OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

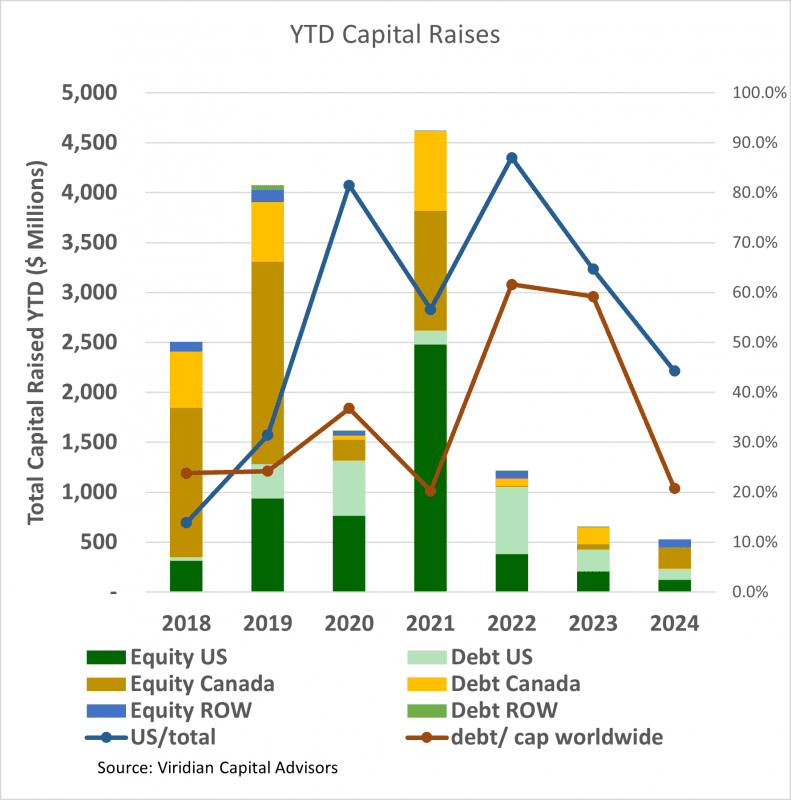

- The U.S. raises accounted for 44.3% of total funds, the lowest percentage since 2019. Conversely, raises from outside the U.S. and Canada, spurred by a sizeable psychedelic equity raise in the U.K., represented a historically high 14.7% of the total funds raised.

- YTD raises by public companies accounted for 76.4% of total funds.

VIRIDIAN INSIGHTS

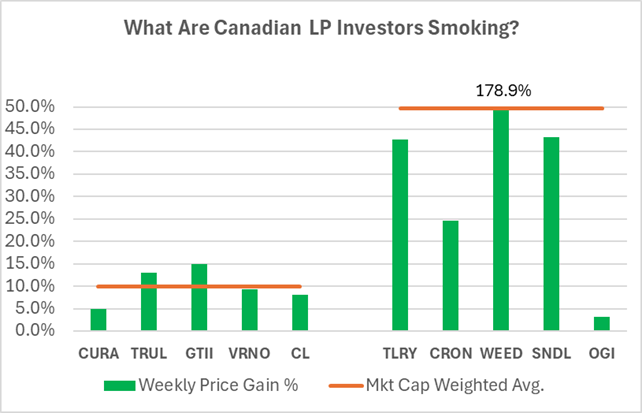

- AN IRRATIONAL RALLY IN CANADIAN LP STOCKS?

- We updated our chart from last week, showing the two-week percentage gain in the top five U.S. MSOs versus the top five Canadian L.P.s. There are three proximate causes for the intense rally in Canadian L.P.s:

- We went through the litany of potential causes for the difference last week, including increased hopes for U.S. legalization (low odds in the next five years, in our opinion), the results of the new report on cannabis laws in Canada (mild impact but largely disappointing), the legalization in Germany (a potential long term positive, however, the current form of the law is lacking on commercialization provisions, and the positive impacts are likely to, at best, take longer to play out than the headlines suggest). Conclusion positive but not spectacularly so)

- This week’s additional dose of positivity comes from new progress towards medical cannabis in France.

