OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

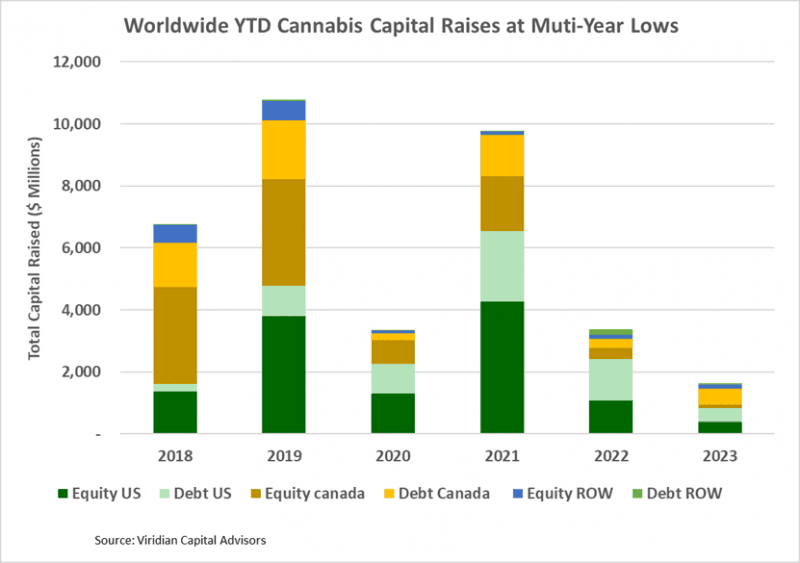

- Cannabis capital raises are off to a multi-year low. Only $1.65B closed through the first forty weeks of the year compared to $3.38B last year.

- Debt represents 60.4% of total capital raised, significantly higher than in any other comparable period since 2018.

- Public companies have raised 73.6% of total capital YTD, down from 73.9% last year and lower than any comparable period since 2019.

- International raises accounted for 11.8% of the total, the most significant percentage since before 2018.

VIRIDIAN INSIGHTS

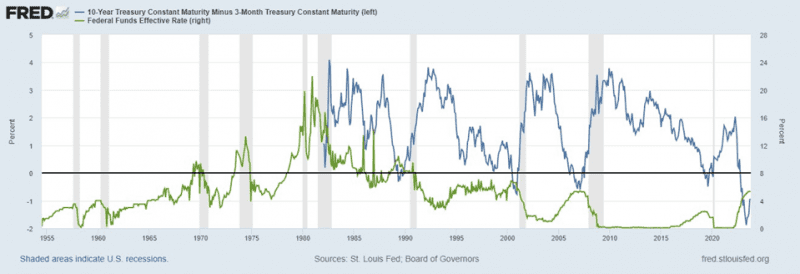

- Is Recession Talk Back in Fashion?

- The three-month-10-year spread has become less inverted, moving from a peak of 188 bp to around 95 bp. Sharp curve steepening, after a period of inversion, preceded each of the last four recessions. Add in increasing default rates on corporate debt, stubbornly high energy prices, a new Middle East war, and chaos in Washington, and one could easily conclude that a recession is imminent. Still, it matters how the curve steepening is happening. The current steepening is due to rising 10-year rates, which usually signals higher economic growth. We believe in the yield curve’s predictive power and think a recession is likely in 2024. What’s your view?

- Reschedule, Reschedule, Reschedule!

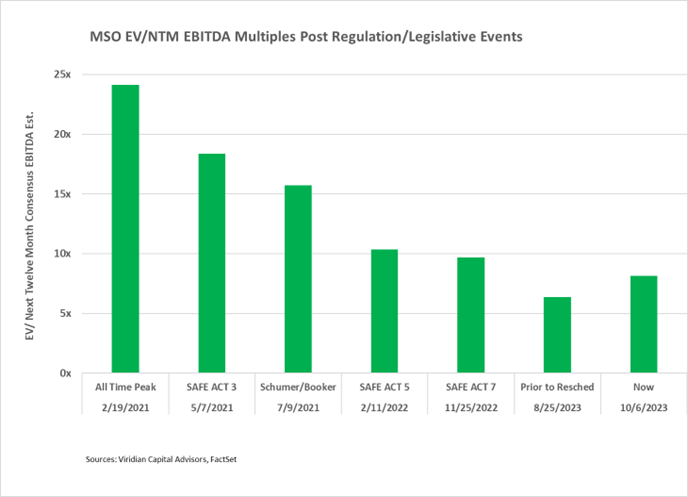

- The HHS recommendation to reschedule cannabis to Schedule 3 has dramatically impacted cannabis equity prices.

