OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

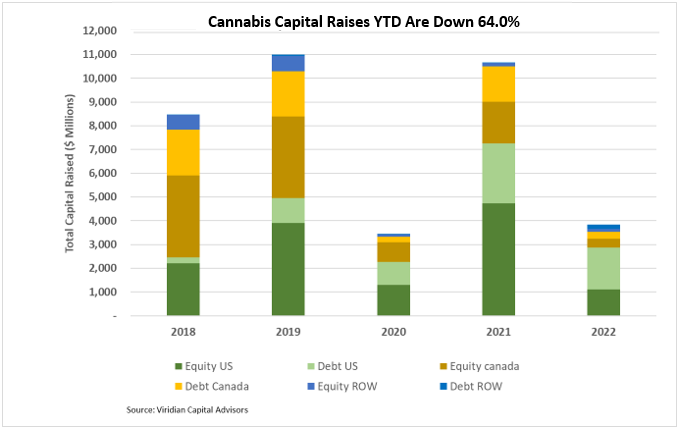

Cannabis capital raises are off 64.0% YTD:

- The U.S. Cultivation & Retail sector has experienced a sharper change in capital raise activity.

- Total capital raised is down 66.7%, but equity capital raised is down approximately 96.3%.

- Debt financing is down 47.3% YTD and accounts for about 95.6% of all capital raised; private companies raised 23.0% of it.

- 5% of total capital raises YTD were completed by public companies compared to 84.7% in 2021.

- In 2022, there have been no equity deals above $25M.

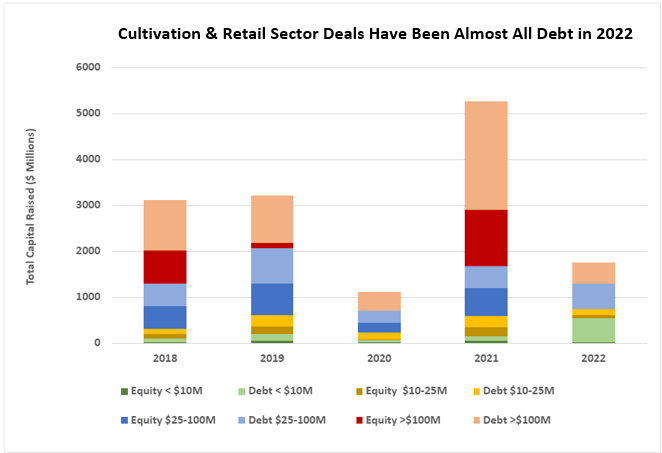

The U.S. Cultivation & Retail sector has experienced a sharper change in capital raise activity:

- The U.S. Cultivation & Retail sector has experienced a sharper change in capital raise activity.

- Total capital raised is down 66.7%, but equity capital raised is down approximately 96.3%.

- Debt financing is down 47.3% YTD and accounts for about 95.6% of all capital raised; private companies raised 23.0% of it.

- 76.5% of total capital raises YTD were completed by public companies compared to 84.7% in 2021.

- In 2022, there have been no equity deals above $25M.

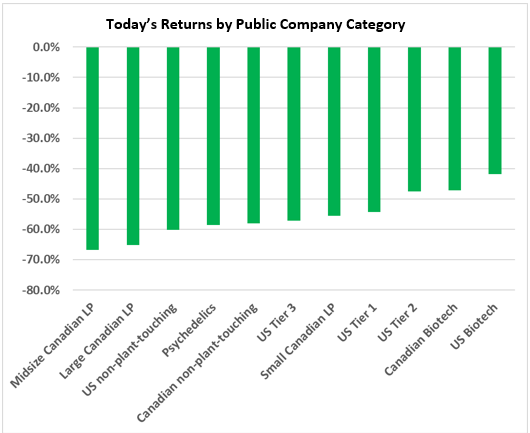

YTD Returns by Public Company Category

- What a difference a week can make! U.S. tier-one MSOs lost four places in our ranking of YTD stock performance in a dramatic demonstration that liquidity can cut both ways. U.S. Biotech and Psychedelics were two of the gainers.

