OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

VIRIDIAN INSIGHTS

- GERMANY’S PARLIAMENT APPROVED A BILL TO LEGALIZE CANNABIS NATIONWIDE.

- The bill will legalize possession and home cultivation and will authorize social clubs to distribute cannabis to members.

- The 407-226 vote was a bit of a surprise, given the polling stats that show Germans only marginally support legalization.

- Still, as passed, the law is a significant step backward from full legalization. The bill leaves out commercial cultivation and sales provisions, significantly limiting the potential commercial opportunities in the German adult rec business.

- CHICAGO ATLANTIC AND SILVER SPIKE, TWO OF THE LARGEST CANNABIS LENDERS, JOINED FORCES

- The deal calls for Chicago Atlantic to sell approximately $130M of cannabis loans to Silver Spike’s BDC in exchange for most of the BDC, which will be renamed Chicago Atlantic. In doing so, Chicago Atlantic will gain access to permanent capital, as BDCs, unlike private debt funds, have no mandated return of capital to their investors. Silver Spike, in return, will gain access to Chicago Atlantic’s more highly developed back office, origination staff, and capital-raising operations.

- The two lenders have competed for deals and become joint lenders on several. They were more partners than competitors anyway, but now it is official.

- FIRST CITIZENS BANK BECOMES THE LARGEST BANK TO JUMP INTO CANNABIS

- The 19th biggest bank in the country, with over $200B in assets, unexpectedly announced that it will begin to service the cannabis industry.

- Regional banks have made several modest-sized cannabis loans over the last year at eye-popping rates.

- First Federal Bank lent Trulieve $25M at 8.31 in December 2023. Trulieve is generally considered one of the top credits in the industry.

- MariMed received a $58.7 million loan in November 2023 at 8.43% from an 8.43% from an unnamed insured bank.

- Needham Bank lent AYR $40M at 8.26% in November 2023, while the company’s public bonds traded at distressed levels.

- TerrAscend received a $25M loan at 10.25% from Stearns Bank in June 2023

- FVC Bank lent Jushi $20M at 8.25% in April 2023, while the company’s public bonds traded around 20%

- The common theme is that the rates have little to do with the corporate credit quality, and the loan sizes have little to do with the size of the cannabis companies. In short, these are not corporate cash flow loans but project loans. The rates represent attractive spreads to the bank’s cost of funds, and the loans are well secured by mission-critical collateral. Potentially a threat to sales leaseback providers but hardly a general solution to cannabis credit.

- The banks may have played for more than the loan business. The regional banks most likely locked in low-cost deposit funds by requiring borrowers to subscribe to cash management services.

- Does the fact that a $200B+ lender is now getting involved signal an acceleration of the trend? Do they know something we don’t? Yes, and maybe. One key is that Citizens is controlled by a family that doesn’t need to fear blowback from investors or shareholders. Another key is that while they are the 19th biggest bank in the country, there is still a quantum leap from them to the trillion dollar giants like JP Morgan.

- Will the Giants step in? We continue to have doubts that the likes of JP Morgan will jump into cannabis lending. For one, the industry is too small to move the needle for a trillion-dollar bank. We do not doubt that JP Morgan will vie to underwrite GTI junk bonds when the time is right, but we don’t see them spending the time to get up the curve to making the kinds of loans we highlighted above.

- Will Bank lending become important? One type of bank loan might make an enormous difference for cannabis. Most U.S. corporations do not derive “rainy day” liquidity by holding cash on their balance sheets. Instead, they have standby revolving credits typically backed by working capital. Cannabis companies, on the other hand, do not have these loans available to them, and to assure liquidity for eventualities like crop failures or the like, they need to maintain large cash balances. Access to standby lines will be a sign that cannabis has finally achieved legitimacy, but that is not yet on the table.

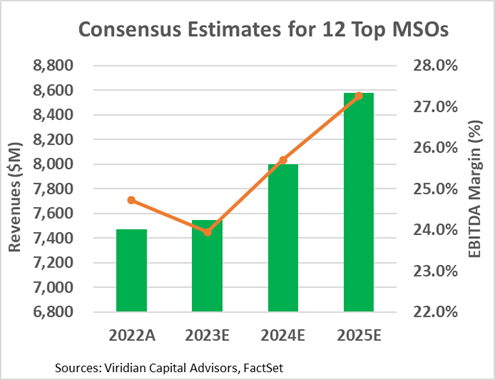

- ANALYSTS MAY BE UNDERSHOOTING ON 2024 EBITDA PROJECTIONS.

