OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

VIRIDIAN INSIGHTS

- SEVEN CANNABIS PREDICTIONS FOR 2024

- THE DEA WILL GO ALONG WITH RESCHEDULING TO LEVEL 3. However, the process may take longer than widely expected with public hearings and likely court appeals. Timing remains uncertain, but we think it could take longer than the market believes. Will it be in place by election day? We doubt it will be fully enacted, but we believe it will be announced in time to campaign on.

- The SAFER ACT, HOWEVER, WILL CONTINUE TO STRUGGLE. WE HAVE DOUBTS THAT IT WILL BE ENACTED IN 2024. Internecine warfare in an election year will prevent any meaningful compromises from being reached. Senator Schumer will likely declare, “We are very close” for the umpteenth time only to fail to push it through. Frankly, the industry seems to have switched its focus to rescheduling, and the push for SAFER seems diluted.

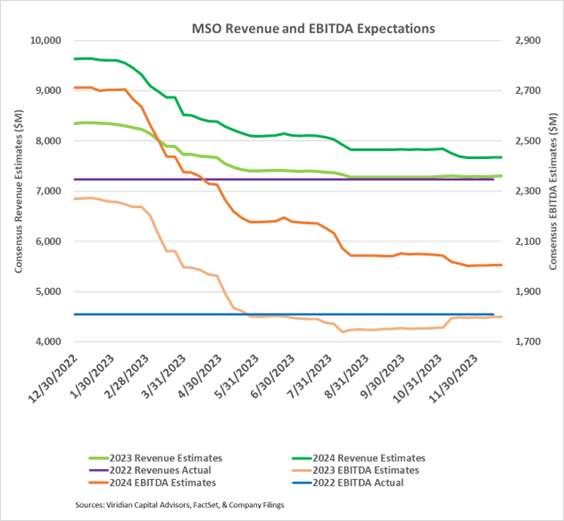

- NEW STATES DRIVE A RESURGENCE IN GROWTH AND INCREASED EBITDA. The graph below shows the progression of analysts’ expectations of 2023 and 2024 revenues and EBITDA through 2023. Note: at the beginning of 2023, consensus estimates for the top ten MSOs called for Revenue of $8.34B (up 15.4% from 2022) and EBITDA of $2.27B (up 25.4% from 2022). Estimates were cut continuously throughout the year, as we predicted in the first quarter.

- Analysts estimates finally hit bottom around the end of October. Revenues and EBITDA for 2024 are projected to be 5.05% and 11.5% higher than 2022, respectively.

- Although we do not believe we have seen the last of commoditization-based wholesale price compression, we think the analysts may be a bit cautious in their 6.2% aggregate consensus 2024 revenue growth. A year of Maryland and Ohio and near-term price stability in several key markets suggests a higher growth expectation may be in order.

- Similarly, we believe the 25.7% 2024 consensus EBITDA margins may be too low as they are only 1.0% higher than the 2022 figures. The industry found religion in 2022 and 2023, stringently managing costs and tightening working capital controls. The industry is poised to be more efficient and profitable as growth returns.

-

-

-

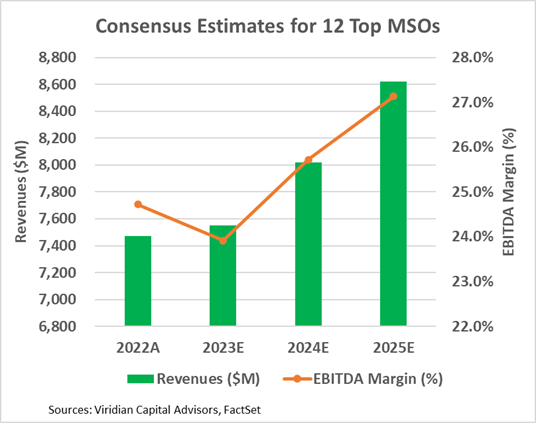

- The graph below shows actual and projected revenues and EBITDA for 12 top MSOs through 2025.

