OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

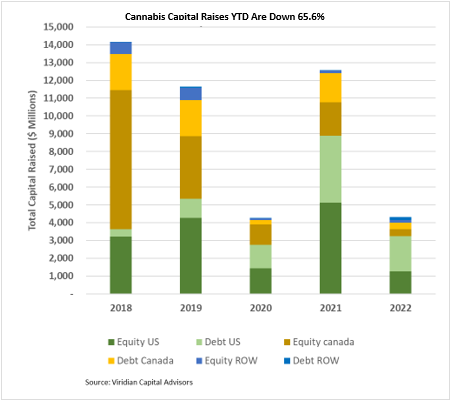

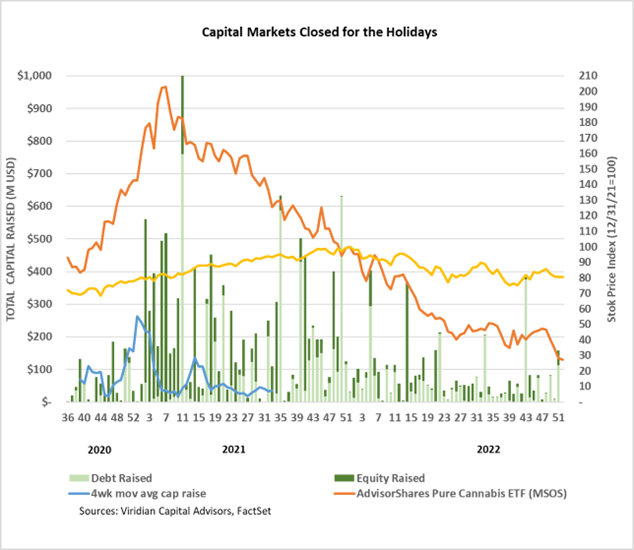

Cannabis capital raises for 2022 were down 65.6% from 2021:

- Total Equity issuance is off 75.0%, and total debt issuance is down 53.1%.

- U.S. debt is down only 47.4%, while Canadian debt is down a more significant 76.4%.

- At 58.7% of total capital raised, debt remains the highest in history for comparable periods.

- Public companies accounted for 75.4% of total financing in 2022, down from 80.8% in 2021.

- The graph below shows that U.S. activity dominated capital raise in 2022, with 74.7% of all capital raised.

- International capital raises of $319.8M represented 7.4% of total capital raises, exceeding the previous record of 6.4% in 2019.

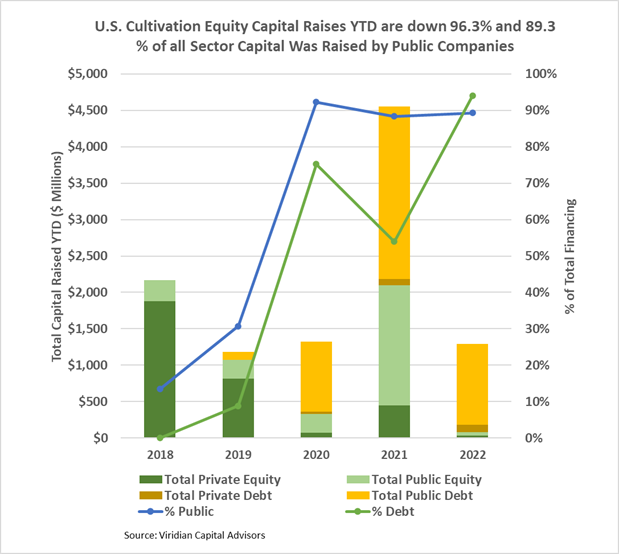

The U.S. Cultivation & Retail sector capital raises are down 71.6% YTD, but equity capital raised is down approximately 96.3%.

- Debt financing is down 50.6% YTD but accounts for about 94.0% of all capital raised; private companies raised 8.7% of it.

- 89.3% of total capital raises YTD were completed by public companies compared to 88.4% in 2021.

- In 2022, there have been no equity deals above $25M.

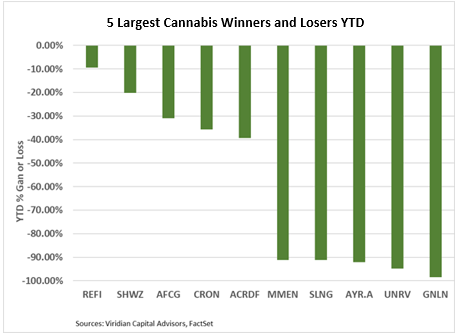

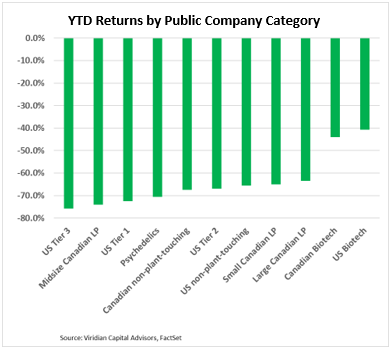

YTD Returns by Public Company Category

- Tier 3s, the category that stood most to gain from SAFE, lost another notch of ranking in terms of YTD returns. Investors are rightfully concerned about the liquidity of smaller companies in the No SAFE capital crunch environment. Ironically, the large Canadian LPs, with among the most disastrous financial statements of all the categories in the graph, outperformed in 2022. For obvious reasons, the best performer was Cronos (CRON: Nasdaq): 91.2% of the company’s market cap is its cash hoard of nearly $900M. We have been critical along the way, but in retrospect, cash has been a better investment than cannabis operations by a wide margin.

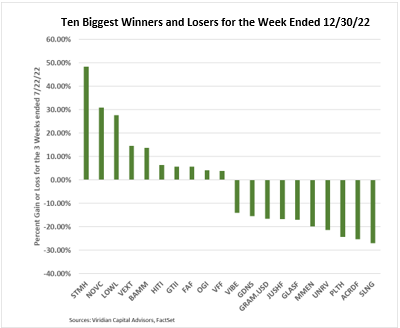

Best and Worst Performers of the last week and YTD

- Nova Cannabis (NOVC: CSE) continued to rally on the news of its joint venture with Sundial. Vext (VEXT: CSE) repeated its showing on the winner’s list for what we ascribe to either M&A speculation or the realization that some of the smaller players will be sustainable even in the no SAFE environment.

- Top losers included California heavy operatorsMedMen (MMEN: CSE).Glass House (GLASF: OTC), TPCO (GRAMF: OTC), and Unrivaled Brands (UNRV: OTC). The realization is that no legislative action will be forthcoming to rescue the disastrous California cannabis economics. We view Glass House as the best hedge against interstate commerce, but this is not a risk at the top of most investors’ minds.