OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

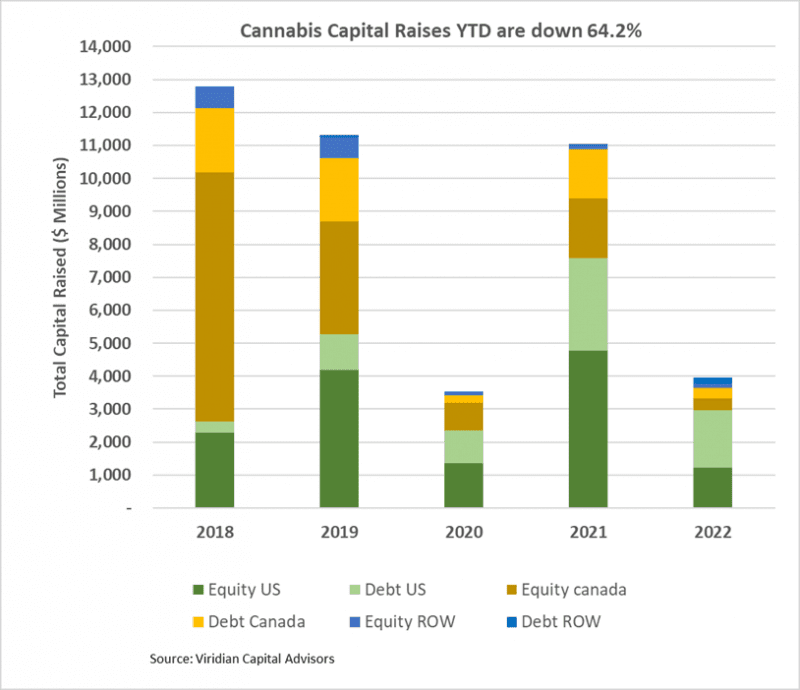

Cannabis capital raises are off 64.2% YTD:

- Total Equity issuance is off 74.4%, and total debt issuance is down 48.2%.

- U.S. debt is down only 37.8%, while Canadian debt is down a more significant 79.4%.

- At 56.5% of total capital raised, debt remains the highest in history for comparable periods.

- Public companies accounted for 74.5% of total financing YTD, down from 79.8% in 2021.

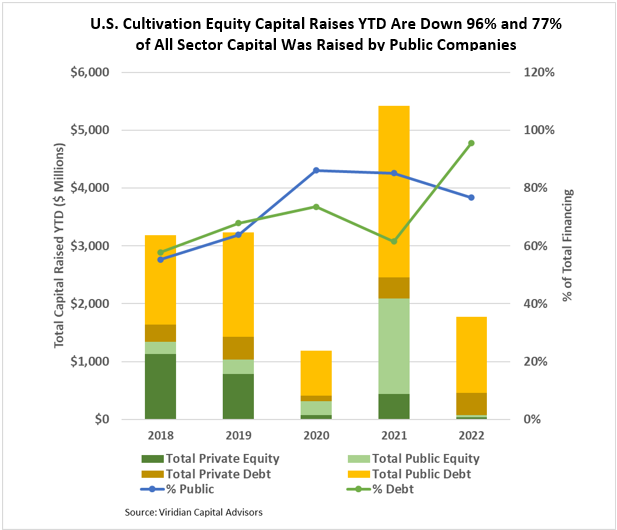

- The graph below shows that U.S. activity dominated capital raises for the first forty-five weeks of 2022, with 75.0% of all capital raised.

- International capital raises of $319M represented 8.1% of total capital raises, exceeding the previous record of 6.4% in 2019.