-

-

-

-

-

- THE CANNABIS CAPITAL MARKETS WILL SEE A MODEST RESURGENCE BASED ON RENEWED REVENUE AND EBITDA GROWTH AND A GROWING LIKELIHOOD OF RESCHEDULING. We all thought 2022 was a lousy year until we saw 2023! Worldwide cannabis capital raises dropped 57.3% from 2022, nearly 56% lower than the last capital freeze year in 2020. The cultivation and retail sector, which generally accounts for over half of all capital raises, was particularly hard hit: total capital raises of around $400M were off 75% from an already horrible year in 2022.

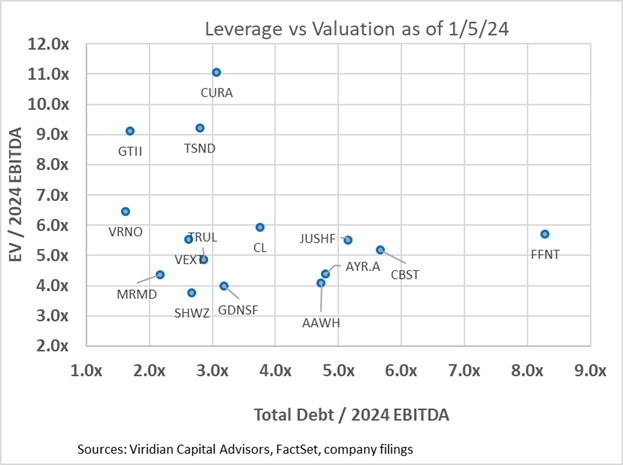

- The graph below shows the Enterprise value to 2024 EBITDA multiples against the Debt/ 2024 EBITDA ratios. We believe that companies with debt/2024 over 3x and reasonable valuations will seize on likely catalyst-driven upswings in equity prices to sell meaningful amounts of equity and reduce debt. 4Front Ventures, an outlier on the chart below, is shown proforma for the conversion of $23M of debt to equity announced last week.

- The graph below shows the Enterprise value to 2024 EBITDA multiples against the Debt/ 2024 EBITDA ratios. We believe that companies with debt/2024 over 3x and reasonable valuations will seize on likely catalyst-driven upswings in equity prices to sell meaningful amounts of equity and reduce debt. 4Front Ventures, an outlier on the chart below, is shown proforma for the conversion of $23M of debt to equity announced last week.

- CANNABIS DEBT SECURITIZATION WILL TAKE OFF IN 2024. We believe the Pelorus securitization transaction completed in July was one of the most critical developments in cannabis debt of the past five years. Securitization is a logical extension of the cannabis debt markets, and the creation of over-secured tranches of debt based on diversified pools of loans will bring major institutional investors who have, to date, avoided the cannabis space into the market. Subsequent developments of credit default swaps will eventually aid in reducing cannabis credit spreads to levels approaching high-yield debt. This will not happen overnight, but the process has begun.

- 2024 WILL BE THE YEAR INVESTORS DISCOVER CANNABIS DEBT. We were talking with investors at a recent conference, and one told us that he viewed GTI stock as a cash equivalent. We beg to differ. On the other hand, senior secured debt of companies like Ascend Wellness, at yields approaching 16%, D.O. seem attractive places to park cash while waiting for greater clarity on rescheduling and SAFER. After seeing two-year losses of around 90% on their equity investments, we think investors should look hard at the underlying debts of these same companies. Viridian publishes credit rankings of these companies every week with indicative debt pricing. Will investors brave a new market for exceptional yield, or are investors still convinced they can time the upswing in cannabis stocks despite years of evidence to the contrary?