- As of 10/6/23, the MSOS ETF was up 44.5% from before the rescheduling news. The chart below shows enterprise to next-twelve-month valuation multiples now compared to previous times when positive regulatory/legislative news hit.

-

- Multiples are now approximately 21% below levels after the 5th SAFE Act passage in the House, but the rescheduling news is more significant as it dramatically impacts cash flows. We conclude that there is significantly more multiple expansion potential to come. If valuations multiples rose to where they were after the announcement of the Schumer-Booker bill, the incremental gains could exceed 93%.

- The potential additional gains also pose an increased risk. If the DEA does not follow the Schedule 3 recommendation, cannabis prices could drop to new lows. Although sheepish, we believe “things are different this time.” Simultaneous progress on 280e and the SAFE Act has never happened before, and we believe the benefits of these two acts together would exceed the benefits of the Schumer/Booker proposal from July 2021. On a down note, interest rates are significantly higher than they were in 2021, and industry economics is more challenging.

- There is still substantial uncertainty about the likelihood, timing, and potential impacts of rescheduling, and we will continue to update the summary below as we learn more:

- Likelihood:

- There is a high likelihood that the DEA agrees to reschedule cannabis to level III.

- The DEA has historically never overridden scheduling recommendations from the HHS.

- The most plausible reason for the DEA refusing the HHS recommendation is that cannabis is subject to control under the Single Convention on Narcotic Drugs of 1961, and rescheduling to lower than level two would not assure compliance with this treaty. Notably, the failure to prevent states from licensing adult-use cannabis put the U.S. in violation of the treaty. No matter the DEA’s position, it cannot bring the country back into compliance with the treaty. Still, this remains the most significant potential sticking point.

- Timing:

- Our best guess is rescheduling is unlikely to occur before Q2:2024.

- Once it has done its analysis, the DEA will post its recommendations and analysis to the Federal Register for public review. It will also open a 60-day public comment period. Interested parties may request a hearing before a federal administrative law judge to present other evidence or to object to the proposed rule.

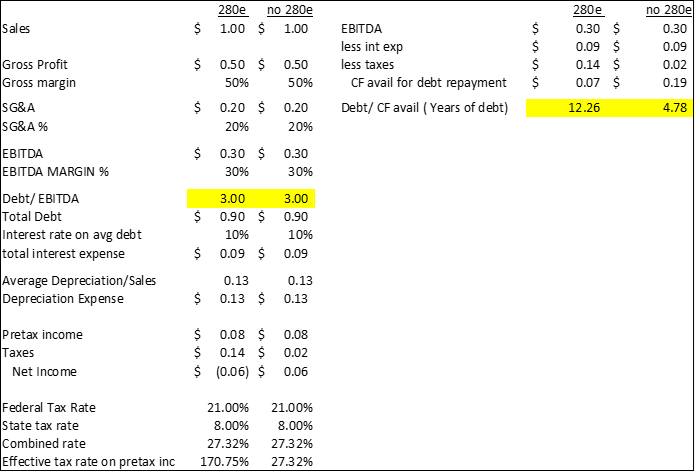

- Impacts– Two definite rescheduling results are the removal of 280e and the fostering of cannabis research.

- The removal of 280e would have a dramatic financial impact on plant-touching companies.

- The table below demonstrates that for a hypothetical cannabis company with 50% gross margins, 20% SG&A, and 3x Debt/ EBITDA, 280e can result in effective tax rates (on pretax income) of over 100%. The table demonstrates our previous claim that debt/EBITDA over three times is unsustainable in a 280e world, as the calculated payback period for the debt would be an unacceptable 12.26 years. Cannabis companies under 280e need less than 2x debt/EBITDA to have acceptable 5-year payback periods.