- The chart below shows consensus revenue and EBITDA margin estimates for the top twelve MSOs.

- Analysts may be too cautious with the group’s 2024 revenue growth projection of 6.0%. A year of Maryland and Ohio and near-term price stability in several key markets suggests a higher growth expectation may be in order.

- Similarly, we believe the 25.7% 2024 consensus EBITDA margins may be too low as they are only 100bp higher than the 2022 figures. The industry found religion in 2022 and 2023, stringently managing costs and tightening working capital controls. The industry is poised to be more efficient and profitable as growth returns.

- A Careful Look at EBITDA and Market leverage and a liquidity review suggest likely courses of action for some overleveraged MSOs.

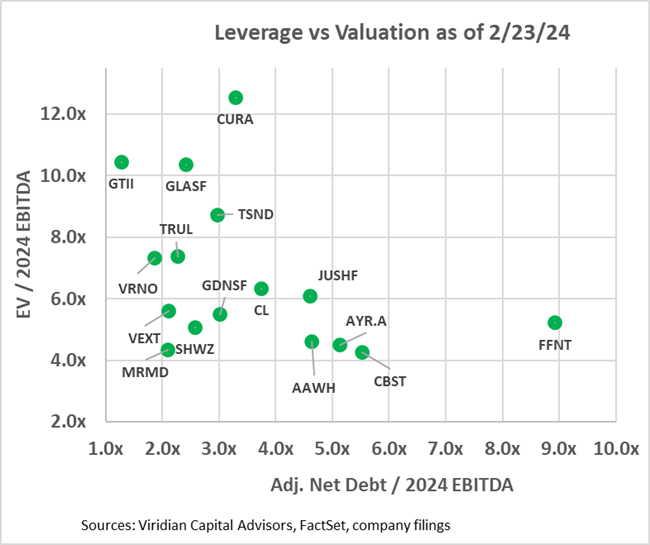

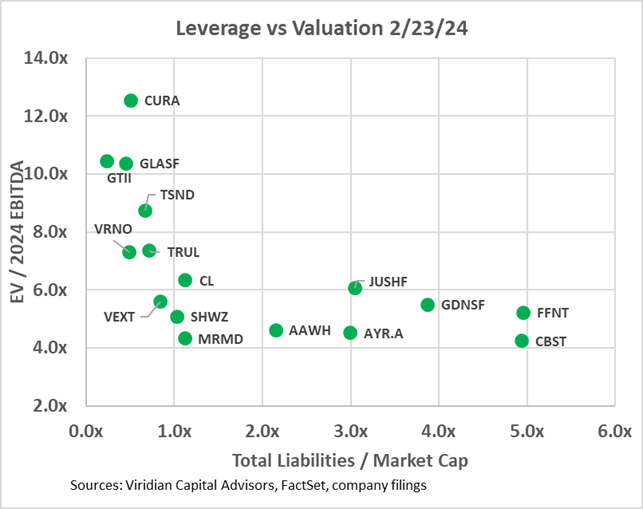

- The two graphs below show the Enterprise value to 2024 EBITDA multiples against two leverage measures. In the first graph, we have calculated an Adjusted Net Debt/ 2024 EBITDA figure by adding any accrued taxes over 90 days of tax expense to debt before subtracting cash to arrive at Adjusted Net Debt. We would expect any regular company to have accrued taxes equal to their last quarterly tax expense and consider that a standard working capital item. Several companies on the chart have far greater than 90 days of accrued taxes, and we consider the excess to be debt. Verano’s excess tax liabilities equal nearly 40% of its debt. Other companies with relatively high imputed tax debt include Curaleaf (CURA: CSE) and 4Front (FFNT: CSE) at 19%, and Terrascend (TSND: TSX) at 17%.

- A comparison of the two top graphs is instructive. Some companies like TerrAscend, Goodness Growth, and Curaleaf appear to be directly on or slightly over 3x adjusted net debt to EBITDA, which we view as the demarcation line of long-term sustainability.

