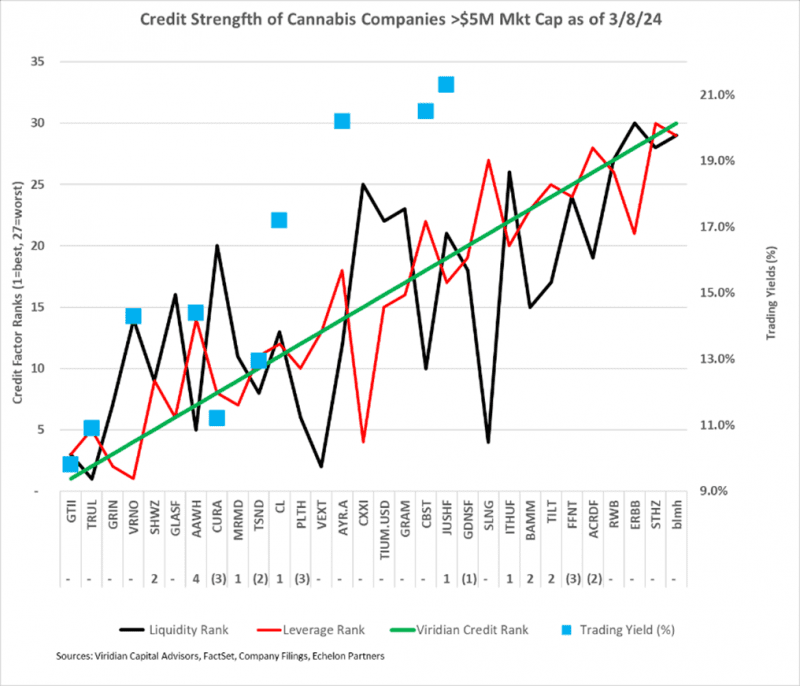

- GIVING CREDIT WHERE CREDIT IS DUE

- The Chart below shows our updated 3/8/24 credit rankings for the 30 U.S. cannabis companies with over $5M market cap. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement.

- The blue squares show the offered-side trading yields for each company. Trading yields have declined significantly since the HHS rescheduling announcement.

- There were several big movers this week, with Ascend improving by four notches and Curaleaf deteriorating by three. Curaleaf looked rich even before this downgrade, and a trade into Trulieve for a minor yield give-up makes sense. Even better would be to trade into either Verano or Ascend term loans for significant yield pickup and credit improvement.

- 4Front dropped three places, and our charts on leverage versus liquidity make the case. The company is an outlier on leverage and liquidity and is particularly vulnerable to any bad news on rescheduling.

- More ranking changes are likely in response to earnings releases in the next two weeks.

- GIVING CREDIT WHERE CREDIT IS DUE

-

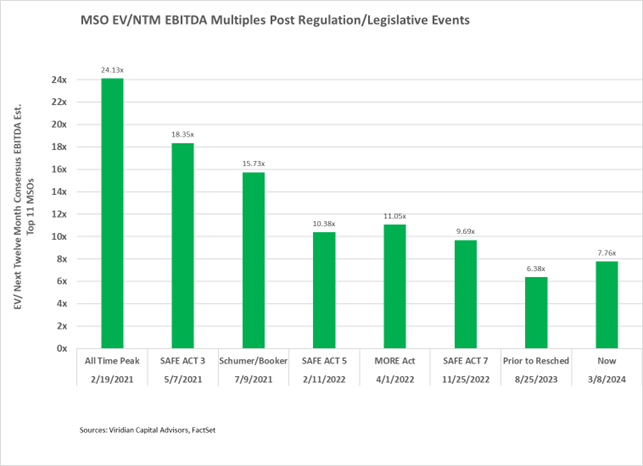

- THERE IS STILL CONSIDERABLE UPSIDE POTENTIAL

- The Chart below shows enterprise to next-twelve-month valuation multiples now compared to previous times when positive regulatory/legislative news hit.

- The Chart demonstrates a healthy investor skepticism regarding positive regulatory/legislative events in Washington, D.C.