- The table shows that combined effective rates (depending on state tax rates) would be reduced to around 27% without 280e making a huge difference in debt capacity. Without 280e, companies could comfortably carry 3x leverage with acceptable payback periods. Importantly, by making interest expense tax deductible, the elimination of 280e also reduces the cannabis cost of capital and increases the intrinsic value of the firms.

- The removal of 280e would have a dramatic financial impact on plant-touching companies.

-

-

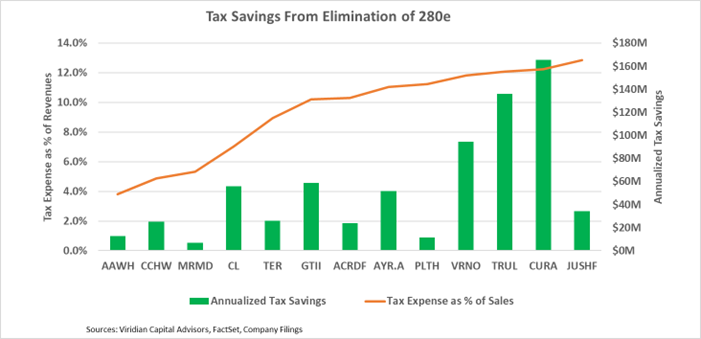

- We estimate annualized tax savings of the top 13 MSOs at $700M.

-

-

-

- Rescheduling will also spur cannabis research by reducing licensing requirements. Over time, this should accelerate medical product creation, providing significant patient benefits.

- What would NOT change:

- Rescheduling should not be confused with legalization. Cannabis as a Schedule 3 substance will continue to be federally illegal, which has several important implications:

- Uplisting to Nasdaq is not assured. Nasdaq is reportedly studying its policies concerning Schedule 3. It may require the SAFE Act to push them over the line.

- The SAFER Act would also probably be necessary to remove restrictions on credit card usage in dispensaries since state-legal adult-use dispensaries will still be violating federal law.

- Significant increases in institutional capital may occur with Schedule 3 status; however, institutions that are concerned with federal illegality may not gain sufficient comfort from Schedule 3.

- Rescheduling will not give cannabis companies access to Chapter 11 bankruptcy proceedings as the business will remain federally illegal.

- Potential pitfalls

- Increased role of FDA. While cannabis is Schedule 1, regulating the industry falls primarily to the DEA. Rescheduling to 3 will potentially increase the role of the FDA. While we have no reason to believe the FDA will feel empowered to begin more aggressively regulating the industry (especially since it will receive no new funding), it is a risk.

- The importance of a new “Cole memo” or Garland memo, which would explicitly draw limits on federal enforcement against state legal business, would be heightened. We expect such a memo will be forthcoming.

- Rescheduling should not be confused with legalization. Cannabis as a Schedule 3 substance will continue to be federally illegal, which has several important implications:

-

- How much SAFER will it be?

- On Wednesday, September 27, The Senate Banking Committee passed the SAFER Act with a 14-9 vote, marking the first time members of the Senate have voted on the bill despite its passage in the House 7 times! We can quibble about the margin of victory and the timing, but it must be counted as a significant achievement to get this far.

- This year, there appear to be sufficient votes in the Senate from both sides of the aisle to pass the bill. One bit of drama stems from the intent of Senator Schumer to roll the HOPE and GRAM bills into SAFER before the Senate vote. HOPE provides the states with funding for expunging cannabis offenses while GRAM ends the prohibition on firearm sales to medical cannabis patients. Will he get greedy and try for even more? We would count it implausible, except that we have seen this movie before.

- The good news of a temporary postponement of a government was overshadowed by the chaos of the removal of the House Speaker, threatening weeks of disarray during which essentially nothing will get done in Washington.

- The remaining drama is still on the House side. It will be instructive to see whether a stand-alone bill will be voted on. We believe any attempt at a “shell game” of trying to insert the bill inside other legislation will be treated harshly by the market. Too much déjà vu!

- Opinion is mixed as to how much the SAFER Act will accomplish. Seven tries ago, it would have been more critical, but since then, most cannabis companies, even relatively small ones, have obtained bank accounts, albeit expensive ones. We also do not see banks rushing to lend money to cannabis companies. The creditworthiness of most cannabis companies is below bank standards, and the industry still requires considerable specialized knowledge that the banks do not yet have. Moreover, for the Tier One banks like Chase, the sector is too small to move the needle. We have no doubt that Chase may want to participate in a junk bond offering for GTI, but lending to a medium-sized cannabis company? Probably not, at least not immediately.