- So, we stick to our original conclusion: Canadian cannabis investors have been whittling away at the excess inventories of cannabis.

- The 178% two-week gain in Canopy Growth implies more of a use of psychedelics than cannabis. We learned that you can’t keep a good meme stock down, but is there a better short candidate than this?

- Florida’s Supreme Court Approved a ballot measure for a change to the State’s Constitution, which would allow for adult recreational use of cannabis.

- The measure must pass by a 60% supermajority to become effective, and various polls have it quite close. Ohio’s adult rec bill passed with a 57% approval rate. Ohio also benefitted from the presence of an abortion bill on the ballot, which is thought to have increased voter participation. The Florida Court also approved an initiative to let voters decide to amend the State’s Constitution to establish a right to an abortion.

- The Viridian Chart of the Week explored the potential impacts on companies levered to Florida and found that an adult recreational move could double several stocks.

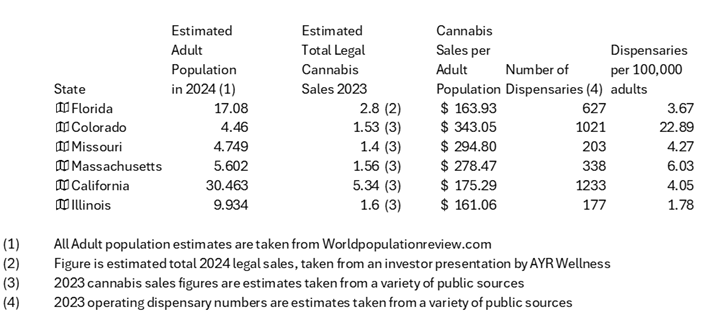

- The potential for an adult market in Florida is BIG! Industry rules of thumb generally call for a doubling of cannabis sales in a state that goes rec. But is this reasonable for Florida? The table below provides some key data points for analyzing the question.

-

-

- Florida’s sales per adult population are already in the middle of some established adult markets. Some observers believe Florida will more than double, perhaps as much as triple, if adult rec is approved.

- Support for more than doubling comes from looking at Colorado, which has 2.09x the spending per adult population. Could Florida go higher than that?

- One factor is tourism, which Florida and Colorado both gain from. Florida has the edge there.

- Another factor is demographics. Florida is older and more affluent than Colorado, which are both positive factors.

- Still, another factor is availability. The chart shows dispensaries per 100,000 adult population. Florida, at 3.67, is above some of the adult states but nowhere near Colorado. Edge goes to Colorado on that basis.

- Another factor is whether the state borders on non-adult legal states. That may be one factor for the strong numbers in Missouri, which appears to be second only to Colorado in sales per adult. Missouri benefits from cross-border sales from Illinois, an adult legal but higher-cost state, and Nebraska, Tennessee, and Kentucky, all illegal states. Florida’s situation in that regard is complex. On the one hand, it borders a large population and severely limited medical state of Georgia. On the other hand, many of Florida’s population centers and dispensaries are long drives from other states. Unclear how this factor will play out.

- Still another positive fact: Florida is one of the states that have recently cracked down on intoxicating hemp products, and that should be positive for adult recreational use.

- Even at a doubling, the Florida increase would by itself represent about 7% of 2024 cannabis sales. The measure would not go into effect until mid-2025 but would add significantly to industry growth.

-

- IMPERIAL BRANDS CONVERTS ITS $123M DEBT IN AUXLY TO EQUITY.

- Although ostensibly, this is a positive for Auxley, one has to question why Imperial would move from a debt position into an equity position in a company whose current price implies a C$9.89 valuation on the $123M debt.

- Auxly had previously negotiated an extension in the maturity of the notes from September 2024 to September 2026, more or less ensuring the company’s near-term solvency, but if you are Imperial, why not just bide your time and potentially negotiate a lower exercise price? After all, the $.81 exercise price is just a bit over the $.04 trading price!

