OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

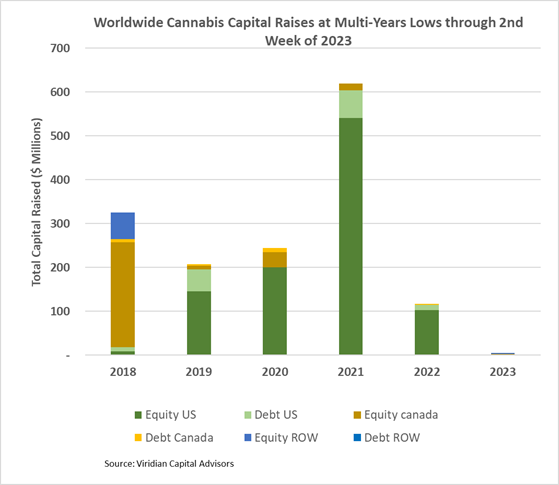

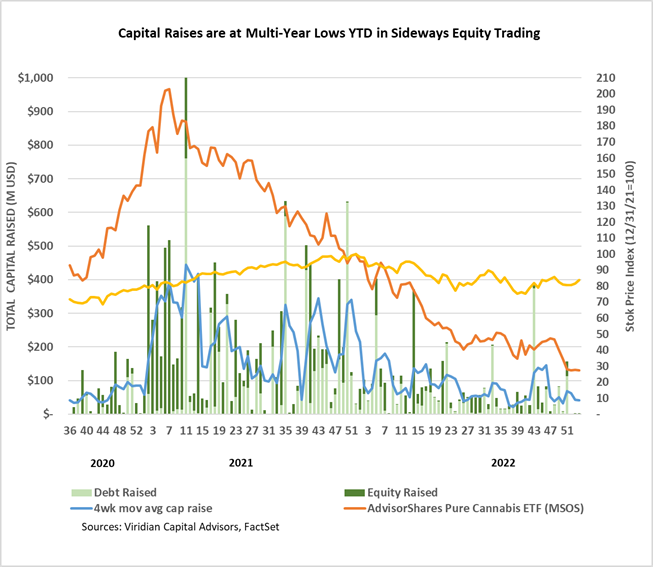

Cannabis capital raises are off to a multi-year low. Only $5.9M has closed through the first two weeks of the year compared to $117.6M last year:

- No U.S. issues have closed YTD.

- No debt issues were closed this week.

- Public companies have raised 56.7% of total capital YTD.

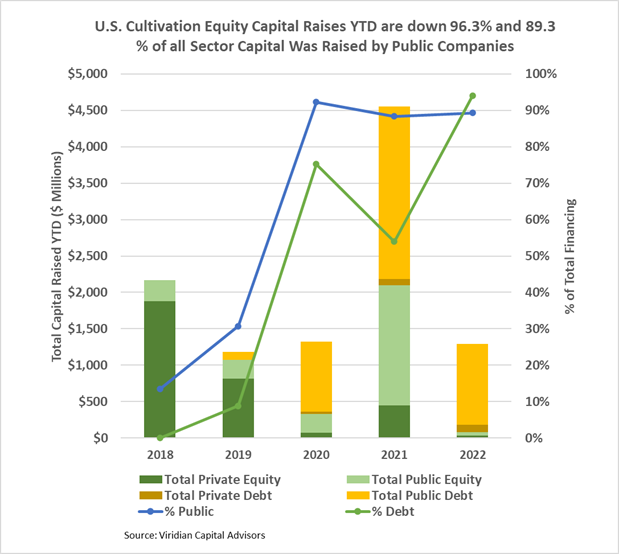

The U.S. Cultivation & Retail sector capital raises are down 71.6% YTD, but equity capital raised is down approximately 96.3%:

- Debt financing is down 50.6% YTD but accounts for about 94.0% of all capital raised; private companies raised 8.7% of it.

- 89.3% of total capital raises YTD were completed by public companies compared to 88.4% in 2021.

- In 2022, there have been no equity deals above $25M.

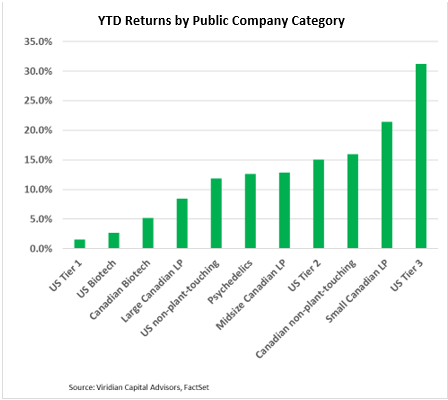

YTD Returns by Public Company Category

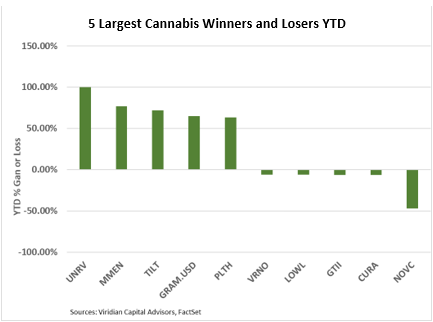

- Returns continue to be positive across all public company categories YTD. Tier one U.S. MSOS underperformed this week and slid five places into the worst performer category. Ironically given the macroeconomic factors, Tier three U.S. companies have been the best performers. Some of the last year’s most beaten-up stocks, including MedMen (MMNFF: OTC), TPCO (GRAMF: OTC), Red White & Bloom (RWBYF: OTC), and Unrivaled Brands (UNRV: OTC), are all up over 65% YTD.

Best and Worst Performers of the last week and YTD

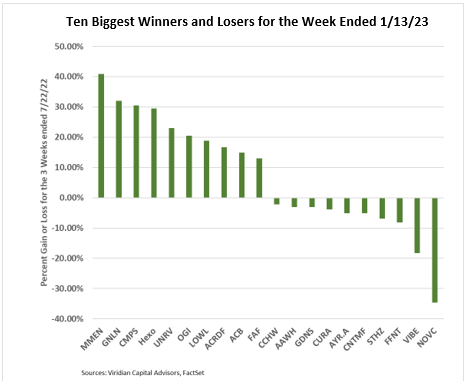

- A curious grouping of companies appeared on top of the leader list this week: MedMen ( MMEN: CSE), Greenlane (GNLN: Nasdaq), HEXO (HEXO: Nasdaq), and Lowell Farms (LOWL: CSE) were all up between 19% (LOWL) and 41% (MMEN). All four have one thing in common; their debt is more than three times their market cap, a level we generally associate with stress/distress.

- The largest losers included Nova Cannabis (NOVC: CSE), Vibe Growth (VIVE: CSE), and 4Front (FFNT: CSE), down 35%, 18%, and 8%, respectively. We saw no news to account for the declines.