OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

-

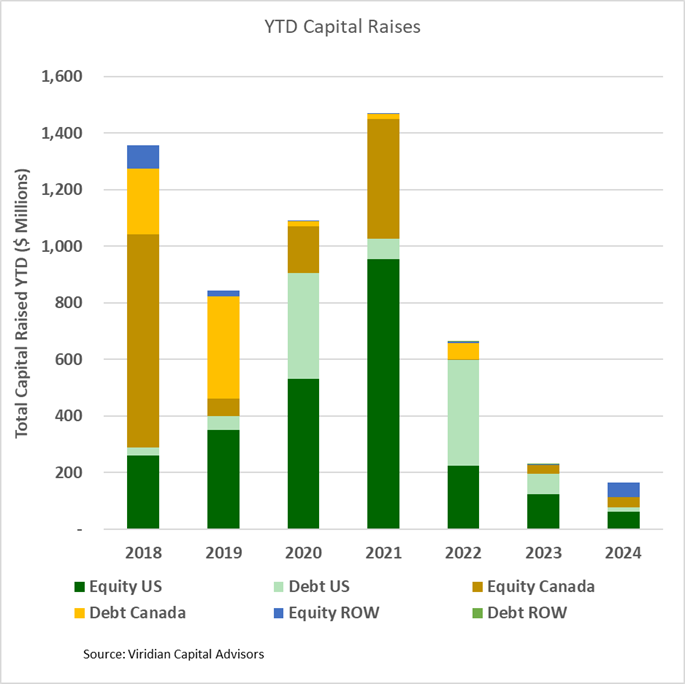

- YTD capital raises are down 29.5% since the same period in 2023. U.S. raises are down significantly more at -60.8%, with declines in equity and 3debt of 51.5% and 77.1%, respectively. Debt accounts for only 9.9% of total capital raised, the lowest percentage of any year since 2018 except for the bubble year of 2021. Countries other than Canada and the U.S. account for 31.1% of all capital raised (mainly U.K.), the highest percentage of any year on record at this point in the year.

VIRIDIAN INSIGHTS

- THE DEA WILL GO ALONG WITH RESCHEDULING TO LEVEL 3. However, the process may take longer than widely expected with public hearings and likely court appeals. Still, it will carry the day and be in place by year-end 2024. Yes, we do feel a bit gun-shy about predicting any positive cannabis regulatory or legislative change. Still, this one ostensibly can happen without any congressional vote, giving us more confidence.

- The SAFER ACT, HOWEVER, WILL CONTINUE TO STRUGGLE. WE HAVE DOUBTS THAT IT WILL BE ENACTED IN 2024. Internecine warfare in an election year will prevent any meaningful compromises from being reached. Senator Schumer will likely declare, “We are very close” for the umpteenth time only to fail to push it through. Frankly, the industry seems to have switched its focus to rescheduling, and the push for SAFER seems diluted.

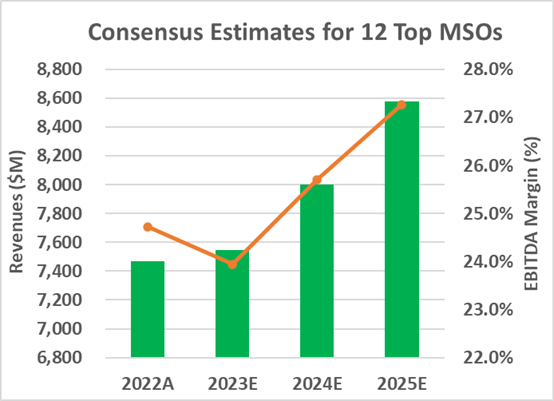

- NEW STATES DRIVE A RESURGENCE IN GROWTH AND INCREASED EBITDA. The chart below shows consensus revenue and EBITDA margin estimates for the top twelve MSOs.