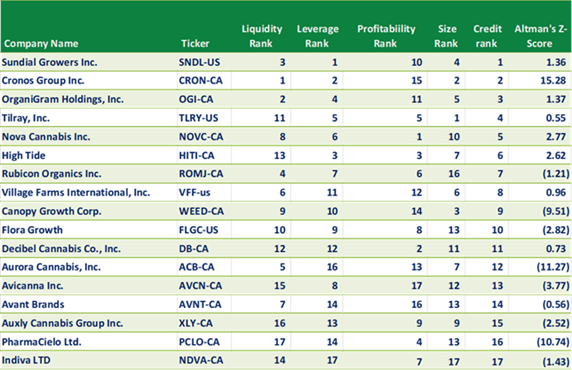

- We rank Auxly quite lowly as a credit even proforma for the debt reduction/conversion to equity from the deal. Below is a table of the Viridian Capital Credit Tracker rankings for the 17 Canadian cultivation and retail sector companies with market caps over US$10M. Our ranking is #15/17. The low liquidity ranking stems from a free cash flow adjusted current ratio of .75x, implying a need for additional capital during the year.

-

- One clue to Imperial’s intent might be the fact that in the latest extensions/amendments, Imperial eliminated the requirement to use Auxly as its sole cannabis supplier.

- Although Auxly’s stock rallied on the news, we view the conversion as a vote of no confidence. In the press release, imperial stated, “Imperial intends to review its investment in the Company on a continuing basis and may, subject to the terms of the A&R Investor Rights Agreement, purchase or sell Shares, either on the open market or in private transactions…”. Our trading days taught us that when a company says they may buy or sell, they generally mean SELL!!!. We interpret the conversion as a means to liquidate the position, albeit at a tremendous loss.