- SAFER would be a huge deal if it directly allowed for dispensary credit card usage. However, after hearing the thoughts of more sophisticated legal minds like Marc Hauser and Shane Pennington, our read is that while it will give the payment processors cover, it is questionable if the card companies will play ball. We think SAFER and rescheduling will eventually tip the balance and produce both up-listing and credit cards, but neither directly achieve those goals.

- Still, the passage of the SAFER Act after all these years would be a significant psychological boost that cannot be underestimated.

- Re-equitization is in the air.

- Three new companies have jumped on the equity bandwagon alongside Cannabist and Canopy Growth:

- Curaleaf (CURA: CSE) completed a marketed offering of 2.7M shares at approximately US$4.39 for total gross proceeds of US$11.85M. TSX listing requirements primarily drove the transaction, but the proceeds will support international operations and general working capital purposes. We viewed the Company as a likely issuer even without the TSX requirements because of its high EV/2024 multiple.

- Vext Science (VEXT: CSE) announced a non-brokered private placement of up to $10M. The Company believes an existing investor and the management group will purchase most of the issue. Frankly, Vext doesn’t fit our model of who would be next. It neither trades at an exceptionally high multiple nor has excessive market leverage. VEXT has solid uses for the capital in its Ohio expansion. Proforma for all announced acquisitions, Vext will have an operating Tier I cultivation facility, an operating manufacturing facility, and four retail dispensaries in Ohio.

- Aurora Cannabis (ACB: TSX) sold 53.2M common shares at approximately US$0.534 for gross proceeds of about US$27.9M. Aurora intends to use most of the proceeds to retire its outstanding US$25M in convertible notes. Aurora doesn’t fit the model espoused below, either. Its liabilities to market cap is only 1.02x, and it trades at a modest multiple of 2024 EBITDA of 7.25x.

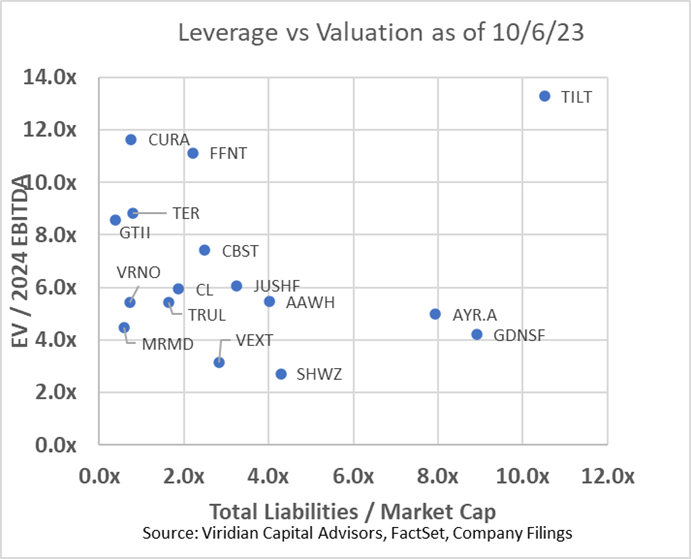

- The table and chart below help frame the likely candidates for additional issuance. Companies with high leverage but reasonable valuation parameters will likely follow with moderate-sized equity issuance. We expect companies will look to “average up” with the expectation of further price gains if rescheduling and SAFER stay on course. We could see Cannabist and Curaleaf hit the market again on this basis.

- Based on this reasoning, likely candidates include AYR (AYR.A: CSE), more from Cannabist (CBST: NEO), Cresco (CL: CSE), more from Curaleaf (CURA: CSE), Jushi (JUSH: NEO), and Trulieve (TRUL: CSE).

- Some companies that could benefit from re-equitization, like Goodness Growth (GDNS: CSE) and Tilt (TILT: CSE), may struggle to get an equity issuance done, given their extreme leverage. This could change rapidly with the further evolution of stock prices or improvements in operations at the companies.