- Analysts may be too cautious with the group’s 2024 revenue growth projection of 6.0%. A year of Maryland and Ohio and near-term price stability in several key markets suggests a higher growth expectation may be in order.

- Similarly, we believe the 25.7% 2024 consensus EBITDA margins may be too low as they are only 100bp higher than the 2022 figures. The industry found religion in 2022 and 2023, stringently managing costs and tightening working capital controls. The industry is poised to be more efficient and profitable as growth returns.

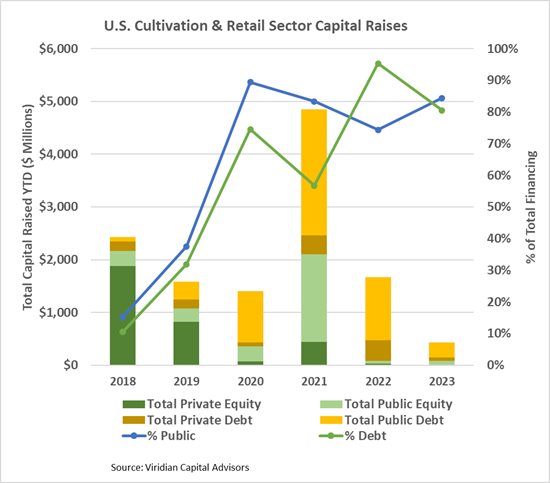

- THE CANNABIS CAPITAL MARKETS WILL SEE A MODEST RESURGENCE BASED ON RENEWED REVENUE AND EBITDA GROWTH AND A GROWING LIKELIHOOD OF RESCHEDULING. We all thought 2022 was a lousy year until we saw 2023! Worldwide cannabis capital raises dropped 57.3% from 2022, nearly 56% lower than the last capital freeze year in 2020. The cultivation and retail sector, which generally accounts for over half of all capital raises, was particularly hard hit: total capital raises of around $400M were off 75% from an already horrible year in 2022.