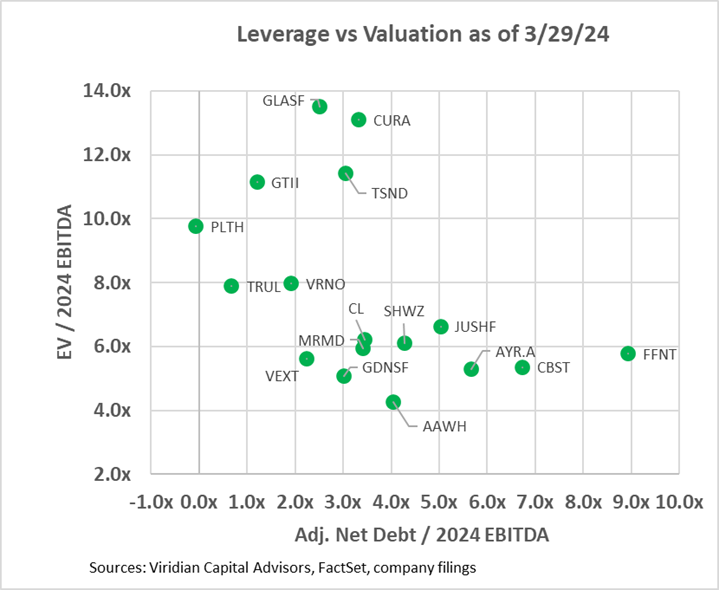

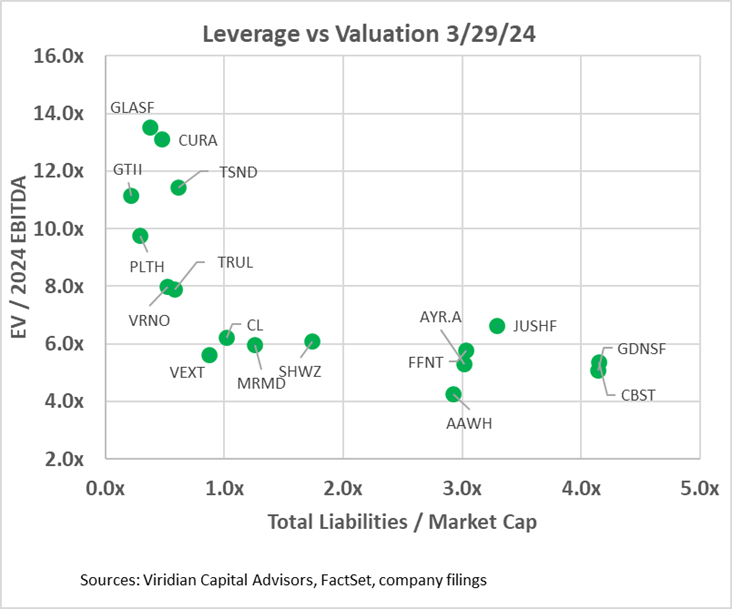

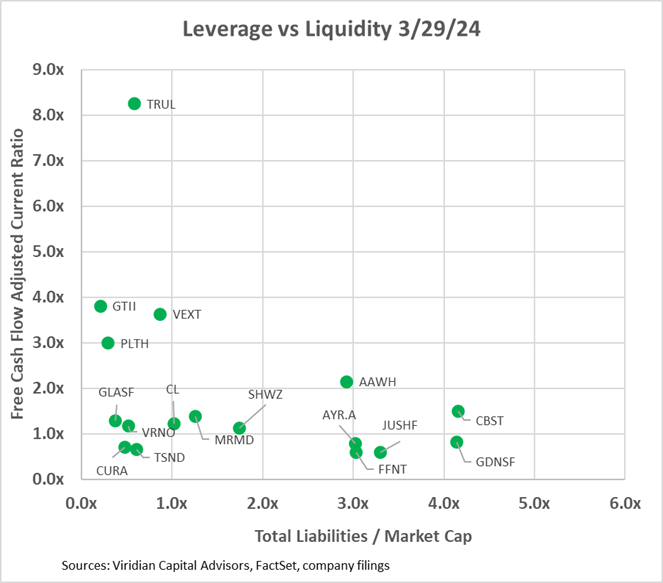

- VALUATION, LEVERAGE, AND LIQUIDITY

- The two graphs below show the Enterprise value to 2024 EBITDA multiples against two leverage measures. In the first graph, we have calculated an Adjusted Net Debt/ 2024 EBITDA figure by adding any accrued taxes over 90 days of tax expense to debt before subtracting cash to arrive at Adjusted Net Debt. We would expect any regular company to have accrued taxes equal to their last quarterly tax expense and consider that a standard working capital item. Several companies on the chart have far greater than 90 days of accrued taxes, and we consider the excess to be debt. Verano’s excess tax liabilities equal nearly 40% of its debt. Other companies with relatively high imputed tax debt include Curaleaf (CURA: CSE) and 4Front (FFNT: CSE) at 19%, and Terrascend (TSND: TSX) at 17%.

- The first graph shows that ten of the seventeen companies have net debt/ 2024 EBITDA over 3x, which we view as the cutoff of sustainability in a 280e world. We view 4x as sustainable in a post-280e environment, and five companies are now over that threshold.

- The second graph looks at leverage through the lens of total liabilities to market cap. This measure separates the companies into two groups that relate to the market’s belief of whether a company can discharge its liabilities without highly dilutive actions, like discounted stock sales or refinancing debt with a heavy warrant or share consideration.

- Companies that have too much debt but have low liabilities to market cap are candidates for stock sales or debt for equity exchanges. These companies include Cresco and TerrAscend. Alternatively, these companies may delever by using their high valuation to buy cash flow. TerrAscend spoke to this possibility on its earnings call.

- Goodness Growth is in precisely the opposite situation. It is not as levered as Curaleaf on an adjusted Debt to EBITDA basis. Still, its stock is trading at such low multiples that the prospect of issuing equity to reduce debt seems unlikely. This is why we anticipated an asset sale like today’s announced sale of the company’s New York licenses and properties.