- Three new companies have jumped on the equity bandwagon alongside Cannabist and Canopy Growth:

-

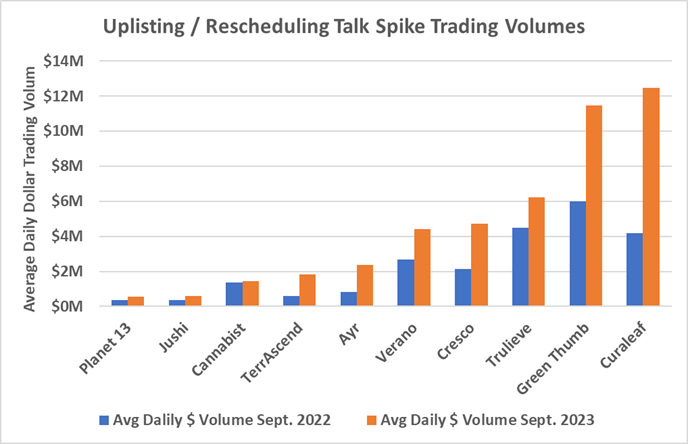

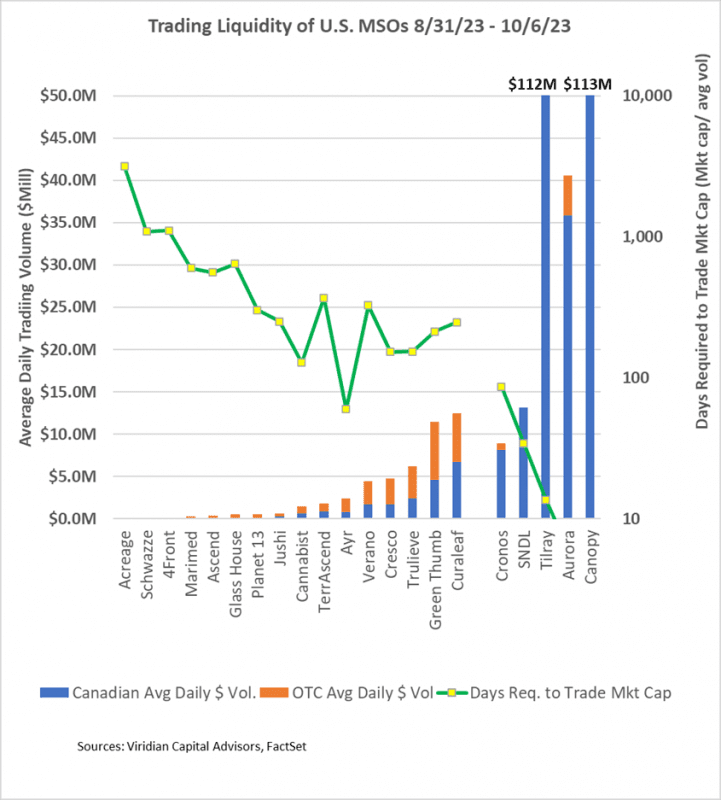

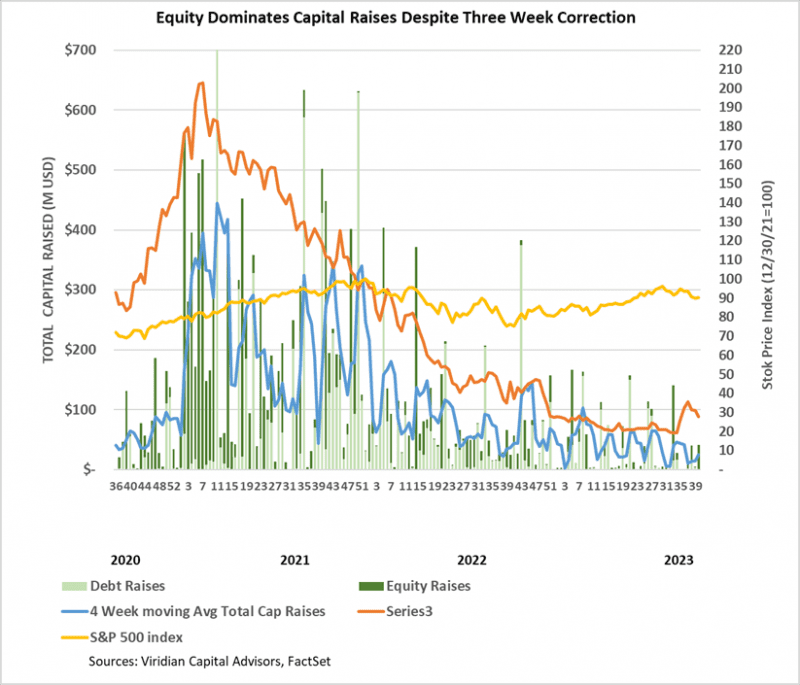

- Trading Volumes are Increasing

- The graph below compares the average daily dollar trading volume for the ten highest volume MSOs between 8/31/23 and 10/6/23 and the equivalent period in 2022. The aggregate average daily dollar volume for the group is up 156%. Gains range from 5% for Cannabist (CBST: NEO) to 209% for TerrAscend (TSND: TSX).

- But the days required to trade the market cap indicator, shown by the green line below (measured on the right axis), continues to show tremendous illiquidity compared to the Canadian LPs, many of which trade on Nasdaq. For example, Verano’s 326 days would mean that if an investor had a 5% position in Verano and wanted to trade out of their position, assuming that they wish to represent less than 25% of average daily volume, it would take them 65 days to sell out of the position. The same percentage position in SNDL could be traded in under seven days.

- Analysts have not revised their slow growth estimates for the remainder of 2023 and 2024, waiting for more clarity about the fate of SAFE and rescheduling.

-

- The impact of the combination would be considerable, potentially enabling higher revenues through credit card purchases, promoting higher internally financed growth rates, and fostering the revitalization of the cannabis capital markets.

- The graph below shows consensus revenue and EBITDA estimates for the 10 top MSOs for 2023 and 2024. The light blue line at the bottom shows that 2023 consensus EBITDA margins are now 24.0%, down from the beginning of the year expectations of 27.2% and 2022 actual margins of 25.0%. 2023 consensus EBITDA estimates are now 3.3% lower than actual 2022 EBITDA for the group. 2024 margins, shown in the dark blue line, are now expected to be 26.1%.

- The green lines at the top show that 2023 revenues are expected to be 1% higher than 2022, while 2024 revenues are expected to be 8% higher than 2023. The two-year 3.9% CAGR is decidedly anemic and reflects ongoing wholesale price compression, somewhat offset by positive impacts of new adult rec states. This is not the kind of growth rate cannabis investors signed up for.