- CANNABIS M&A WILL BOUNCE BACK FROM ITS LOWEST YEAR EVER IN 2023. Despite its promising potential for rescheduling and legislative reform, 2024 will not immediately differ from 2023: capital markets remain challenging, profitability is squeezed, and many private operators are tired of fighting the uphill cannabis battle. Moreover, they see the advantages of being part of a larger organization. This is just an aspect of a more significant trend toward consolidation. One of our Charts of the Week showed how fragmented cannabis is relative to other industries, and the long-term trend is that the big will get bigger. No other significant U.S. consumer-facing industry has leaders as small as the largest MSOs.

- THE CANNABIS CAPITAL MARKETS WILL SEE A MODEST RESURGENCE BASED ON RENEWED REVENUE AND EBITDA GROWTH AND A GROWING LIKELIHOOD OF RESCHEDULING. We all thought 2022 was a lousy year until we saw 2023! Worldwide cannabis capital raises dropped 57.3% from 2022, nearly 56% lower than the last capital freeze year in 2020. The cultivation and retail sector, which generally accounts for over half of all capital raises, was particularly hard hit: total capital raises of around $400M were off 75% from an already horrible year in 2022.

-

-

- THE CAPITAL MARKETS ARE FROZEN, AWAITING GREATER CLARITY ON RESCHEDULING.

- This week, the non-redacted text of the HHS recommendation was released, confirming that after much study, the HHS believes cannabis should be rescheduled to Schedule III from Schedule I. We saw no major unexpected revelations in the documents. As expected, the HHS emphasized that:

- Cannabis has a potential for abuse that is lower than other substances in Schedules I and II;

- that there are currently accepted medical uses for cannabis,

- while cannabis can lead to low physical dependence, ‘the likelihood of serious outcomes is low.”

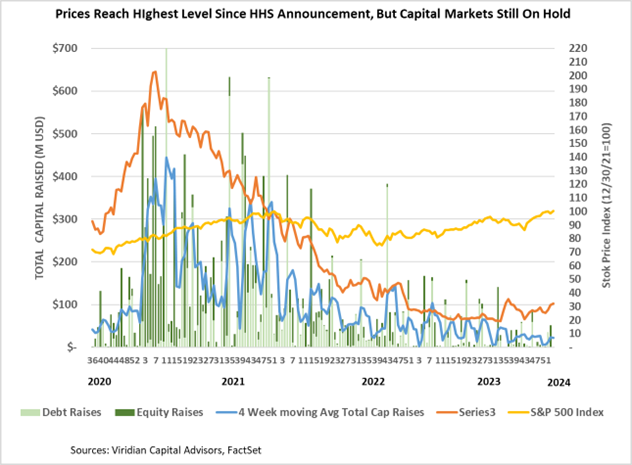

- Ironically, the strength in equity prices and the widespread belief in an imminent DEA announcement have produced an even deeper chill in capital raises. No financial officer of a plant-touching company wants to raise equity now only to see his stock price double when rescheduling is announced. The rational decision is to wait. The same reasoning applies to debt raises since removing 280e will add significantly to cash flows, increasing credit quality and, presumably, reducing debt spreads.

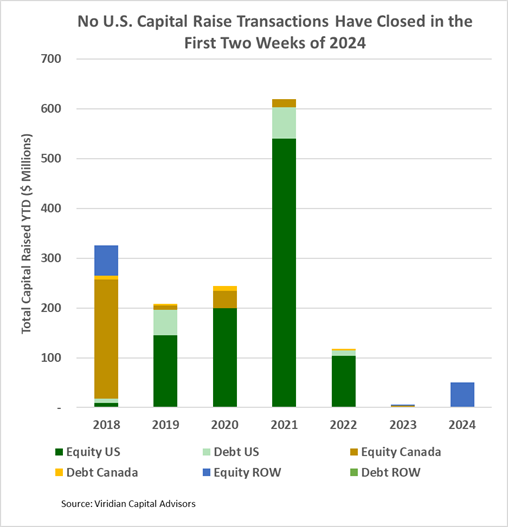

- The week ending 1/12/24 was the first week since the third quarter of 2019 when no equity or debt transactions closed!