- TerrAscend and Curaleaf have relatively low total liabilities to market cap because the market is valuing their stocks at such high multiples. These companies should issue equity at these high multiples to directly fund debt reduction or use equity to purchase another company and increase EBITDA. An acquisition of one of the companies trading at much lower EBITDA multiples is likely to be accretive.

- Goodness Growth is in precisely the opposite situation. It is not as levered as Curaleaf on an adjusted Debt to EBITDA basis. Still, its stock is trading at such low multiples that the prospect of issuing equity to reduce debt seems unlikely. Goodness Growth will likely have to sell assets or sell itself to work out of its overleveraged situation.

- Jushi, AYR, Cannabist, and 4Front appear significantly overleveraged in both an EBITDA and Market Cap sense. However, each has some element of optionality that might prove 2024 EBITDA estimates too conservative. For Jushi, it is Pennsylvania and Virginia. For AYR, it is Florida. Cannabist is in Ohio, New York, Pennsylvania, and Florida. 4Front is levered to Illinois.

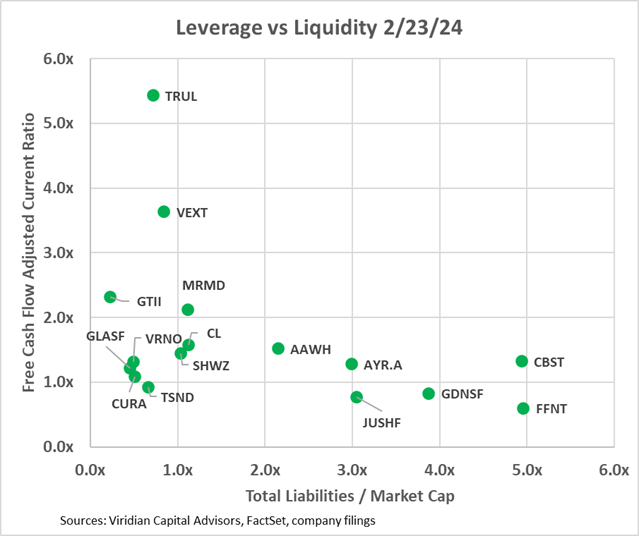

- The third graph shows that AYR and Cannabist have better liquidity than Jushi or 4Front and are less likely to need to push a highly dilutive equity deal or expensive debt deal into the market.

- Looking at leverage in two ways and having a comprehensive measure of liquidity can give investors a good idea of possible scenarios for today’s overleveraged companies.

-

-

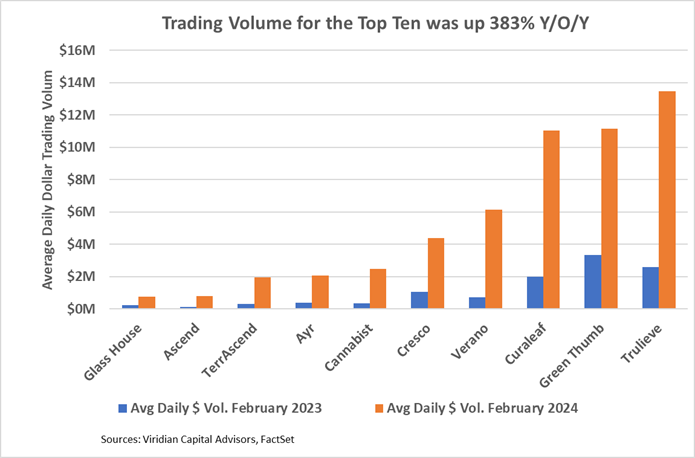

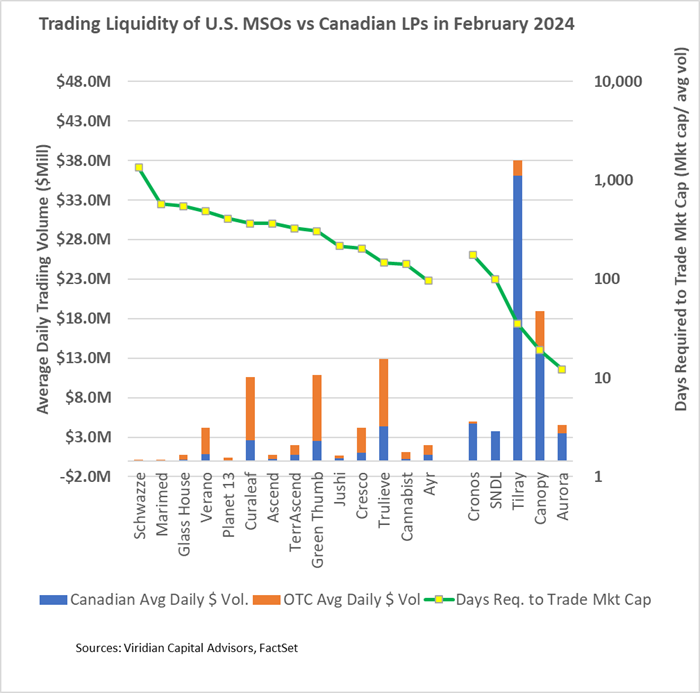

- CANNABIS STOCK LIQUIDITY JUMPED IN FEBRUARY 2024 vs 2023

- The first graph below shows the striking 383% increase in average daily dollar volume for the top ten trading MSOs in February 2024 compared to February 2023. The volume was influenced by the MJUS ETF portfolio rebalancing we discussed in a recent Viridian Chart of the Week. Still, the gains are too significant to ascribe to only that event. The drumbeat for a DEA rescheduling announcement is driving increased trading.

- The second graph shows the average daily dollar volume of the MSOs and Canadian L.P.s. The bars show each company’s average daily dollar volume combined between primary and secondary exchanges. The green line (measured on the right axis) shows the aggregate Days to Trade the Market Cap. (DTMC). Some of the MSOs are trading with greater liquidity than some of the L.P.s. The most liquid US MSO on a DTMC basis is AYR at 96 days, which is beginning to become acceptable for institutional investors. As an illustration, if an investor took a 5% position in a stock with a 96 DTMC and wanted not to be over 25% of the average daily trading in the stock (so as not to disturb the market), it would take him 19 days to trade out of his position. The equivalent calculation for Tilray is seven days, illustrating the importance of up-listing.

- CANNABIS STOCK LIQUIDITY JUMPED IN FEBRUARY 2024 vs 2023

-

-

-

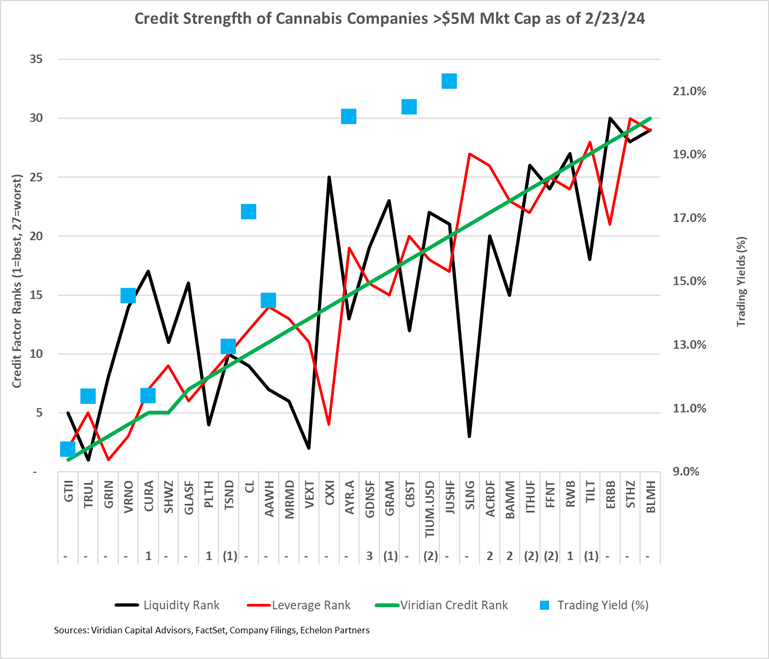

- GIVING CREDIT WHERE CREDIT IS DUE

- The chart below shows our updated 2/23/24 credit rankings for the 30 U.S. cannabis companies with over $5M market cap. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement.

- The blue squares show the offered-side trading yields for each company. Trading yields have declined significantly since the HHS rescheduling announcement.

