OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

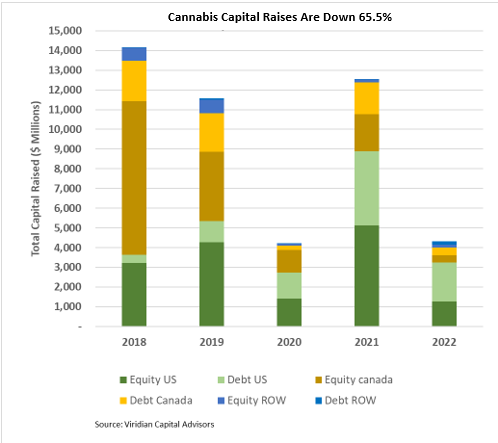

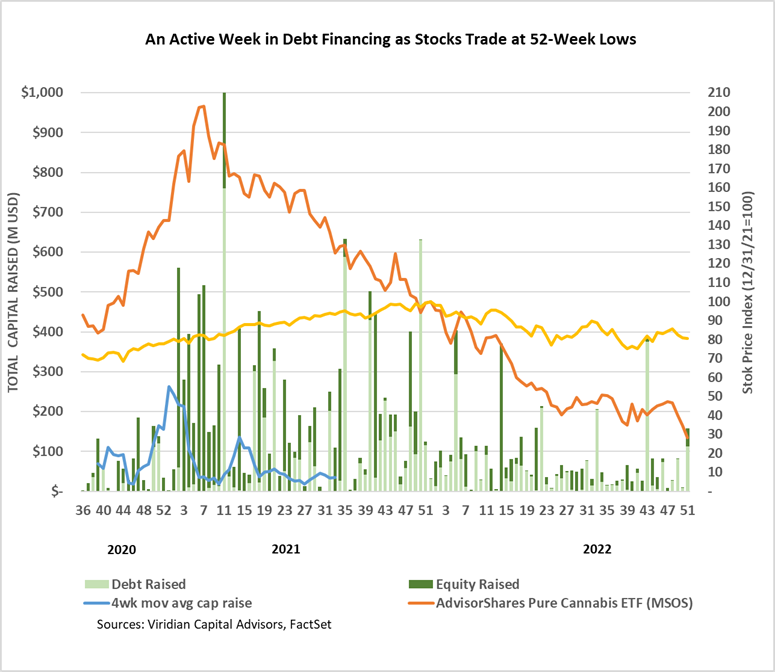

Cannabis capital raises are off 65.5% YTD:

- Total Equity issuance is off 75.0%, and total debt issuance is down 52.8%.

- U.S. debt is down only 47.4%, while Canadian debt is down a more significant 76.0%.

- At 58.7% of total capital raised, debt remains the highest in history for comparable periods.

- Public companies accounted for 73.9% of total financing YTD, down from 80.2% in 2021.

- The graph below shows that U.S. activity dominated capital raises for the first fifty-one weeks of 2022, with 74.7% of all capital raised.

- International capital raises of $319.8M represented 7.4% of total capital raises, exceeding the previous record of 6.5% in 2019.

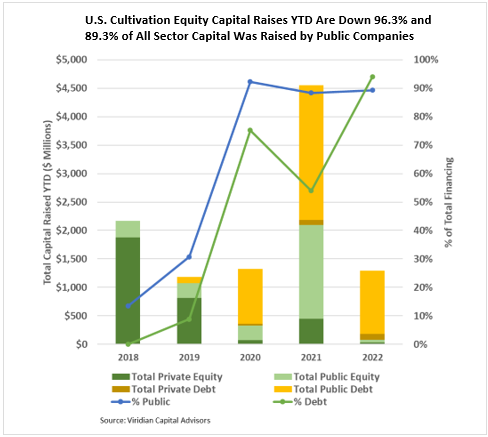

The U.S. Cultivation & Retail sector capital raises are down 71.6% YTD, but equity capital raised is down approximately 96.3%.