- EV/NTM EBITDA Multiples fell sharply this week and are now 25.2% below the levels after the 5th SAFE Act passage in the House in February 2022. Still, the rescheduling news is more significant as it dramatically impacts cash flows. If valuations multiples rose to where they were after the announcement of the Schumer-Booker bill, the incremental gains would equal 102.7%. We view a DEA announcement ratifying the HHS recommendation to be much more significant than introducing the Schumer-Booker bill, which most observers viewed as DOA and had no immediate impact on operator cash flows. Accordingly, we believe there is considerably more runway for price increases, perhaps reaching the 5/7/21 multiples of 18.35x, producing 136.5% returns from current levels.

- Cannabis equities (as measured by the MSOS ETF) were down 8.68% for the week.

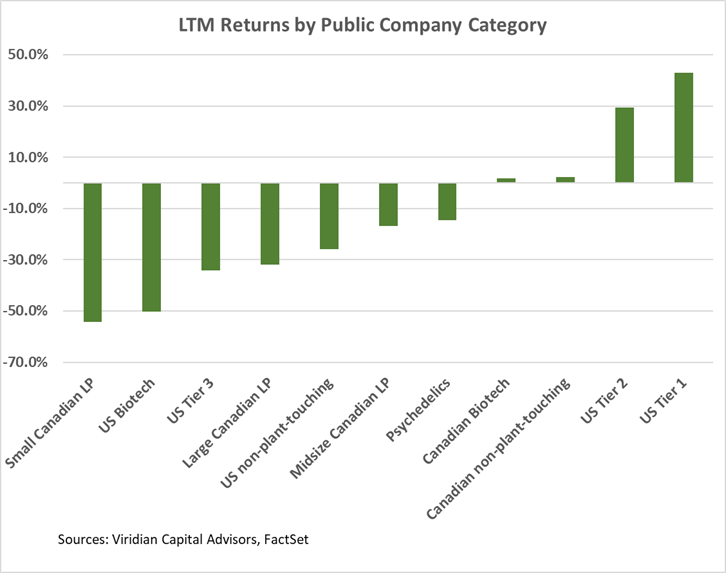

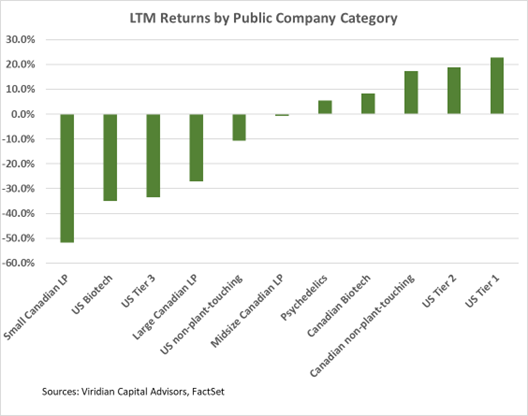

Trailing 52-Week Returns by Public Company Category:

- U.S. Tier One MSOs continue performing best out of our eleven categories. Still, the gap between Tier One and Tier Two MSOs has narrowed, as demonstrated by the Viridian Valuation Gap chart in the M&A section of the tracker.

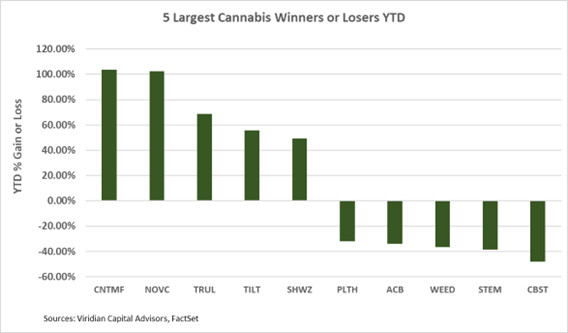

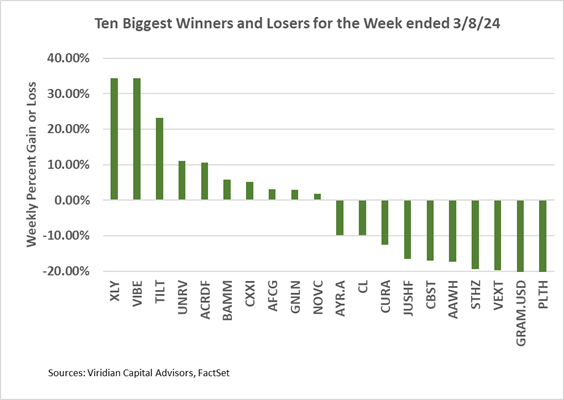

Best and Worst Performers of the last week and YTD: