OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

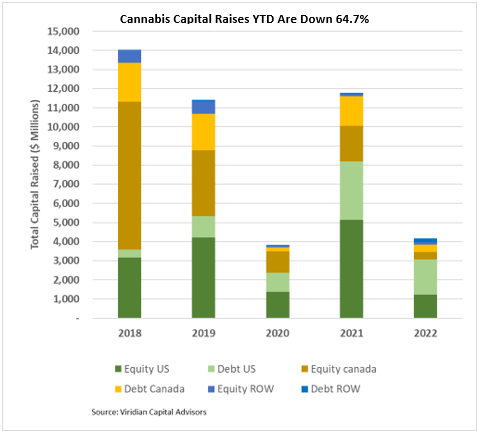

Cannabis capital raises are off 64.7% YTD:

- Total Equity issuance is off 75.6%, and total debt issuance is down 47.8%.

- U.S. debt is down only 39.3%, while Canadian debt is down a more significant 75.6%.

- At 58.2% of total capital raised, debt remains the highest in history for comparable periods.

- Public companies accounted for 74.5% of total financing YTD, down from 79.6% in 2021.

- The graph below shows that U.S. activity dominated capital raises for the first forty-nine weeks of 2022, with 74.0% of all capital raised.

- International capital raises of $319.8M represented 7.7% of total capital raises, exceeding the previous record of 6.3% in 2019.

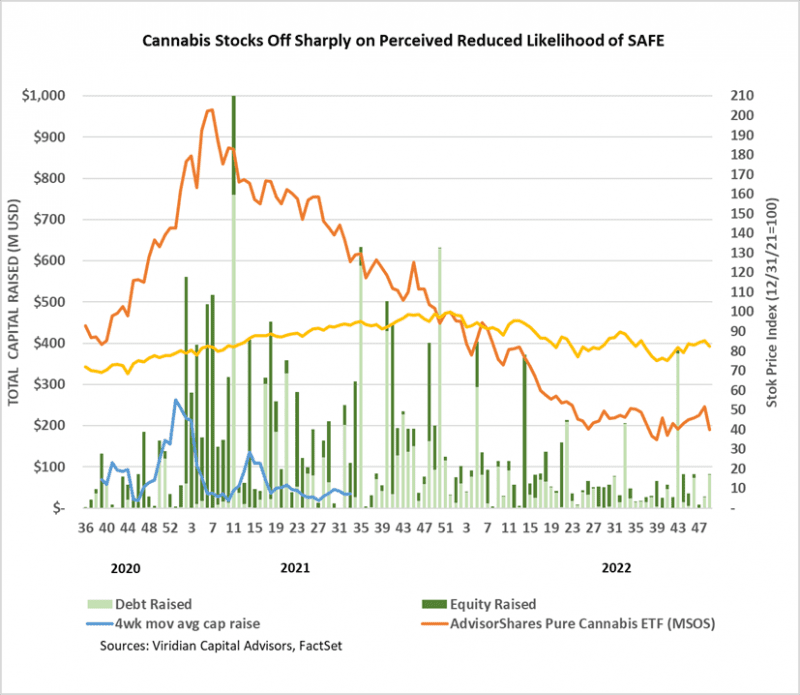

The U.S. Cultivation & Retail sector has experienced a similar change in capital raise activity, although the components have changed significantly.

- Total capital raised is down 62.3%, but equity capital raised is down approximately 95.0%.

- Debt financing is down 30.0% YTD but accounts for about 93.5% of all capital raised; private companies raised 24.9% of it.

- 73.0% of total capital raises YTD were completed by public companies compared to 80.9% in 2021.

- In 2022, there have been no equity deals above $25M.

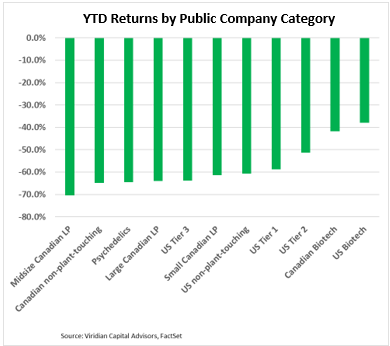

YTD Returns by Public Company Category

- Interestingly, Tier 3s, the category that stood most to gain from SAFE, actually gained one notch of improved ranking in terms of YTD returns. We chalk this up to illiquidity, which can be a blessing in a free-falling market like we saw this week.

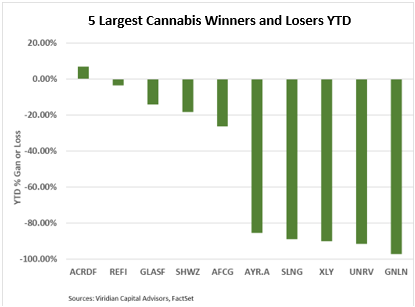

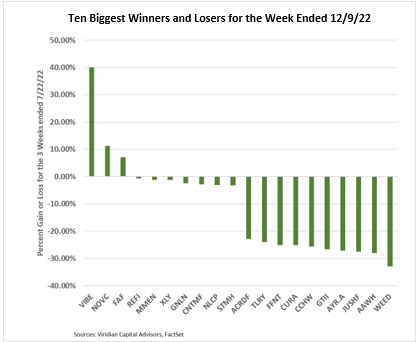

Best and Worst Performers of the last week and YTD

- Top gainers this week are from three categories: 1) the dawned of the dead, including Nova Cannabis (NOVC: CSE), Fire & Flower (FAF: CSE), MedMen (MMEN: CSE), and Greenlane (GNLN: Nasdaq), all among the largest YTD losers; 2) Loan providers Chicago Atlantic (REFI: Nasdaq) and New Lake Capital (NLCP: OTCQX) both of which stand to gain from the failure of SAFE; and Vibe Growth (VIBE: CSE) which gained 40% last week on the news of a company share buyback, only to trade back down 29% over the last two days.

- Top losers included a selection of the largest and most liquid names in cannabis, including Canopy Growth (WEED: TSX), Ascend (AAWH: OTCQX), Green Thumb (GTII: CSE) and Curaleaf (CURA: CSE), all victims of their own liquidity.