OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

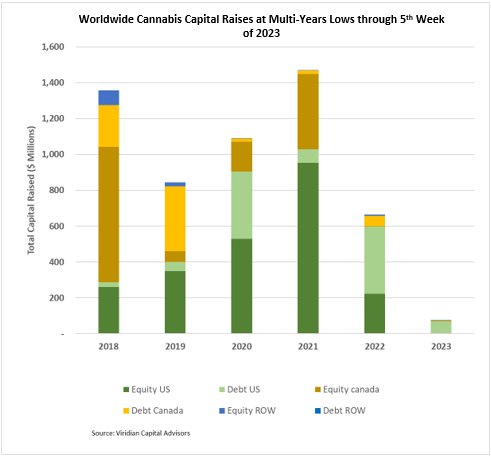

Cannabis capital raises are off to a multi-year low. Only $77.4M has closed through the first five weeks of the year compared to $662.9M last year.

- Public companies have raised 96.7% of total capital YTD.

VIRIDIAN INSIGHTS

- More indications of stress/distress appear in the market.

- On February 7, 2023, $1M AYR 12.50% bonds due 12/10/2024 traded on the CSE at 55, down from a previous $10M trade at 70 on January 25. It is shocking to see such heavy discounts for notes with such short maturities and high coupons issued by one of the country’s largest MSOs. The seller of these bonds is obviously none too confident of the company’s ability to refinance the debt between now and the slightly less than 2-year maturity. We are more optimistic about the company’s ability to satisfy this maturity. Still, we have noted previously that the $110M outstanding amount of this debt is quite large relative to the company’s current under $100M market cap. It demonstrates a fact about liquidity- it’s all about confidence and perception. Corporate bonds are rarely paid off from operating cash flows; they are almost always refinanced before maturity. If the market perceives that you are likely to be able to roll your debt, then a two-year maturity bond should begin to trade asymptotically closer to par. However, if there are doubts about your ability to refinance, then the same bond can begin to trade to a perceived recovery value, and yield calculations go out the window. Given last week’s MariMed deal at an effective cost of 19.7%, a two-year AYR 12.5% bond would likely trade at some discount, but a 50 price (which implies a yield to maturity of over 60%) is a whole other story!

- MedMen released their December quarter results, reminding us of an old lending joke: If you borrow $1000, you have a creditor, but if you borrow $100M, you have a partner. MedMen shows $15.6M of cash on its books and current liabilities of $237M, including a current portion of LTD of $66M. It wasn’t exactly a major news item when the company stated that it “…also needs to obtain an extension or a refinancing of its debt-in-default with the secured senior lender.” That lender is now Tilray, who purchased 75% of MedMen’s outstanding secured convertible notes from Gotham Green in August. So, what does Tilray do? It would be a major embarrassment to say, “OOPS! We messed up”, but we are certainly no closer to legalization than we were in August, which seems to be Tilray’s big hope here. It appears that Tilray has little choice but to keep doing what it takes to help MedMen survive, hoping that some fantastic event somehow makes them whole. Desperate times call for desperate actions.

- We are hearing more talk of groups assembling pockets of capital to pursue the acquisition of distressed assets. Much of this is focused on California, but opportunities abound in other developed markets that have been the chief victims of price compression.

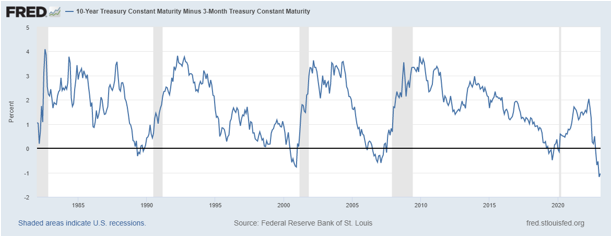

- The 3-month vs. 10-year treasury spread is still close to the most inverted since 1981, at negative 101bp (126bp last week). This inversion has successfully predicted the previous five recessions, and we don’t think it will miss this time either. But you wouldn’t know it if you have been looking at the S&P500 or meme stocks. Recession? What recession?

- The degree to which the premium end of cannabis holds up in the face of a recession is the big unknown. We don’t doubt that people will continue to consume cannabis relatively unchecked in the recession, but to what degree do they downscale into more affordable SKUs? Remember, the last recession, when people were being paid stimulus checks to stay home and smoke weed, is hardly a good predictor.

