OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

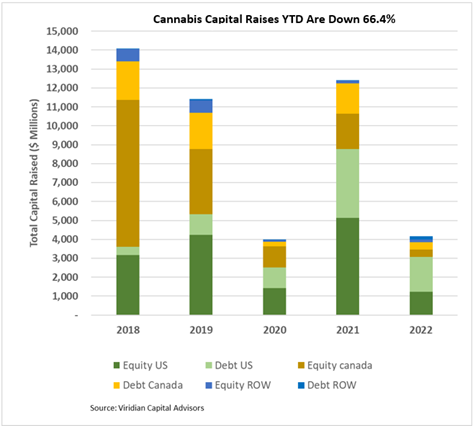

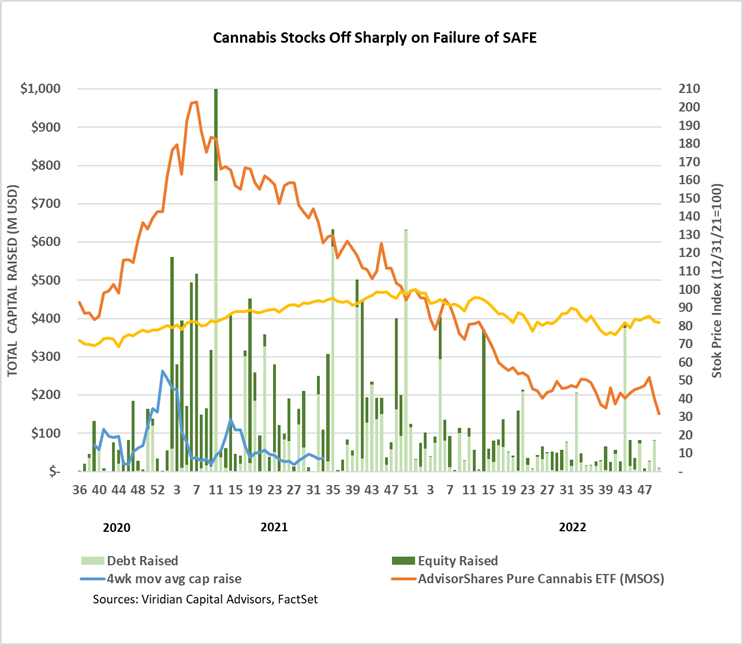

Cannabis capital raises are off 66.4% YTD:

- Total Equity issuance is off 75.6%, and total debt issuance is down 53.9%.

- U.S. debt is down only 48.9%, while Canadian debt is down a more significant 76.0%.

- At 58.3% of total capital raised, debt remains the highest in history for comparable periods.

- Public companies accounted for 74.5% of total financing YTD, down from 79.6% in 2021.

- The graph below shows that U.S. activity dominated capital raises for the first fifty weeks of 2022, with 73.9% of all capital raised.

- International capital raises of $319.8M represented 7.7% of total capital raises, exceeding the previous record of 6.3% in 2019.

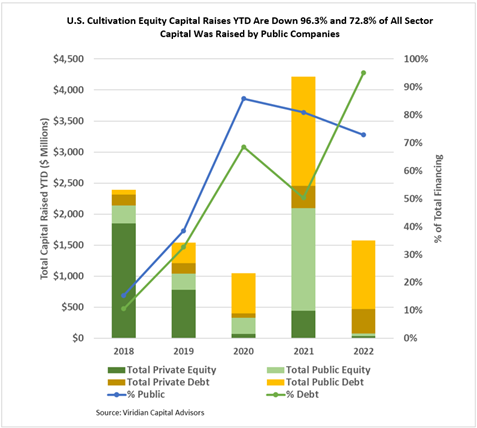

The U.S. Cultivation & Retail sector has experienced a similar change in capital raise activity, although the components have changed significantly.

- Total capital raised is down 67.1%, but equity capital raised is down approximately 96.3%.

- Debt financing is down 44.4% YTD but accounts for about 95.1% of all capital raised; private companies raised 25.1% of it.

- 72.8% of total capital raises YTD were completed by public companies compared to 83.2% in 2021.

- In 2022, there have been no equity deals above $25M.

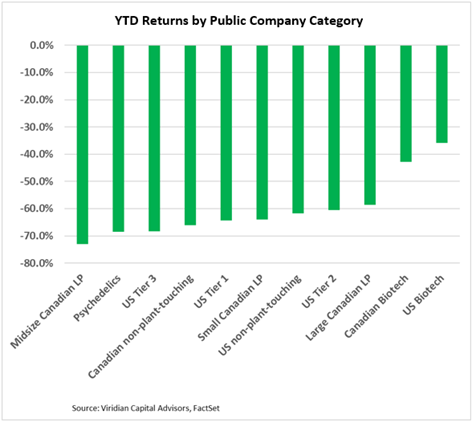

YTD Returns by Public Company Category

- Tier 3s, the category that stood most to gain from SAFE, lost two notches of ranking in terms of YTD returns. Investors are rightfully concerned about the liquidity of smaller companies in the No SAFE capital crunch environment.

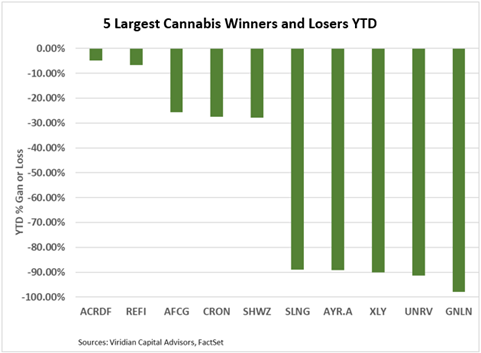

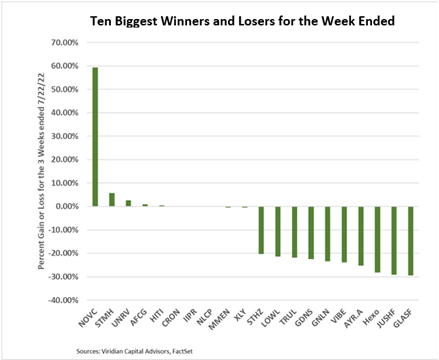

Best and Worst Performers of the last week and YTD

- Top gainers this week are from three categories: 1) out-of-the-money option equities trading on pure volatility, a category which includes Stem Holdings (STMF: OTC), Unrivaled Brands (UNRV: OTC), MedMen (MMEN: CSE), and Auxly (XLY: CSE); 2) Capital providers AFC Gamma (AFCG: Nasdaq), New Lake Capital (NLCP: OTCQX), and Innovative Industrial Properties (IIPR: NYSE), all of which stand to gain from the failure of SAFE; and Nova Cannabis (NOVC: CSE), which was up strongly on record volume. We saw no news to account for the gain.

- Top losers included AYR (AYR.A: CSE), Jushi (JUSHF: OTC), and Trulieve (TRUL: CSE).