- This week, the non-redacted text of the HHS recommendation was released, confirming that after much study, the HHS believes cannabis should be rescheduled to Schedule III from Schedule I. We saw no major unexpected revelations in the documents. As expected, the HHS emphasized that:

- GIVING CREDIT WHERE CREDIT IS DUE

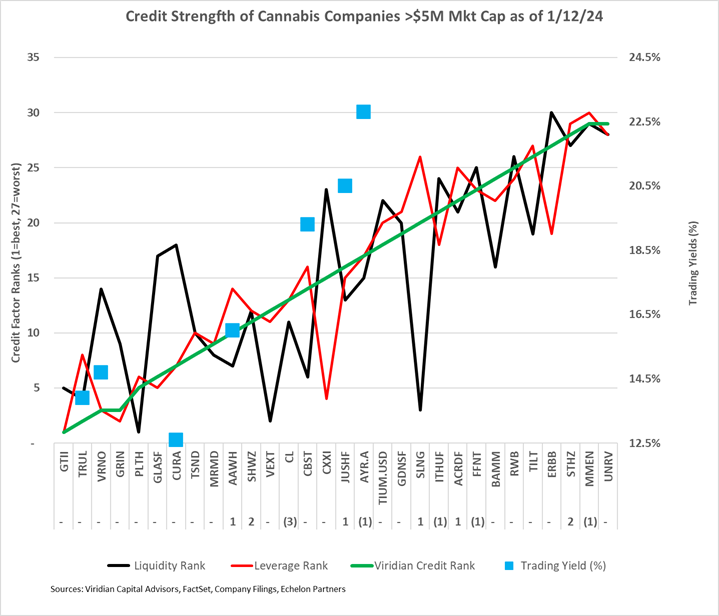

- The chart below shows our updated 1/12/24 credit rankings for the 30 U.S. cannabis companies with over $5M market cap. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement.

- The blue squares show the offered-side trading yields for each company. Trading yields have declined significantly since the HHS rescheduling announcement.

- Verano and Trulieve appear to be more rationally priced than Curaleaf, offering higher yields at what we believe to be lower risk. At the riskier end of the spectrum, AYR’s new 13% Sr. Secured Debt due 2026, trading at around 22%, looks attractive. We think the company is still overleveraged, but we believe that upside catalysts in 2024 will likely allow the company to right the ship.

- The most significant credit move of the week was the Cresco Lab (CL: CSE) three-notch deterioration to #13 from #10 last week, primarily due to worsened leverage and profitability rank scores.

- NOTHING MATTERS BUT RESCHEDULING

- The HHS recommendation to reschedule cannabis to Schedule 3 dramatically impacted cannabis equity prices, propelling the MSOS ETF upwards by nearly 85%. As of 1/12/24, the ETF was up 67.35% from before the rescheduling news.

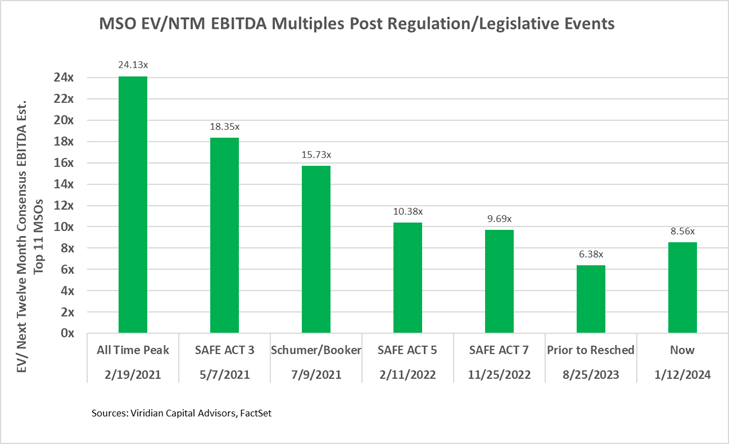

- The chart below shows enterprise to next-twelve-month valuation multiples now compared to previous times when positive regulatory/legislative news hit.