- Lower revenue and margin expectations are among the reasons we do not believe cannabis multiples are likely to fully retrace the path back to peaks of over 20x EV/EBITDA.

- Amend and Extend

- Our Chart of the Week showed that most of the top ten MSOs have manageable cash flow shortfalls after interest expense, taxes, capex, and debt maturities. Even the three with significant gaps relative to their market caps will likely achieve a favorable resolution. Our primary reasoning is that lenders will bend over backward to avoid repossessing their collateral, particularly given that cash flows service all other liabilities and contribute towards reducing debt. This situation will be improved significantly by the likely elimination of 280e.

- Two companies with very different credit profiles took steps to fix their debt maturity problems this week:

- Lowell Farms (LOWL: CSE) repurchased all $22.2M of its Senior Secured Convertible Debentures due October 2023. The debt holders received membership interests in LF Brandco LLC, an entity formed to hold the IP relating to “Lowell Smokes” and “Lowell Herb Co.” and approximately 36% of the Company’s consolidated common stock. (about 6.85M shares). The stock component of the deal is only worth about $2.0M at current prices, and we do not have enough information to value the potential royalty streams from the IP interests. Can any of our readers fill in the missing blanks? What value do the bondholders believe they are getting from this deal?

- In a surprising turnaround, Cannabist (CBST: CBOE) announced that it was redeeming $25M of the outstanding $33.8M of its 13% SR secured notes at 101%. The notes had been offered at around 97% recently, and the Company had been in discussions with holders to exchange on a one-for-one basis with the Company’s 9.5% senior secured notes due February 2026. The exchange idea never entirely made sense to us. (we tried!). We didn’t get the logic of exchanging a higher coupon shorter maturity bond for a lower coupon longer maturity pari-pasu issue. Even up. Evidently, the Company ran into the same argument and pivoted towards a partial redemption.

