OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

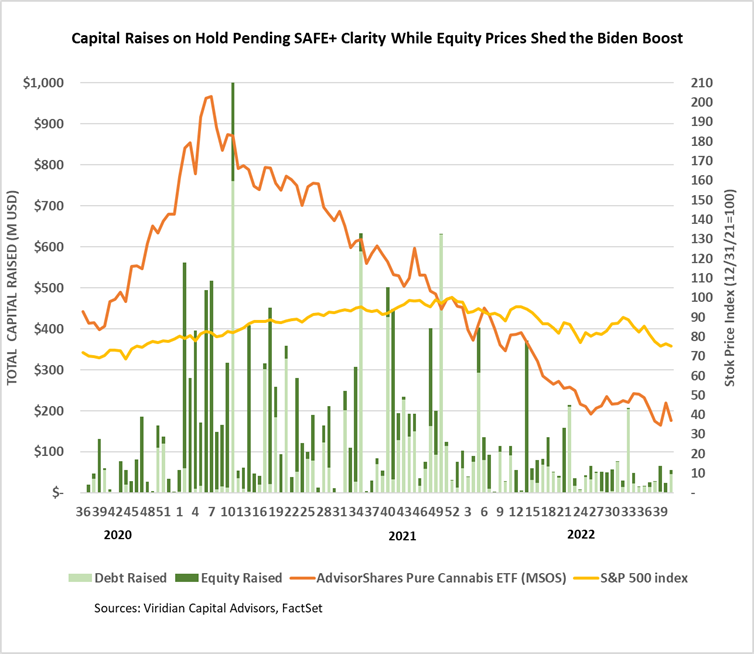

Cannabis capital raises are off 66.4% YTD:

- Total Equity issuance is off 75.8%, and total debt issuance is down 49.7%.

- U.S. debt is down only 39.9%, while Canadian debt is down a more significant 78.5%.

- At 53.7% of total capital raised, debt remains the highest in history for comparable periods.

- Public companies accounted for 73.9% of total financing YTD, down from 83.2% in 2021.

- The graph below shows that U.S. activity dominated capital raises for the first forty-one weeks of 2022, with 71.8% of all capital raised.

The U.S. Cultivation & Retail sector has experienced a sharper change in capital raise activity:

- Total capital raised is down 69.9%, but equity capital raised is down approximately 96%.

- Debt financing is down 39.5% YTD and accounts for about 93% of all capital raised; private companies raised a record 36% of it.

- 64.0% of total capital raises YTD were completed by public companies compared to 78.9% in 2021.

- In 2022, there have been no equity deals above $25M, which has never happened in a comparable period.

YTD Returns by Public Company Category

- What a difference a week can make! U.S. tier-one MSOs lost four places in our ranking of YTD stock performance in a dramatic demonstration that liquidity can cut both ways. U.S. Biotech and Psychedelics were two of the gainers.

- The market is still strongly differentiating between MSOs, but the record-high gap of 86 points last week has narrowed to only 45 points. The chart below shows the divergence of stock prices since the end of July.

Best and Worst Performers of the last week and YTD

- Three of the top ten performers this week are California based: StateHouse (STHZ: OTC), Unrivaled (UNRV: OTC), and Glass House (GLASF: OTC), possibly on news that California is becoming more aggressive in fighting the illicit market.

- AYR Wellness (AYR.A: CSE) has now been one of the top ten performers for two weeks. The company had become too cheap for investors to ignore and is also a potential take out candidate.

- Aside from Goodness Growth (GDNS: CSE), down 58.9% after being jilted by Verano (VRNO: CSE), Canadian companies, including Canopy (WEED: TSX), Aurora (ACB: TSX) and Sundial (SNDL: Nasdaq) were prominently featured in the loser list.