- EV/NTM EBITDA Multiples are now 17.53% below levels after the 5th SAFE Act passage in the House in February 2022. Still, the rescheduling news is more significant as it dramatically impacts cash flows. We conclude that there is significantly more potential for multiple expansions. If valuations multiples rose to where they were after the announcement of the Schumer-Booker bill, the incremental gains would equal 83.8%.

FINANCIAL IMPACTS OF REMOVING 280e

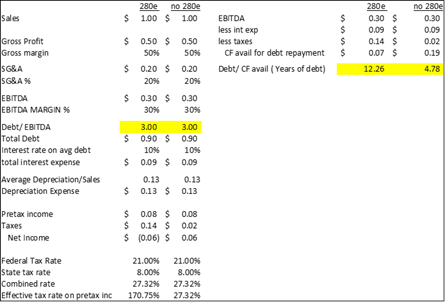

- The table below demonstrates that for a hypothetical cannabis company with 50% gross margins, 20% SG&A, and 3x Debt/ EBITDA, 280e can result in effective tax rates (on pretax income) of over 100%.

- The table demonstrates our previous claim that debt/EBITDA over three times is unsustainable in a 280e world, as the calculated payback period for the debt would be an unacceptable 12.26 years. Cannabis companies under 280e need less than 2x debt/EBITDA to have acceptable 5-year payback periods. The table shows that combined effective rates (depending on state tax rates) would be reduced to around 27% without 280e, making a considerable difference in debt capacity.

- Without 280e, companies could comfortably carry 3x leverage with acceptable payback periods. By making interest expense tax deductible, the elimination of 280e also reduces the cannabis cost of capital and increases the intrinsic value of the firms.

- Removing 280e would still not support the level of debt we now see in the industry. Six of the top sixteen companies now have debt/2024 EBITDA over 4x, which is unsafe even without 280e, especially given ongoing cost inflation and wholesale price compression.

-

-

- We estimate annualized tax savings of the top 13 MSOs at $700M.

-

- SOME CORPORATE MOVES TO REDUCE DEBT DON’T FLY

- Canopy Growth (WEED: TSX)((CGC: Nasdaq) canceled a planned $30M equity issue that was intended to augment liquidity and pay down debt.

- Canopy’s share price had taken a hit after announcing the placement on January 9, most likely because the transaction proposed to sell units at a significantly below-market $4.29 per share consisting of one share and one five-year warrant with an exercise price of $4.83. We calculate a net share price of only $3.03 for the transaction, a 40% discount on the pre-announcement price.

- Canopy is facing more significant problems, trying to dilute its way out of its growing net debt problem. Investors demanded a considerable discount to accept more shares, but in the end, Canopy may have to bite the bullet and take whatever terms it can get.

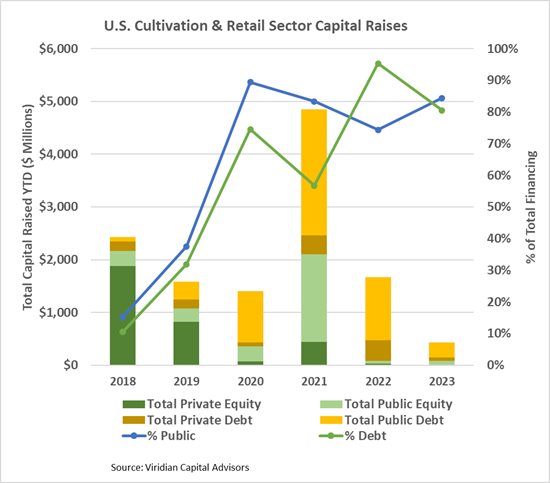

- No Cultivation and Retail sector capital raises closed in the first two weeks of 2024, and we expect capital markets to remain tight until more clarity arises regarding rescheduling. The graph below shows annual cultivation & retail trends over the last few years.