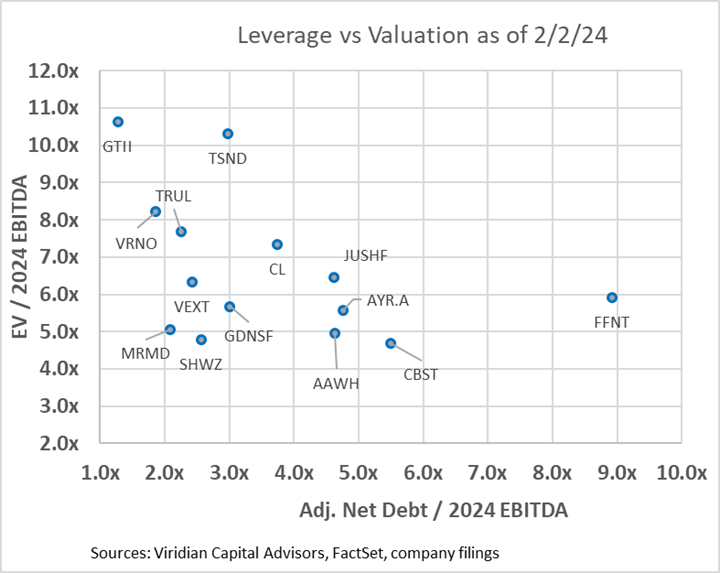

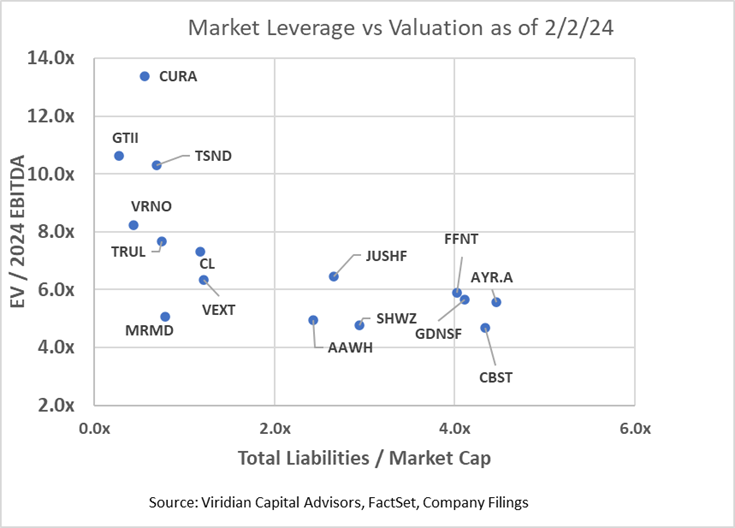

- The two graphs below show the Enterprise value to 2024 EBITDA multiples against two leverage measures. In the first graph, we have calculated an Adjusted Net Debt/ 2024 EBITDA figure by adding any accrued taxes over 90 days of tax expense to debt before subtracting cash to arrive at Adjusted Net Debt. We would expect any regular company to have accrued taxes equal to their last quarterly tax expense and consider that a standard working capital item. Several companies on the chart have far greater than 90 days of accrued taxes, and we consider the excess to be debt. Verano’s excess tax liabilities equal nearly 40% of its debt. Other companies with relatively high imputed tax debt include Curaleaf (CURA: CSE) and 4Front (FFNT: CSE) at 19%, and Terrascend (TSND: TSX) at 17%.

The analysis in our rescheduling discussion shows that 3x debt is unsustainable in a 280e environment and results in relatively uncomfortable debt payback periods of close to 5 years, even in a post-280e world. Accordingly, companies with adjusted net debt/2024 EBITDA over 3x and reasonable valuations will seize on likely catalyst-driven upswings in equity prices to sell meaningful amounts of equity and reduce debt. 4Front and AYR (AYR.A: CSE) have shown that lenders are extracting heavy tolls for amendments/extensions or debt-to-equity conversions, making those options unattractive. Granted, paying down debt is not a favored use of equity proceeds. However, a straight equity issuance may be the best option, given that leverage is too high.

- CANNABIS DEBT SECURITIZATION WILL TAKE OFF IN 2024. We believe the Pelorus securitization transaction completed in July was one of the most critical developments in cannabis debt of the past five years. Securitization is a logical extension of the cannabis debt markets, and the creation of over-secured tranches of debt based on diversified pools of loans will bring major institutional investors who have, to date, avoided the cannabis space into the market. Subsequent developments of credit default swaps will eventually aid in reducing cannabis credit spreads to levels approaching high-yield debt. This will not happen overnight, but the process has begun.

- 2024 WILL BE THE YEAR INVESTORS DISCOVER CANNABIS DEBT. We were talking with investors at a recent conference, and one told us that he viewed GTI stock as a cash equivalent. We beg to differ. On the other hand, senior secured debt of companies like Ascend Wellness, at yields approaching 16%, D.O. seem attractive places to park cash while waiting for greater clarity on rescheduling and SAFER. After seeing two-year losses of around 90% on their equity investments, we think investors should look hard at the underlying debts of these same companies. Viridian publishes credit rankings of these companies every week with indicative debt pricing. Will investors brave a new market for exceptional yield, or are investors still convinced they can time the upswing in cannabis stocks despite years of evidence to the contrary?

- CANNABIS M&A WILL BOUNCE BACK FROM ITS LOWEST YEAR EVER IN 2023. Despite its promising potential for rescheduling and legislative reform, 2024 will not immediately differ from 2023: capital markets remain challenged, and profitability is squeezed. Still, our Valuation Gap analysis (presented in the M&A section, indicates that large MSOs now possess the highest EV/NTM EBITDA multiple advantage that they have had since November 2021, augmenting the possibility of accretive transactions. So, even though the year is off to an even slower start than 2023, we are sticking to this prediction.