- AYR, Cannabist, and Jushi are now trading at yields consistent with our relative credit rankings.

- GIVING CREDIT WHERE CREDIT IS DUE

-

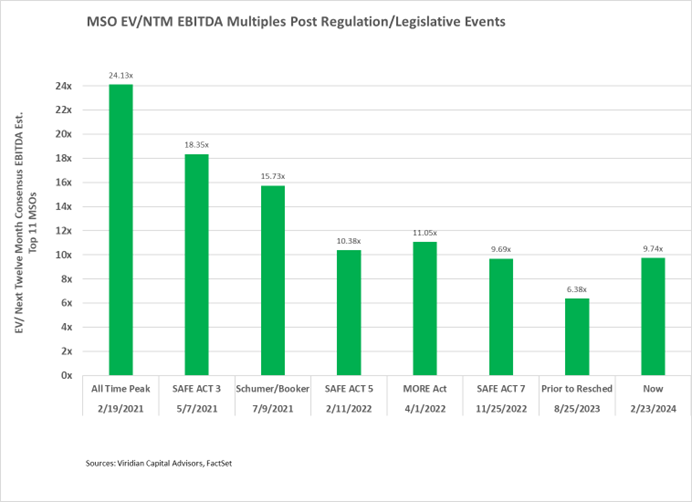

- THERE IS STILL CONSIDERABLE UPSIDE POTENTIAL

- The chart below shows enterprise to next-twelve-month valuation multiples now compared to previous times when positive regulatory/legislative news hit.

- The chart demonstrates a healthy investor skepticism regarding positive regulatory/legislative events in Washington, D.C.

- EV/NTM EBITDA Multiples are now 6.1% below the levels after the 5th SAFE Act passage in the House in February 2022. Still, the rescheduling news is more significant as it dramatically impacts cash flows. If valuations multiples rose to where they were after the announcement of the Schumer-Booker bill, the incremental gains would equal 61.5%. We view a DEA announcement ratifying the HHS recommendation to be much more significant than introducing the Schumer-Booker bill, which most observers viewed as DOA and had no immediate impact on operator cash flows. Accordingly, we believe there is considerably more runway for price increases, perhaps reaching the 5/7/21 multiples of 18.35x, producing 88.4% returns from current levels.

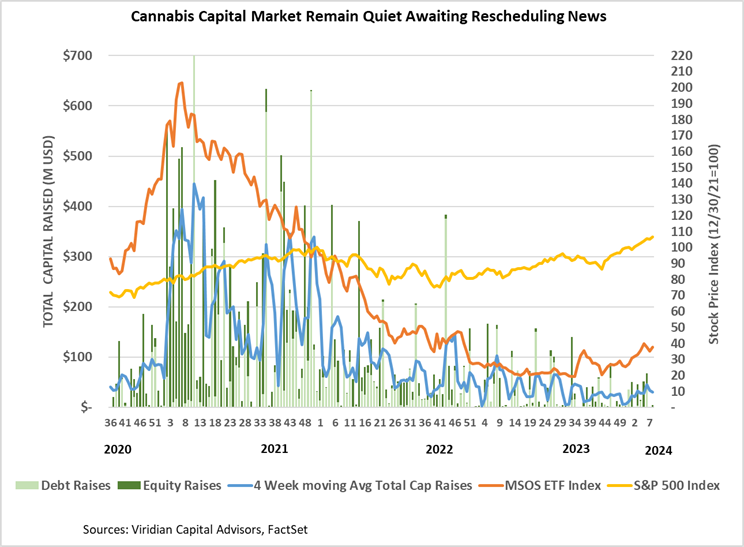

- Cannabis equities (as measured by the MSOS ETF) were up 6.77% for the week as investors gear up for 4th quarter earnings releases beginning this week.