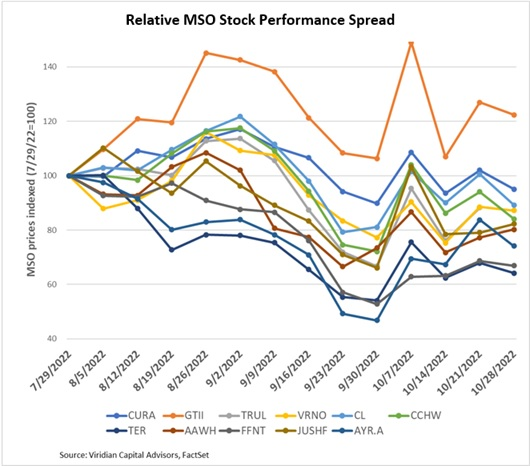

- The market is still strongly differentiating between MSOs, and the gap in the last twelve-week stock performance between the best performer (GTI (GTII: CSE) up 26.9%) and the worst (4Front (FFNT: CSE) down 32.2%) has widened to 68 points. But since August, it’s been Green Thumb and everyone else. GTI has been the lone gainer over the last three months.

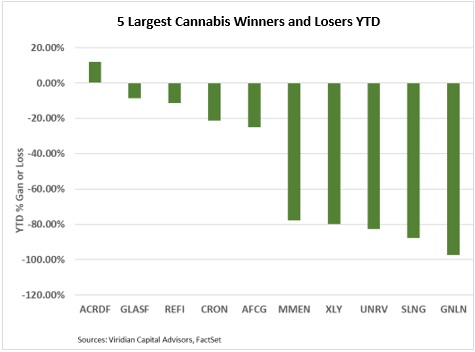

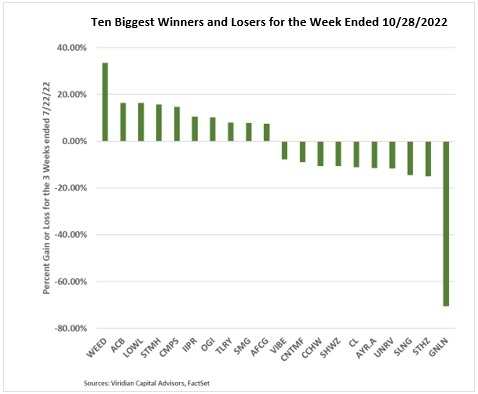

Best and Worst Performers of the last week and YTD

- Canopy Growth (CGC: Nasdaq) was the week’s biggest gainer, up 33% on the surprise announcement that it was completing its acquisition of Acreage and pooling its U.S. assets into a newly formed U.S. holding company. The news shocked the market because everyone believed such a move would jeopardize Canopy’s Nasdaq listing. Canopy has shown incredible legal creativity before, though. Hence, its announcement immediately set dozens of lawyers to work analyzing the potential for a U.S. MSO to use a similar workaround to gain a Nasdaq listing. By the end of this week, the enthusiasm for that possibility had died down, and Nasdaq’s announcement that it disagreed with consolidating the results of the U.S. operations into the Canadian entity erased some of the gains.

- Aurora Cannabis (ACB: Nasdaq) was the second largest gainer, up 16% on the Canopy news.

- Greenlane (GNLN: Nasdaq) was the worst performer of the week, down 70.6% on the news that it had priced a “best efforts” unit deal for gross proceeds of $7.5M. Each unit included two seven-year warrants struck with a 0% premium. Each of these terms is unusual. We are used to seeing ½ or one warrant per unit, usually priced at a premium of 20-30%, expiring in 2 -4 years. The Black Scholes value of the warrant package is $.735 reducing the net share price to about $.16 per share. Greenlane shares closed the week at $.49 per share, down from $1.68 the previous week. Greenlane leads the list of YTD decliners, down 97%.