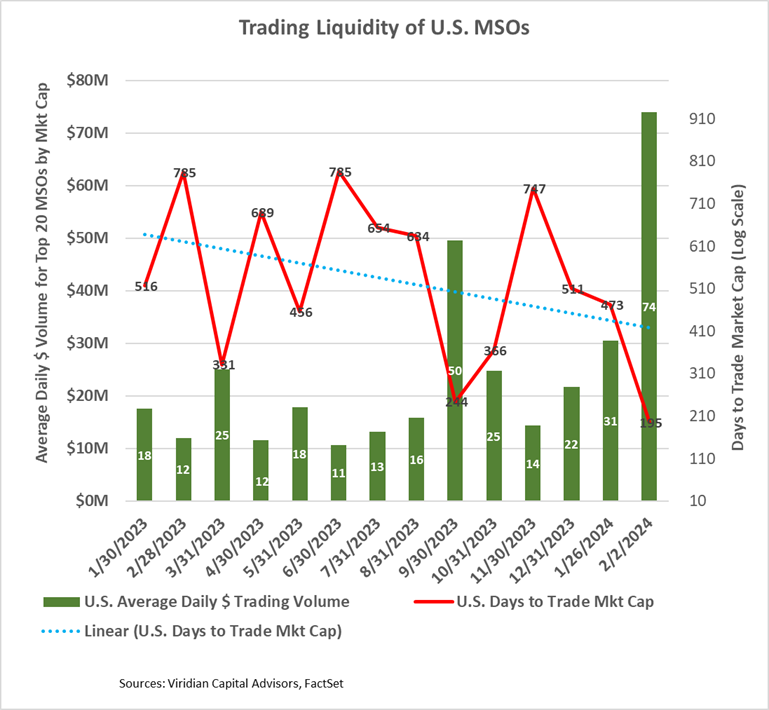

- CANNABIS STOCK LIQUIDITY IS SLOWLY IMPROVING

- The graph below depicts the trading liquidity of the fifteen U.S. MSOs with market caps over $100M as of 2/2/24. The green bars (measured on the left axis) show the group’s aggregate average daily dollar trading volume. The average daily trading volume of $74M for the week ended 2/2/24 significantly exceeded any period in the last 52 weeks, including the weeks immediately after the HHS announcement. There has been no specific news to drive this acceleration, just the pervasive and growing belief that a DEA announcement is likely soon. The red line (measured on the right axis) shows the aggregate Days to Trade the Market Cap. (DTMC). The 195 days is down sharply from the 747 days registered in November but still represents significant illiquidity. As an illustration, if an investor took a 5% position in a stock with a 195 DTMC and wanted not to be over 25% of the average daily trading in the stock (so as not to disturb the market), it would take him 39 days to trade out of his position. The equivalent calculation for the top 5 Canadian LPs (trading on Nasdaq) is approximately seven days, illustrating the importance of up-listing. The dotted blue line shows DTMC’s improving trend.