- Jushi, AYR, Cannabist, and 4Front appear significantly overleveraged in both an EBITDA and Market Cap sense. However, each has some element of optionality that might prove 2024 EBITDA estimates too conservative. For Jushi, it is Pennsylvania and Virginia (although Virginia’s hopes are stymied for the time being by the governor’s veto of legislation that would open adult sales). For AYR, it is Florida. Cannabist is in Ohio, New York, Pennsylvania, and Florida. 4Front is levered to Illinois.

- The third graph introduces the free cash flow adjusted current ratio liquidity measure into the mix. Companies with less than 1x on this measure will likely have to raise capital next year. Six of the companies fall into this bucket.

- Looking at leverage in two ways and having a comprehensive measure of liquidity can give investors a good idea of possible scenarios for today’s overleveraged companies. Companies with low valuation metrics, high EBITDA, market cap basis leverage, and low liquidity include Jushi, 4Front, AYR, and Goodness Growth. Cannabist appears to have reasonable near-term liquidity; however, it is very highly levered and trading at discounted multiples.

-

-

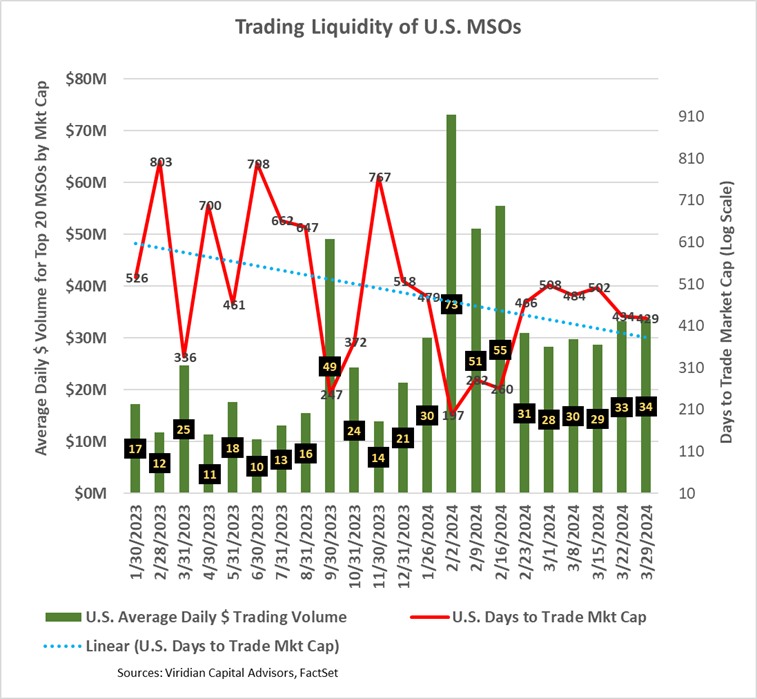

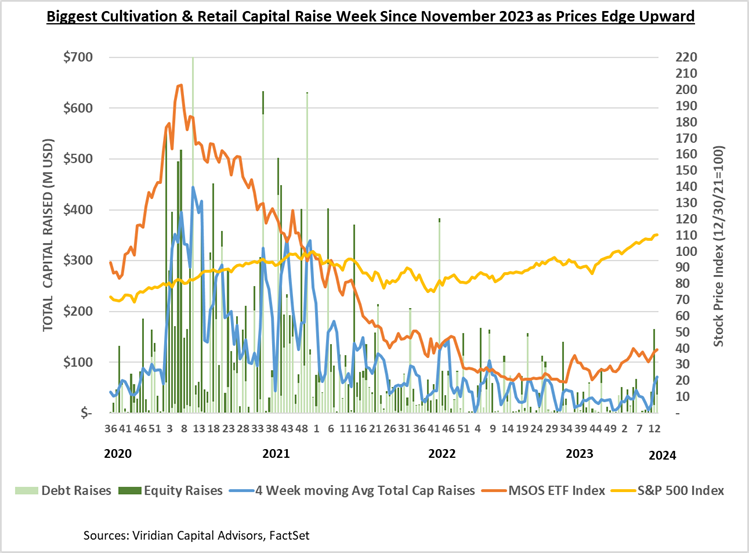

- CANNABIS STOCK LIQUIDITY FAILS TO REBOUND SIGNIFICANTLY DESPITE PRICE GAINS

- The Days to Trade Market Cap (DTTMC) series depicts the number of days it would take to trade the market cap of a stock or group of stocks. Its most recent reading of 429 days is above the downward trend line shown on the graph. A 429 DTTMC implies that an investor who acquired a 5% position in the stock, assuming he wanted to be less than 25% of the average daily dollar volume, would require 86 days to trade out of his position.

