OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

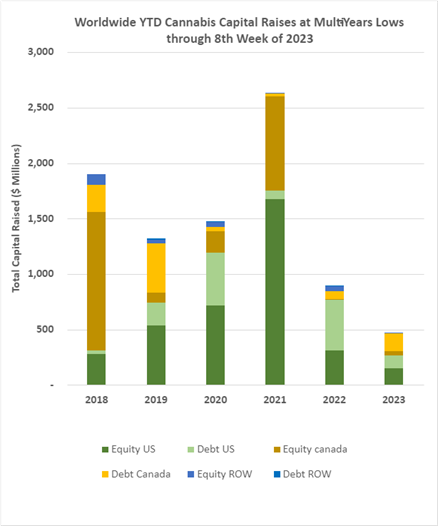

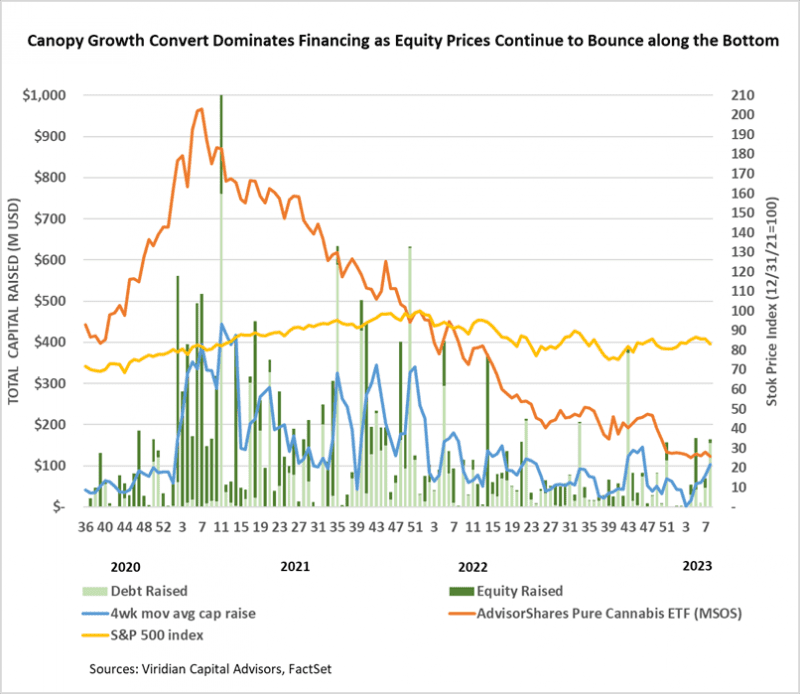

Cannabis capital raises are off to a multi-year low. Only $475.96M has closed through the first eight weeks of the year compared to $894.46M last year.

- Public companies have raised only 72.4% of total capital YTD, down from 79.4% last year.

VIRIDIAN INSIGHTS

- This week’s Canopy Growth (CGC: Nasdaq), convertible debenture issue, and recent transactions by Tilt Holdings and MariMed make it clear that the cost of debt is rising. Treasury rates and cannabis risk premia are up significantly, and companies are hard-pressed to pay the required returns in cash. One result is a reversal in the trend toward straight non-equity-linked debt. In 2019, approximately 80% of all cannabis debt issues were equity-linked, but this had fallen to around 5% by 2022. We also see other mechanisms for cranking up the IRR of debt deals like OIDs, mandated premiums at maturity, and various fees. Viridian attempts to explicitly value these options and features to arrive at an actual effective cost of debt.

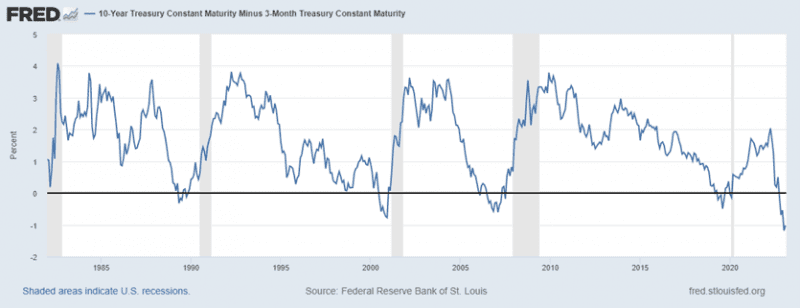

- The 3-month vs. 10-year treasury spread inversion narrowed about six basis points to negative 96bp, but it is still the most pronounced inversion since 1981. We like to watch this spread as opposed to the more commonly monitored 2yr-10yr spread for two reasons: 1) it is the measure that the Fed focuses more attention on, and 2) this measure does a better job of mirroring bank lending economics. This inversion has successfully predicted the previous five recessions, and we don’t think it will miss this time either. Investors have slowly realized that the Fed is not about to pivot anytime soon since it considers inflation quite ingrained and sticky. The chart below makes it clear that in virtually every case, the yield curve will begin to steepen before the onset of the recession.