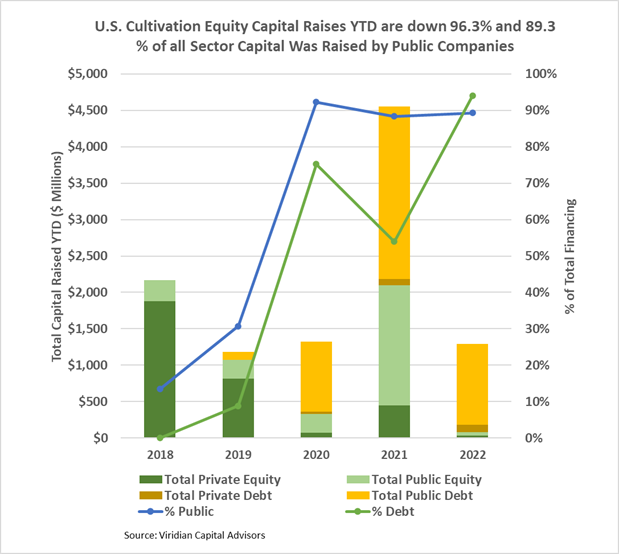

The U.S. Cultivation & Retail sector capital raises are down 71.6% YTD, but equity capital raised is down approximately 96.3%:

- Debt financing is down 50.6% YTD but accounts for about 94.0% of all capital raised; private companies raised 8.7% of it.

- 89.3% of total capital raises YTD were completed by public companies compared to 88.4% in 2021.

- In 2022, there have been no equity deals above $25M.

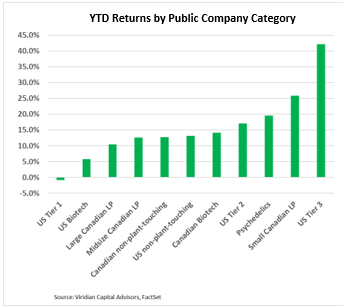

YTD Returns by Public Company Category

- Tier 1 MSOs continue to be the only category with negative YTD returns. Still, the category improved materially this week with gains of 13.6% by GTI (GTII: CSE), 12.6% by Columbia Care (CCHWF: OTC), and 11.2% by Verano (VRNOF: OTC).

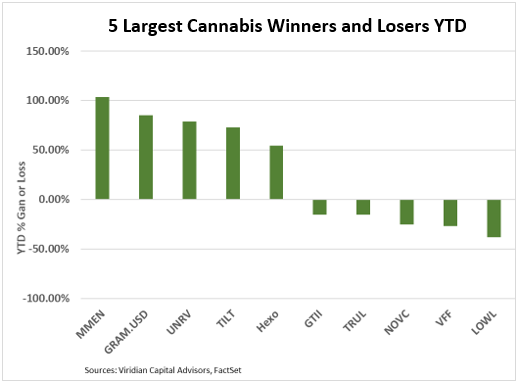

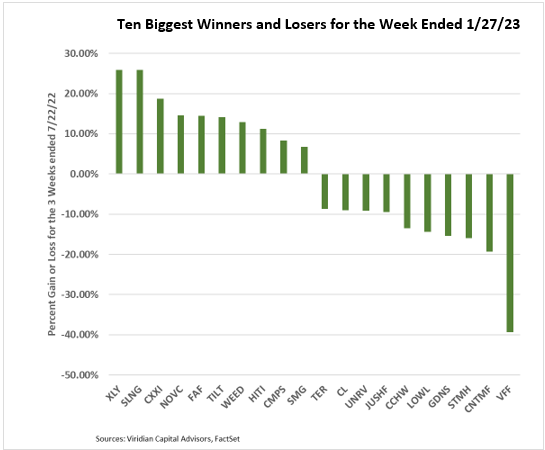

Best and Worst Performers of the last week and YTD

- Several of this week’s top gainers, including Auxly (XLY: CSE), Slang (SLNG: CSE), Fire & Flower (FAF: CSE), and Tilt (TILT: CSE), were bounce-backs from the loser list last week. The volatility is extreme, with several of these names up 10-20% this week after being down similar amounts last week.

- Lowell Farms (LOWL: CSE) repeats on the loser list, down 14.4% this week after a decline of 28% last week. The longer things go on without any news on the company, the more negative the market assumes the outcome will be. The reasoning is that everyone knows the company is for sale, and if there was buy-side interest, wouldn’t we have heard something by now? The argument is a bit too simplistic, but we have heard it from several respected sources this week.

- We are happy to report that our fears of contagion in the cannabis lender sector have proved unfounded. IIPR, AFC Gamma, NewLake Capital, and Chicago Atlantic all performed in the context of the market this week. The ability to book transactions like this week’s Chicago Atlantic/ MariMed deal is undoubtedly positive for the sector’s ability to raise funds.