-

-

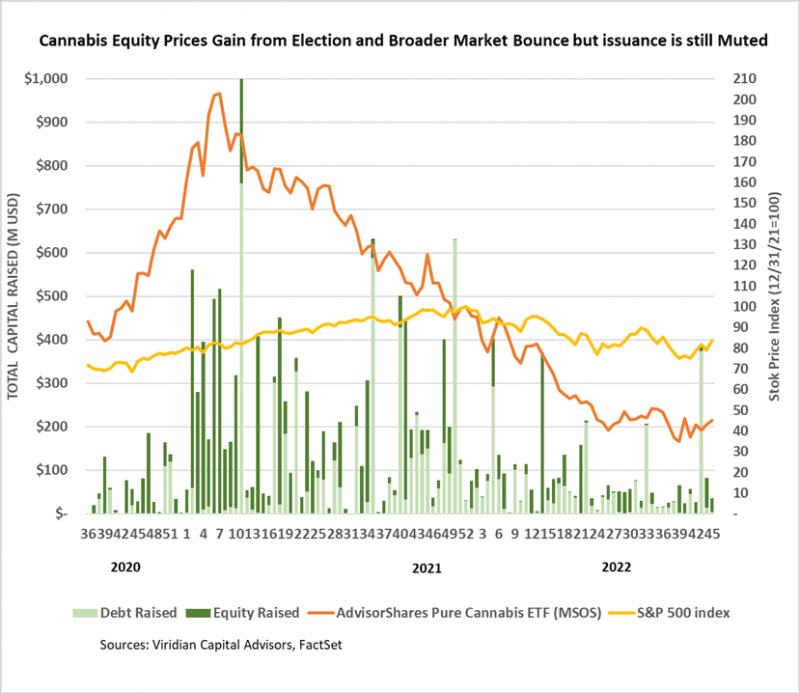

- Cannabis stock prices (measured by the MSOS ETF) were up 6.60% last week, buoyed by better-than-expected results from Green Thumb (GTII: CSE) and news of the $185M purchase of Cresco (CL: CSE) and Columbia Care (CCHW: CSE) assets by Sean “Diddy” Combs.

- We believe that the passage of SAFE+ in the lame-duck session is quite likely. SAFE+ will have potentially dramatic, though indirect, impacts on stock prices.

- Meanwhile, negative industry trends, including wholesale price compression and an inflation-pressured consumer, continue to pressure financial results. We will closely monitor changes to analysts’ 2023 outlooks over the next two weeks as third-quarter results continue to roll in. Investors should keep a close eye on cash levels as projected capital spending.

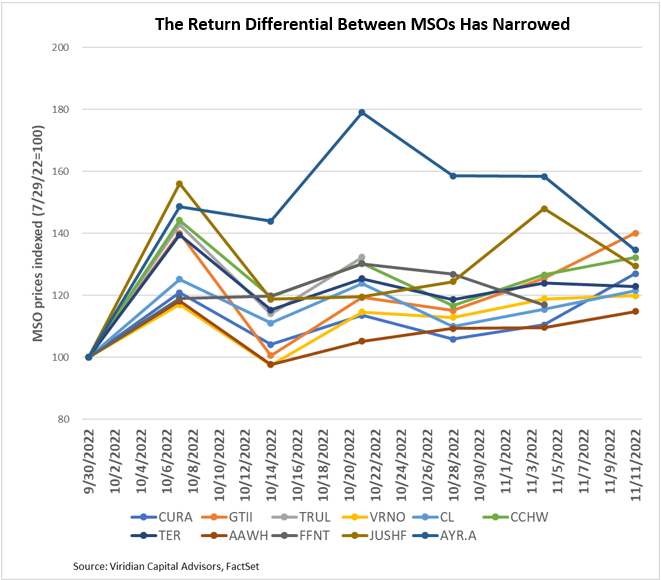

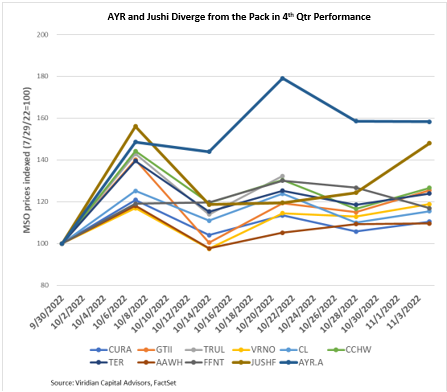

- Since the end of the third quarter, the major MSOs have traded in a relatively tight band. After initial outperformance by GTI and Curaleaf and recent catch-up spurts by AYR and Ascend, the spread has been narrowing over the last month, and less than 25 points of performance separates the best from the worst. The market is back to trading mainly as a block, reacting primarily to snippets regarding SAFE.