- Arguably, cannabis is already in a recession, at least in many developed markets where profitability has been sapped by commodification-driven wholesale price declines exacerbated by inflation-driven cost increases. We continue to hear pundits bemoan the “race to the bottom” of pricing as though competitors in an agricultural commodity-based business have many choices. Unfortunately, we believe this is not a temporary condition but a sign of things to come. Retailers continue to tell us that their customers are primarily concerned with price and THC content, which spells commodity. It’s another reason why we consider federal legalization and the eventual interstate commerce it will bring to be the industry’s most significant long-term risk factor.

- This week BDSA predicted that the size of the legal cannabis market would increase from $32B in 2022 to nearly $60B by 2027, which seems like a bold prediction given the sharp contractions we have seen recently in the mature state markets like California, Colorado, Oregon, and Nevada. The forecast depends on converting illegal to legal sales primarily in newly developed markets like New Jersey, New York, Missouri, and states yet to turn on the adult use spigot. Luckily there are still enough new markets to be opened to maintain cannabis’ status as one of the world’s fastest-growing industries for at least the next five years. Commodity price pressures, however, are not going away. The battle for increased legal usage against likely continued price compression will determine how much growth is realized.

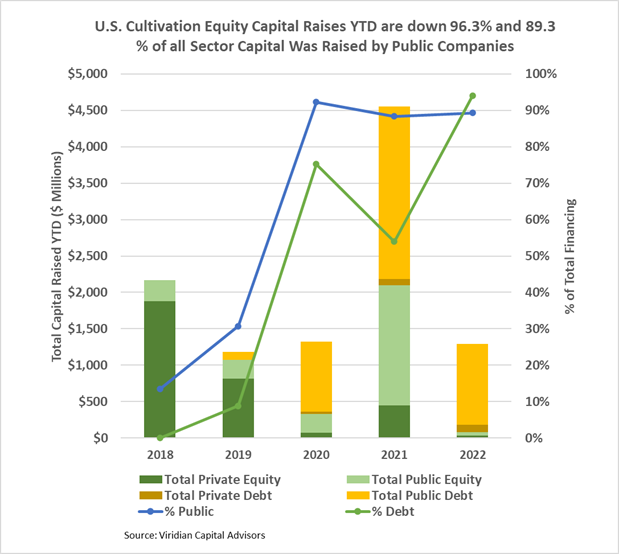

The U.S. Cultivation & Retail sector capital raises are down 71.6% YTD, but equity capital raised is down approximately 96.3%:

- Debt financing is down 50.6% YTD but accounts for about 94.0% of all capital raised; private companies raised 8.7% of it.

- 89.3% of total capital raises YTD were completed by public companies compared to 88.4% in 2021.

- In 2022, there have been no equity deals above $25M.

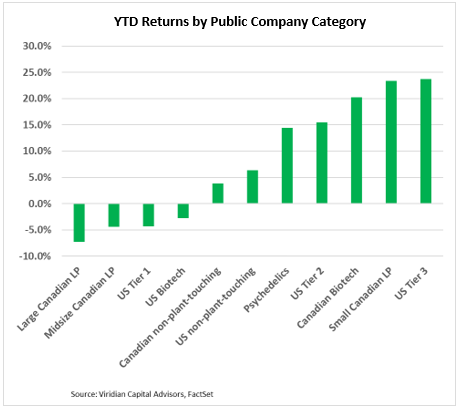

YTD Returns by Public Company Category

- Large Canadian LPs are still the worst-performing category in YTD returns, registering high single-digit weekly losses led by an 8.7% decline for Cronos Group (CRON: Nasdaq). Cronos dropped an additional 4% today after reporting lackluster earnings. The company’s market cap is now below its cash level. Four of our eleven public company categories are trading at negative YTD returns.

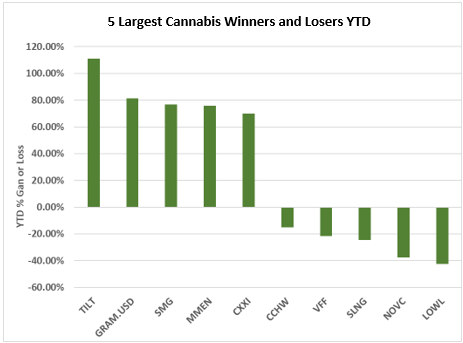

Best and Worst Performers of the last week and YTD