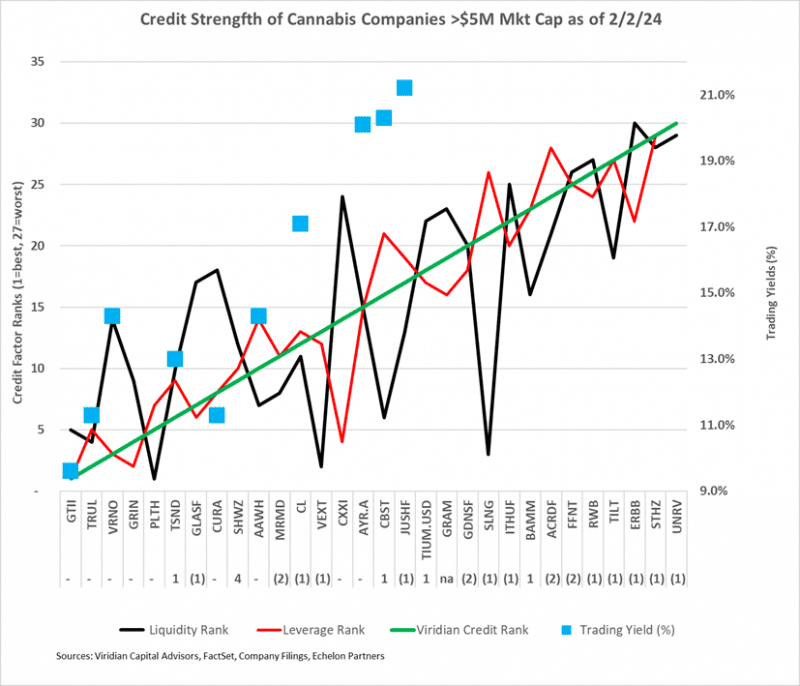

- GIVING CREDIT WHERE CREDIT IS DUE

- The chart below shows our updated 2/2/24 credit rankings for the 30 U.S. cannabis companies with over $5M market cap. This week, we added Gold Flora (GRAM: NEO) to the list and eliminated MedMen. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement.

- The blue squares show the offered-side trading yields for each company. Trading yields have declined significantly since the HHS rescheduling announcement.

- Trulieve and Curaleaf market yields have come down by as much as 200 basis points since the beginning of the year, and we now think that Curaleaf has gotten a bit rich relative to our perception of its credit quality. At current prices, we would prefer to be in the TerrAscend (Gage) paper, which we rank as a better credit, offered at 150bp higher yield.

- AYR’s new 13% Sr. Secured Debt due 2026 has also moved in the direction we predicted last week, quoted approximately five points higher to yield 20.1% to the 2026 maturity, about 100bps lower yield than Jushi’s second lien paper and still attractive in our view.

- The most significant credit move of the week was the four-notch improvement by Schwazze (SHWZ: OTC), primarily because the company had one of the best-performing stocks of the week, reducing relative market leverage indicators. Cannabist (CBST: CBOE) continued to climb in the rankings, rising to #16. The Viridian Capital Credit Tracker ranks Cannabist as a slightly weaker credit than AYR, and its trading yield mirrors that evaluation.

- NOTHING MATTERS BUT RESCHEDULING

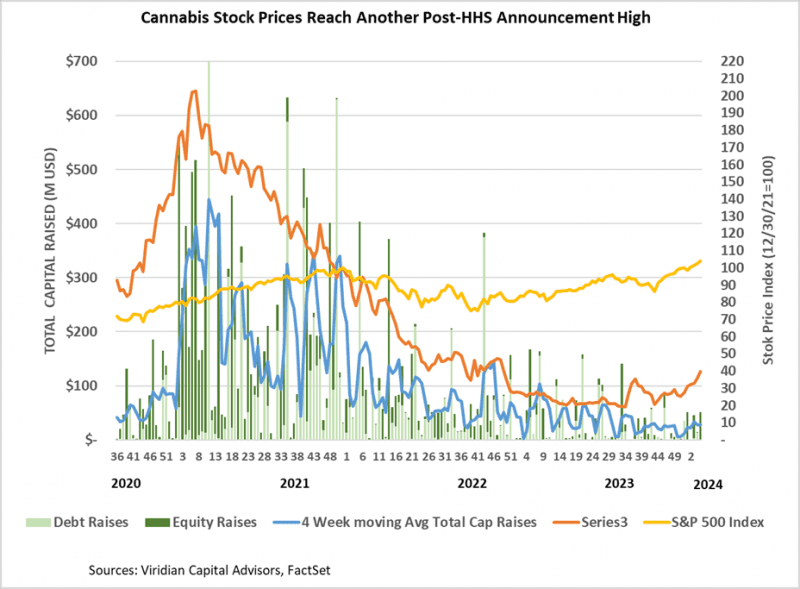

- The HHS recommendation to reschedule cannabis to Schedule 3 dramatically impacted equity prices, propelling the MSOS ETF upwards sharply. As of 2/2/24, the ETF was up 108.4% since the rescheduling news.