- The reality is that very little new institutional capital has come into the cannabis market. The investors are still the same, and many are not committing additional funds to the industry until some of the regulatory smoke clears. Will rescheduling change this? Perhaps, but not directly. Still, at the margin, the cash-flow-enhancing impacts of Schedule 3 will make cannabis more investible and attract more capital.

- CANNABIS STOCK LIQUIDITY FAILS TO REBOUND SIGNIFICANTLY DESPITE PRICE GAINS

-

-

-

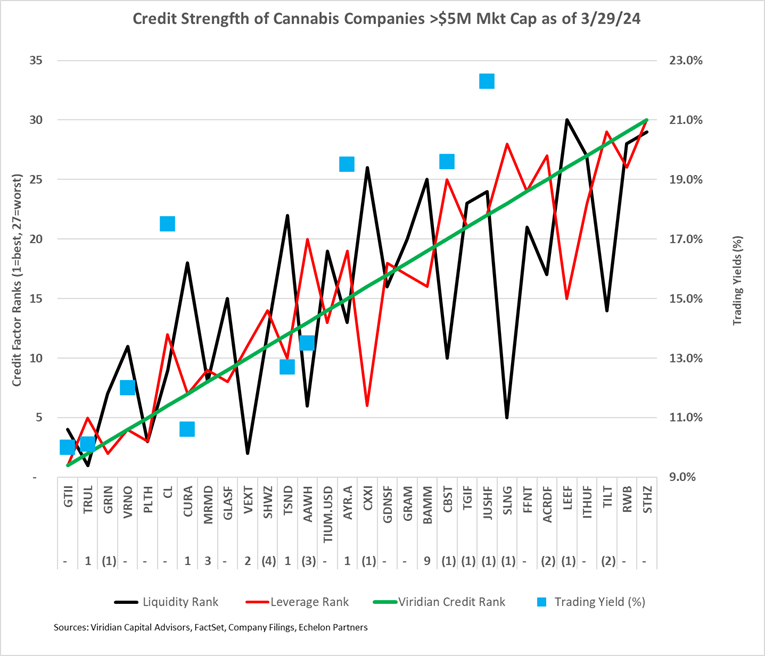

- GIVING CREDIT WHERE CREDIT IS DUE

- The chart below shows our updated 3/29/24 credit rankings for the 30 U.S. cannabis companies with over $5M market cap. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement.

- The blue squares show the offered-side trading yields for each company. Trading yields have declined significantly since the HHS rescheduling announcement.

- The rankings spread between Trulieve and Curaleaf held steady this week, with Trulieve gaining one spot to #2 and Curaleaf gaining one spot to #7

- Based on this week’s rankings, Curaleaf appears overvalued. It is trading nearly on top of GTI and Trulieve, which we believe are superior credits. Trulieve should trade at a bit wider spread to GTI. Cresco’s senior secured term debt continues to appear too cheap, so trading out of Curaleaf into Cresco seems like a good trade. Jushi’s debt has traded off, appropriately given the governor’s veto of adult rec in Virginia. AYR has significantly more leverage to a Florida rec event, and we believe it should trade at a lower yield relative to Cannabist.

