OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

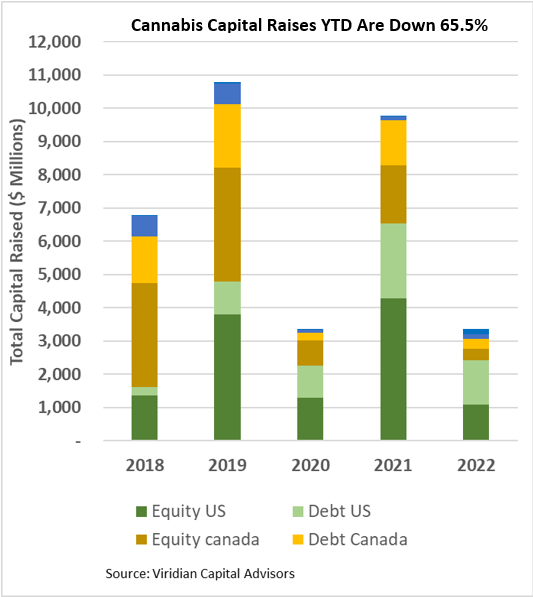

Cannabis capital raises are off 65.5% YTD

- Total Equity issuance is off 74.3%, and total debt issuance is down 50.5%.

- U.S. debt is down only 41.1%, while Canadian debt is down a more significant 78.4%.

- At 55.0% of total capital raised, debt remains the highest in history for comparable periods.

- Public companies accounted for 73.9% of total financing YTD, down from 83.2% in 2021.

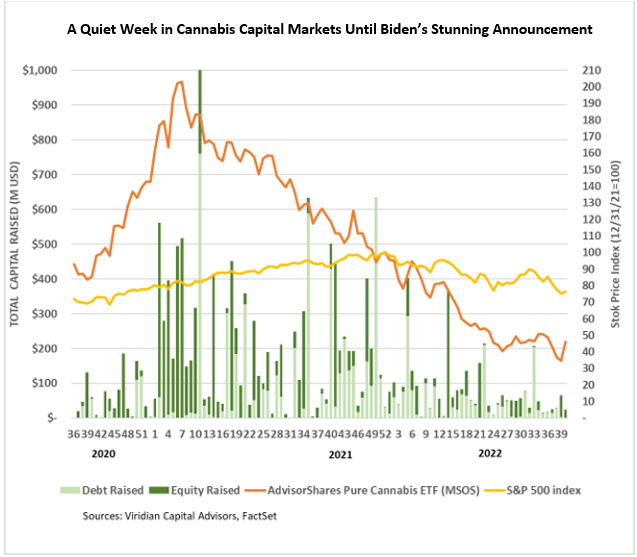

- The graph below shows that U.S. activity dominated capital raises for the first thirty-eight weeks of 2022, with 71.5% of all capital raised.

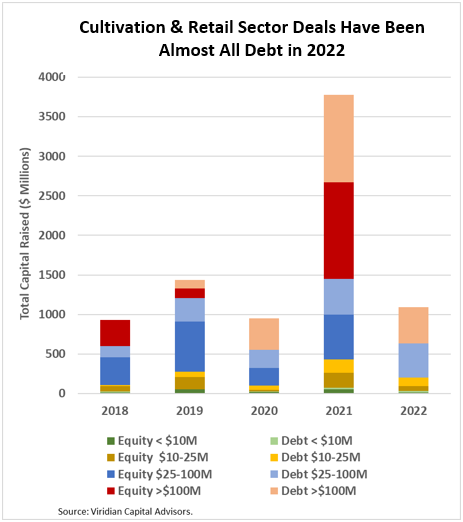

The U.S. Cultivation & Retail sector has experienced a sharper change in capital raise activity:

- Total capital raised is down 71.1%, but equity capital raised is down approximately 96%.

- Debt financing is down 41.7% YTD and accounts for about 93% of all capital raised; private companies raised a record 37% of it.

- 62.8% of total capital raises YTD were completed by public companies compared to 79.3% in 2021.

- In 2022, there have been no equity deals above $25M!

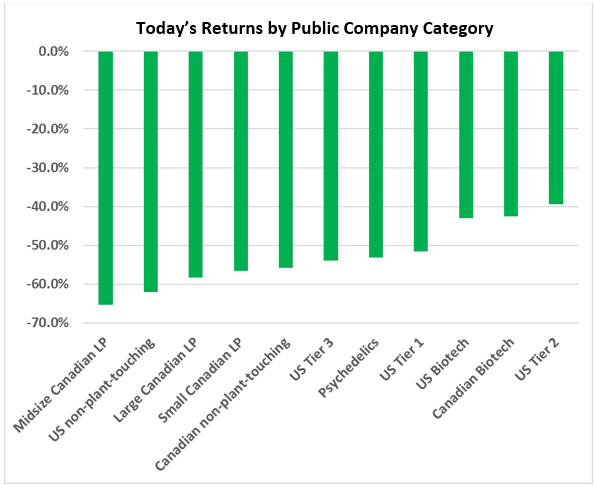

YTD Returns by Public Company Category

- U.S. Tier 1 companies improved several notches in response to the surprise Biden announcement. Canadian LPs have significantly underperformed the other categories.

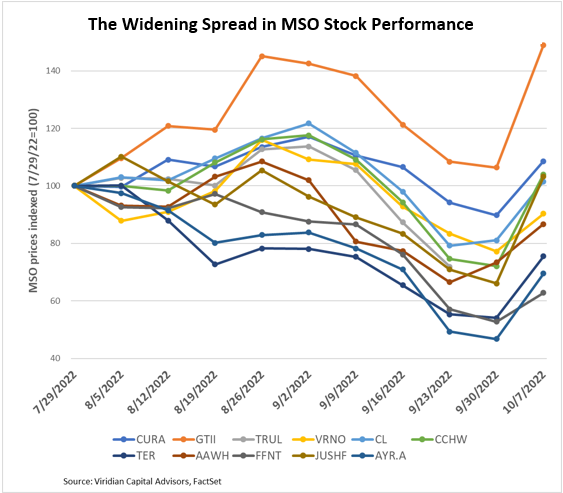

- The market is strongly differentiating between MSOs. In two months, there has been a 60-point difference between the percentage returns of the best-performing versus the worst-performing MSO. The chart below shows the divergence of stock prices since the end of July.

Best and Worst Performers of the last week and YTD

- Jushi Inc. (JUSHF: OTC) was the week’s best performer, up 56.1%. The market-beating performance was a bit puzzling since the company focuses on eastern limited license states, which are not the locations that would gain the most from rescheduling or de-scheduling.

- Glass House (GLASF: OTC), up 49.6% for the week, is more understandable. It is arguably the best-positioned company for an interstate commerce scenario.

- The worst performer was TPCO, down 18.9%. We saw no news to explain the move.