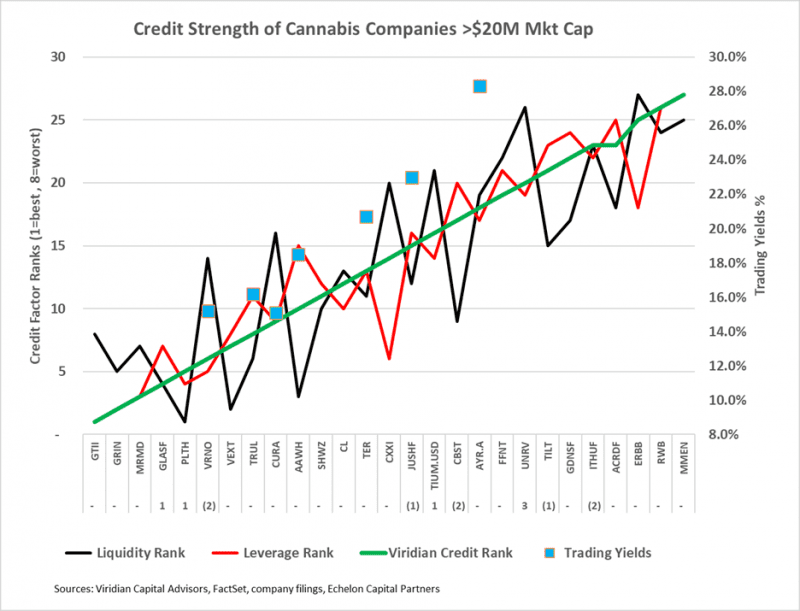

- The chart below shows our updated 10/6/23 credit rankings for the 27 U.S. cannabis companies with over $20M market cap. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement. The blue squares show the offered-side trading yields for each Company. Where two or more traded obligations are quoted, we have chosen the closest to a 2026 maturity. Note we have priced AYR to a 2026 maturity because we believe investors are pricing the bond by weighting probabilities of default vs maturity extensions. We have suspended the publication of Cannabist’s yields, awaiting post-tender markets to settle.

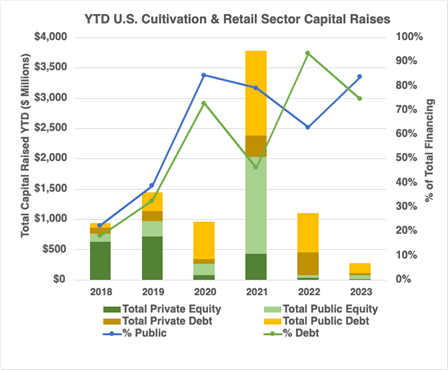

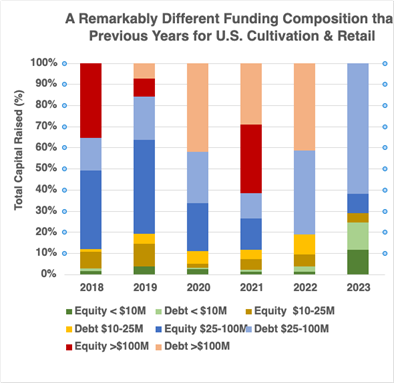

- YTD, U.S. Cultivation & Retail sector capital raises are down 75.2% from 2022 and are lower than any previous comparable period since before 2018.

- Debt is still the dominant form of funding, accounting for 74.7% of all cultivation sector capital raised. 17.2% of the debt raised YTD has been for private companies.

- Large transactions are still absent from the market. There have been no debt or equity deals over $100M YTD. The graph below shows the strikingly different composition of U.S. Cultivation & Retail capital raises in 2023 compared to previous years, with small equity and midsized debt dominating raises.