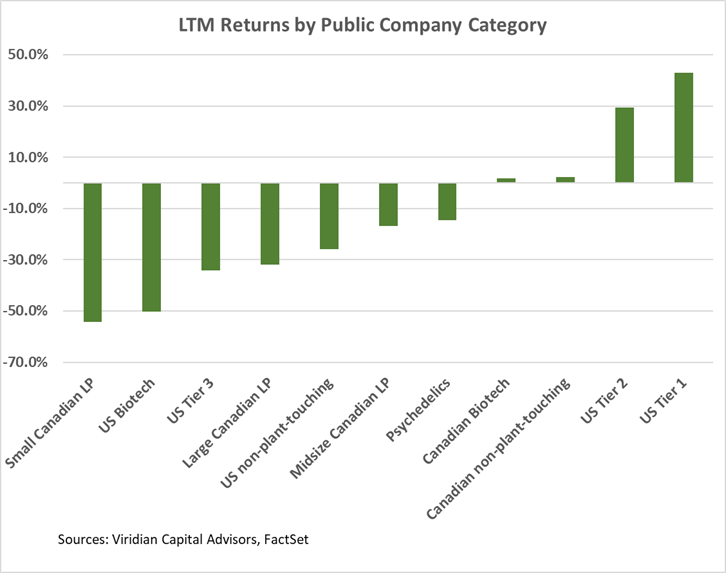

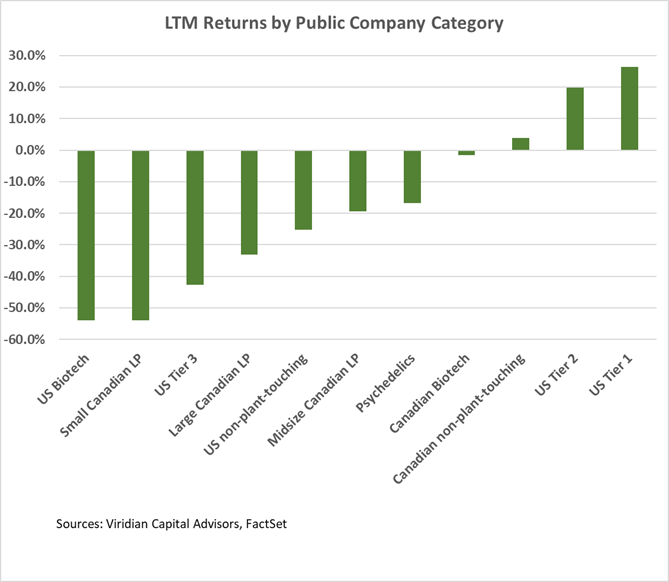

Trailing 52-Week Returns by Public Company Category:

- Unsurprisingly, U.S. Tier One MSOs continue performing best out of our eleven categories, with Tier Two MSOs close behind.

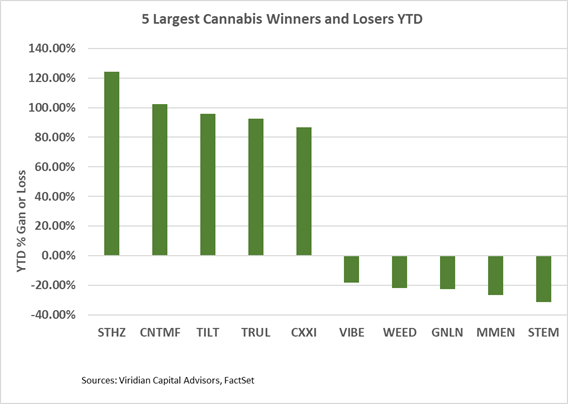

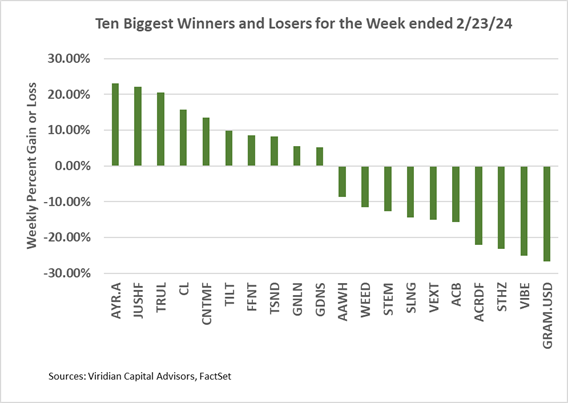

Best and Worst Performers of the last week and YTD:

- Gainers were all in our credit rankings’ mid to lower tiers except for Trulieve.

- Losers include names levered to a rescheduling announcement, including AYR, Cannabist, Cresco, Jushi, and 4Front.