-

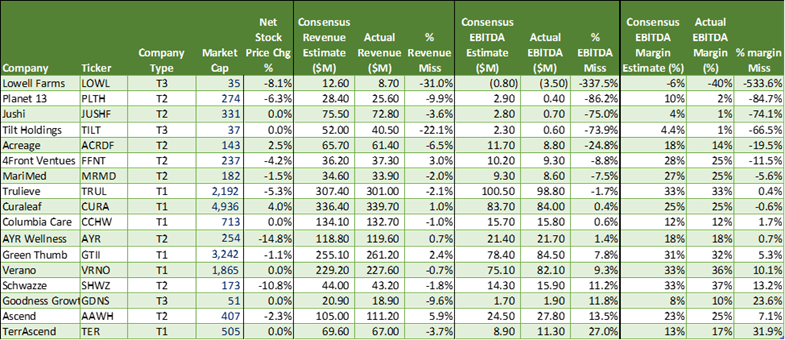

- Third-quarter earnings releases have been a mixed bag. Curaleaf (CURA: CSE), Green Thumb (GTII: CSE), Ascend (AAWH: OTC), and Schwazze (SHWZ: OTC) all had positive earnings surprises, while Trulieve (TRUL: CSE), Planet 13 (PLTH: CSE), MariMed (MRMD: CSE), Acreage (ACRDF: OTC), and Lowell Farms (LOWL: CSE) all disappointed. The chart below shows the revenue and EBITDA consensus estimates and actuals, ordered from the most significant EBITDA % misses to the most prominent EBITDA % beats.

The U.S. Cultivation & Retail sector has experienced a sharper change in capital raise activity:

- Total capital raised is down 67.3%, but equity capital raised is down approximately 96.3%.

- Debt financing is down 49.2% YTD but still accounts for about 95.6% of all capital raised; private companies raised 22.4% of it.

- 7% of total capital raises YTD were completed by public companies compared to 85.1% in 2021.

- In 2022, there have been no equity deals above $25M.

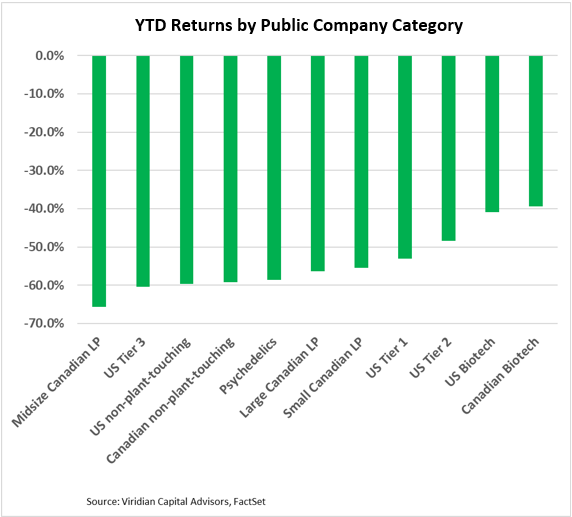

YTD Returns by Public Company Category

- Over the last month, U.S. Tier One companies have advanced four ranking positions due to solid performance from the largest names: Curaleaf (CURA: CSE). Green Thumb (GTII: CSE), and Trulieve (TRUL: CSE). The U.S Tier 3 category has underperformed as Parent Company (GRAMF: OTC). Tilt Holdings (TILT: CSE), Red White & Bloom (RWBYF: OTC), and StateHouse (STHZF: OTC) all suffered double-digit stock declines over the period.

- The market is still strongly differentiating between MSOs, and the gap in the last twelve-week stock performance between the best performer (GTI (GTII: CSE) up 26.9%) and the worst (4Front (FFNT: CSE) down 32.2%) has widened to 68 points. But since August, it’s been Green Thumb and everyone else. GTI has been the lone gainer over the last three months.

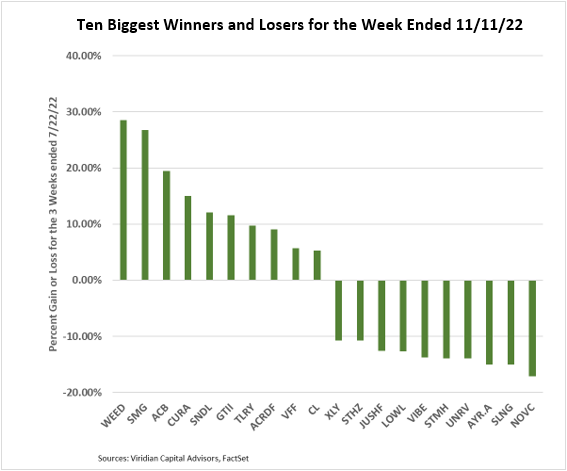

Best and Worst Performers of the last week and YTD

- Canopy Growth (WEED: TSX), Aurora (ACB: Nasdaq), and Sundial (SNDL: Nasdaq) were all among the top gainers this week on continued hope that the TSX gave Canopy’s innovative legal maneuver to consolidate earnings of its U.S. properties positive mention. Nasdaq has yet to issue a definitive ruling on the action.

- California companies Unrivaled Brands (UNRV: OTC), Stem Holdings (STMH: OTC), Vibe Growth (VIBE: CSE), and Lowell Farms (LOWL: CSE) repeated their last week’s positioning among the biggest losers, all down in the 12%-14% range.