- Debt financing is down 50.1% YTD but accounts for about 94.0% of all capital raised; private companies raised 8.7% of it.

- 3% of total capital raises YTD were completed by public companies compared to 88.4% in 2021.

- In 2022, there have been no equity deals above $25M.

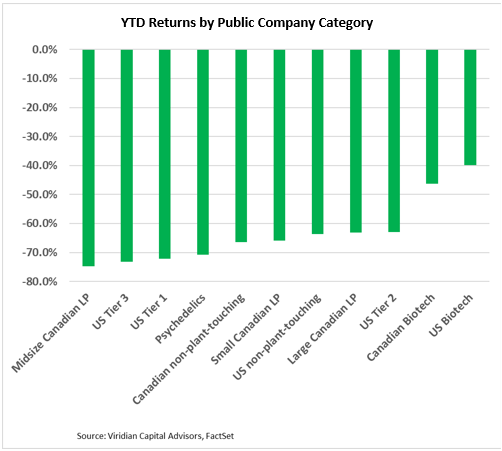

YTD Returns by Public Company Category

- Tier 3s, the category that stood most to gain from SAFE, lost another notch of ranking in terms of YTD returns. Investors are rightfully concerned about the liquidity of smaller companies in the No SAFE capital crunch environment. Tier 1s lost two notches demonstrating that liquidity is not always a benefit.

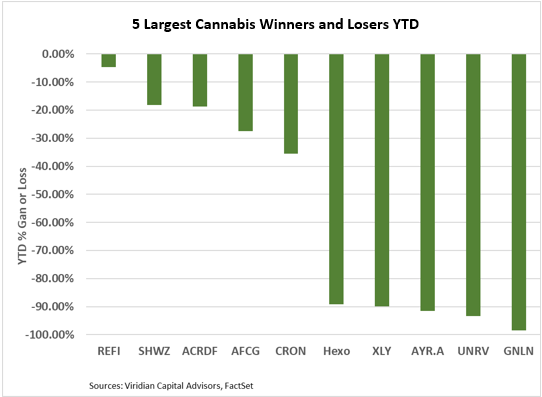

Best and Worst Performers of the last week and YTD

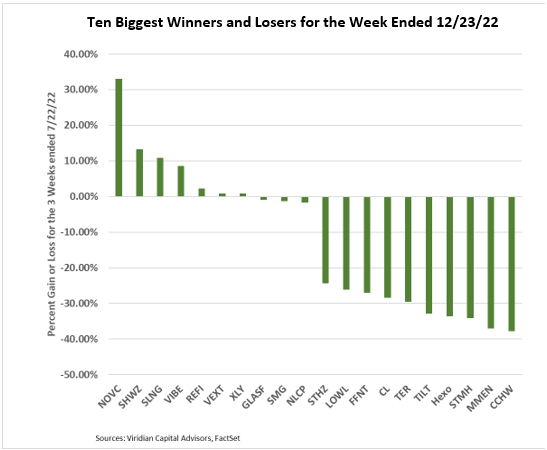

- Top gainers this week included capital providers Chicago Atlantic (REFI: Nasdaq) and New Lake Capital (NLCP: OTCQX), both of which gain from the continued capital squeeze; Nova Cannabis (NOVC: CSE), up on the news of its joint venture with Sundial, and a trio of well-performing smaller competitors, Schwazze (SHWZ: CSE), Vibe (VIBE: CSE), and Vext (VEXT: CSE) who might be up either on M&A speculation or on the realization that some of the smaller players will be sustainable even in the no SAFE environment.

- Top losers included California heavy operators: StateHouse (STHZ: CSE), Lowell Farms (LOWL: CSE), 4Front (FFNT: CSE), and MedMen (MMEN: CSE). HEXO was down 33% on the week after a 14 to 1 reverse split of its stock. A reverse split, in the absence of any other good news, often fails to halt the slide of a stock. How long will the company stay above Nasdaq listing requirements?