- GIVING CREDIT WHERE CREDIT IS DUE

-

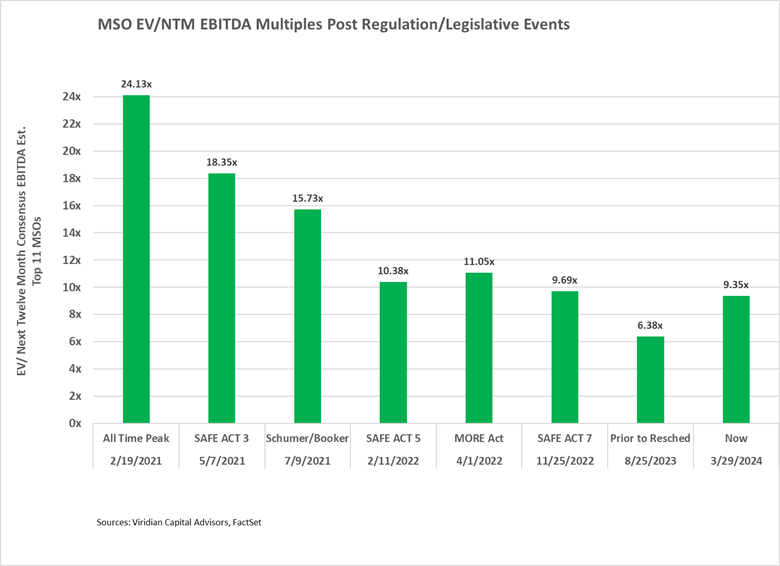

- THERE IS STILL CONSIDERABLE UPSIDE POTENTIAL

- The chart below shows enterprise to next-twelve-month valuation multiples now compared to previous times when positive regulatory/legislative news hit.

- The chart demonstrates a healthy investor skepticism regarding positive regulatory/legislative events in Washington, DC.

- EV/NTM EBITDA Multiples were up sharply this week and are now 11.0% below the levels after the 5th SAFE Act passage in the House in February 2022. Still, the rescheduling news is more significant as it dramatically impacts cash flows. If valuations multiples rose to where they were after the announcement of the Schumer-Booker bill, the incremental gains would equal 68.2%. We view a DEA announcement ratifying the HHS recommendation to be much more significant than introducing the Schumer-Booker bill, which most observers viewed as DOA and had no immediate impact on operator cash flows. Accordingly, we believe there is considerably more runway for price increases, perhaps reaching the 5/7/21 multiples of 18.35x, producing 96.25% returns from current levels.

- We also note, however, that the downside risk from an adverse DEA announcement has grown. If Schedule 3 were to go away (unlikely but possible) totally, we would expect stocks to go back to at least as low as they were before the HHS announcement, and this would imply a 31.7% loss. We think the downside could be a bit more.

- Probability weighting seems like a reasonable approach here, however subjective it may be. We ascribe a 60% chance of a positive DEA announcement that boosts stocks by 68%, a 20% chance of a doubling, and a 20% chance of a loss of 50%. The expected gain from this is approximately positive 51%.

- Cannabis equities (as measured by the MSOS ETF) were up 4.05% for the week.