- Cannabis equities (as measured by the MSOS ETF) were up 3.67% for the week, gaining sharply on Friday on the publication of the unredacted HHS rescheduling recommendation. The market is convinced that a DEA announcement will be forthcoming soon, and prices are up sharply In early week trading.

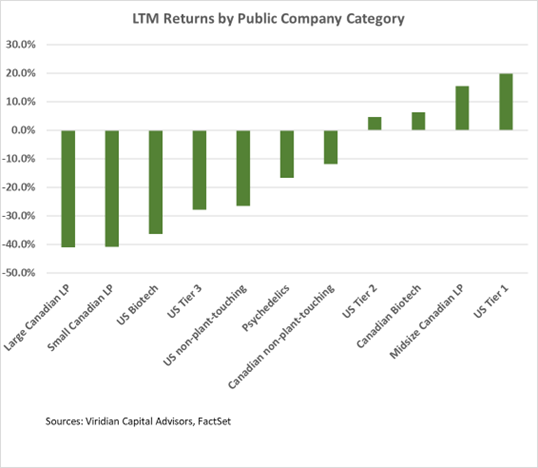

YTD Returns by Public Company Category:

- The strong rescheduling rally places five categories in positive 52-week returns. U.S. Tier one MSOs have risen to the top-gaining category.

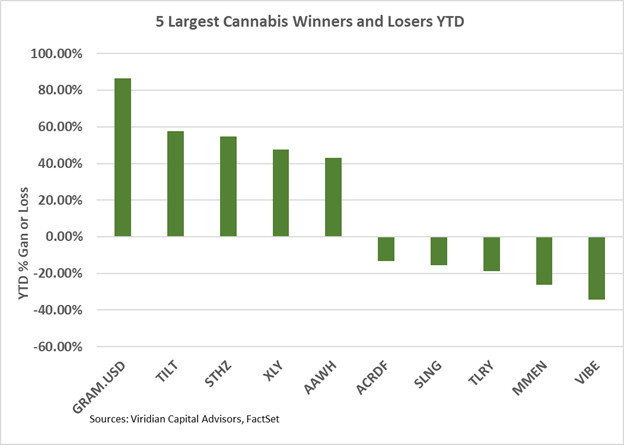

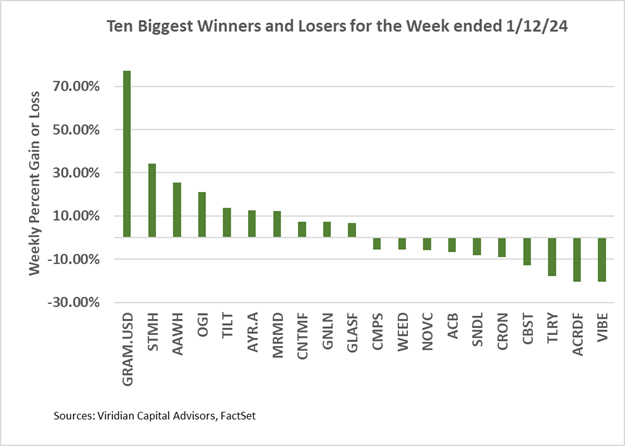

Best and Worst Performers of the last week and YTD:

- The top gainers were credit-challenged companies that stand to gain from both reopened capital markets and increased cash flows from eliminating 280e. The Viridian Chart of the Week pointed out five companies outperforming in up markets. Three of these companies, AYR (AYR.A: CSE), Ascend (AAWH: CSE), and MariMed (MRMD: CSE), were on the top gainers list this week.

- The losers list included read like a list of top Canadian LPs, including Aurora (ACB: Nasdaq), Canopy Growth (CGC: Nasdaq), SNDL (SNDL: Nasdaq), Cronos (CRON: Nasdaq), and Tilray (TLRY: Nasdaq).