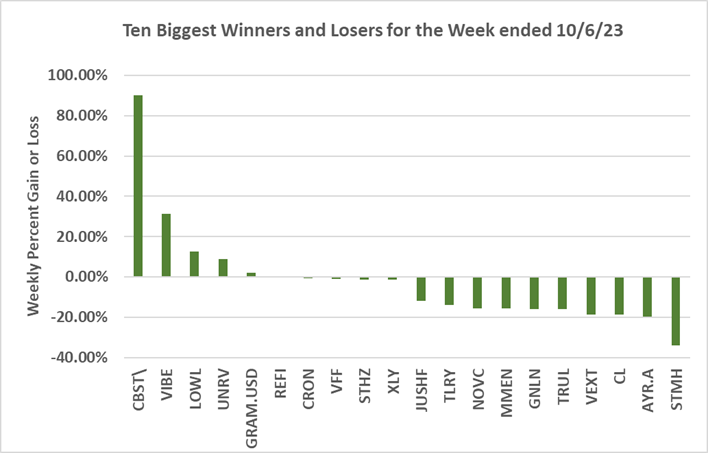

- Cannabis equities (as measured by the MSOS ETF) were down 10.83% for the week.

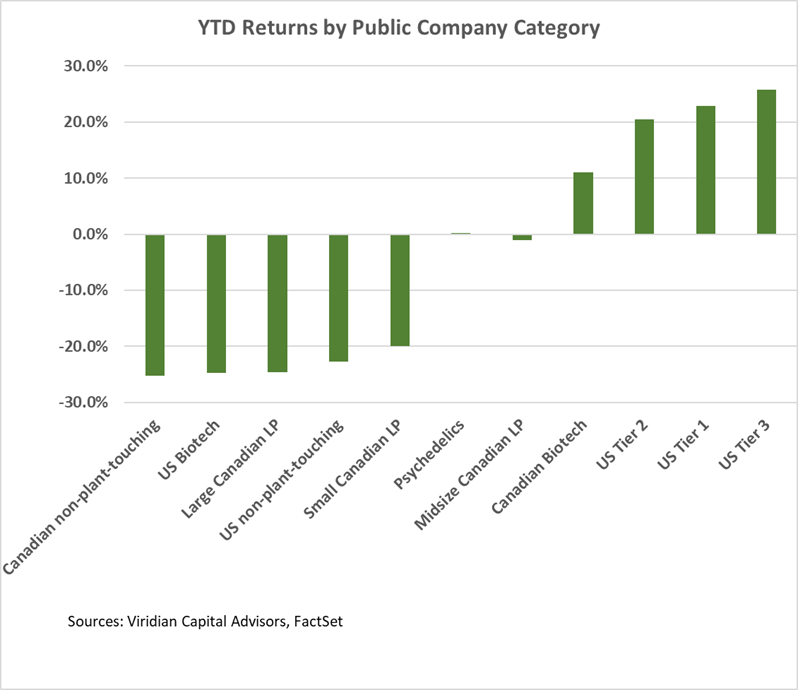

YTD Returns by Public Company Category:

- There were no significant ranking changes this week.

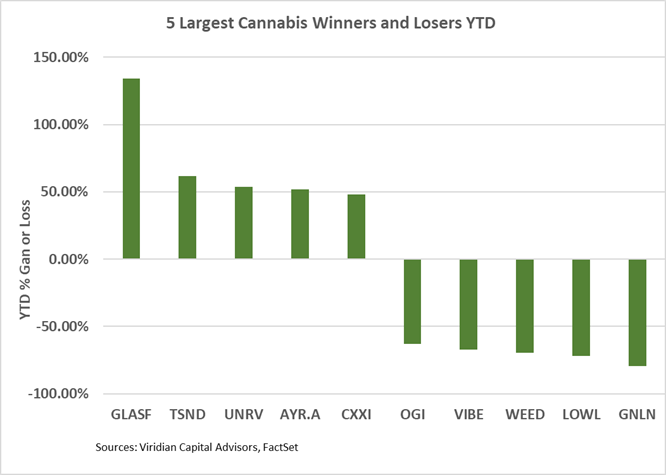

Best and Worst Performers of the last week and YTD:

- Cannabist (CBST: CBOE) and Lowell Farms (LOWL: CSE) were both on the leaders list after taking action to eliminate potential upcoming crises at maturity. AYR (AYR.A: CSE) was on the loser list for the second consecutive week, based on the House chaos potentially slowing down the SAFER Act and the lack of new company announcements regarding debt maturity extensions.