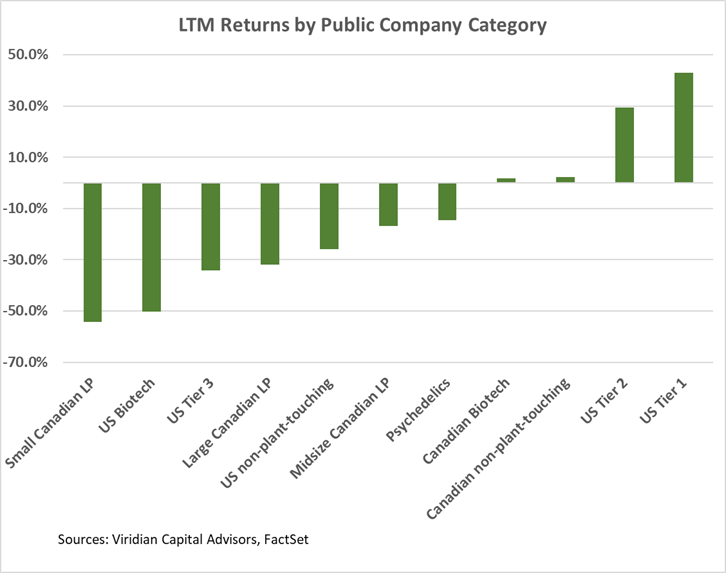

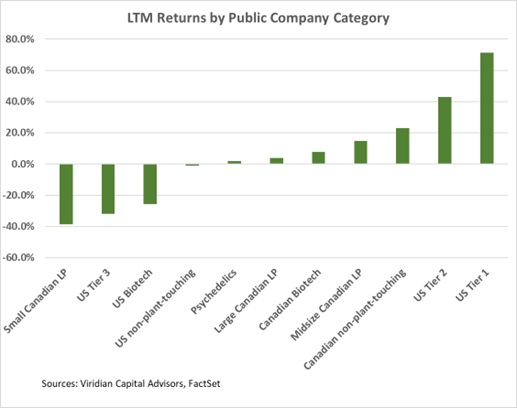

Trailing 52-Week Returns by Public Company Category:

- U.S. Tier One MSOs are now up over 70% for the LTM period, and Large Canadian L.P.s have snuck into positive territory for the first time this year based on the outsized gains over the last two weeks. Canopy Growth is still down 55% for the period despite its 178% gain over the previous two weeks.

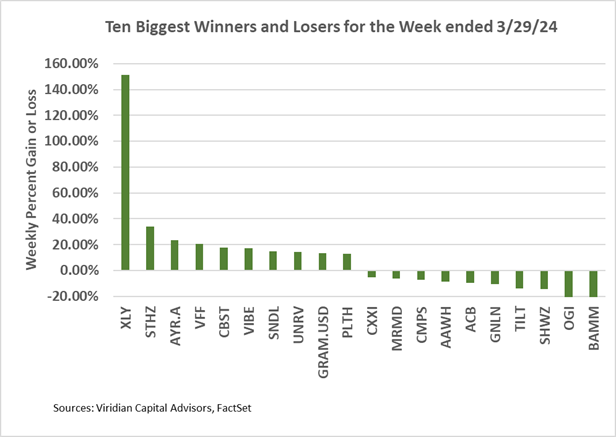

Best and Worst Performers of the last week and YTD:

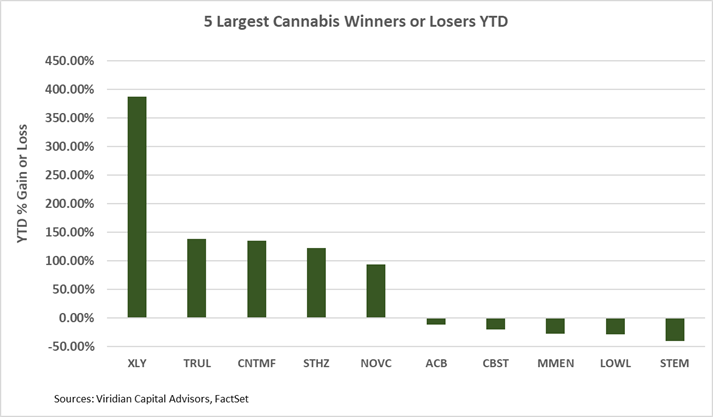

- Trulieve and Cansortium are the top gainers YTD with over 100% increases. Both would be beneficiaries from Florida Adult Rec., but we think the potential is still much higher, potentially another doubling, without 280e relief! See our Chart of the Week and analysis above for our reasoning.

- Auxly (XLY: TSX) tops the weekly gainer list on news that it converted a $123M Imperial Brands debt position into equity. We are not convinced the event represents the vote of confidence that the market perceives. See our INSIGHTS section for more analysis. California figured as a common factor in several of the other gainers, including StateHouse (STHZ: OTC), Vibe (VIBE: CSE), and Gold Flora (GRAM.USD: CSE).