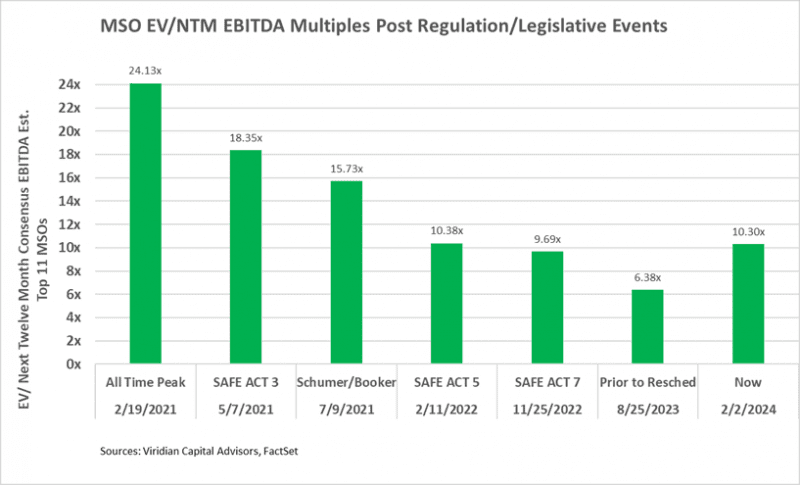

- The chart below shows enterprise to next-twelve-month valuation multiples now compared to previous times when positive regulatory/legislative news hit.

- EV/NTM EBITDA Multiples are now roughly equal to the levels after the 5th SAFE Act passage in the House in February 2022. Still, the rescheduling news is more significant as it dramatically impacts cash flows. If valuations multiples rose to where they were after the announcement of the Schumer-Booker bill, the incremental gains would equal 52.4%. We view a DEA announcement ratifying the HHS recommendation to be much more significant than introducing the Schumer-Booker bill, which most observers viewed as DOA and had no immediate impact on operator cash flows. Accordingly, we believe there is considerably more runway for price increases, perhaps reaching the 5/7/21 multiples of 18.35x, producing 78% returns from current levels.

FINANCIAL IMPACTS OF REMOVING 280e

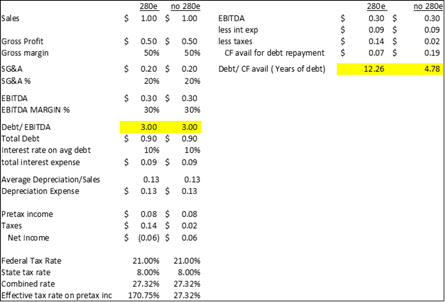

- The table below demonstrates that for a hypothetical cannabis company with 50% gross margins, 20% SG&A, and 3x Debt/ EBITDA, 280e can result in effective tax rates (on pretax income) of over 100%.

- The table demonstrates our previous claim that debt/EBITDA over three times is unsustainable in a 280e world, as the calculated payback period for the debt would be an unacceptable 12.26 years. Cannabis companies under 280e need less than 2x debt/EBITDA to have acceptable 5-year payback periods. The table shows that combined effective rates (depending on state tax rates) would be reduced to around 27% without 280e, making a considerable difference in debt capacity.

- Without 280e, companies could carry 3x leverage with acceptable payback periods. By making interest expense tax deductible, the elimination of 280e also reduces the cannabis cost of capital and increases the intrinsic value of the firms.

- Removing 280e would still not support the level of debt we now see in the industry. Six of the top sixteen companies have adjusted net debt/2024 EBITDA over 4x, which is unsafe even without 280e, especially given ongoing cost inflation and wholesale price compression.

-

-

- We estimate annualized tax savings of the top 13 MSOs at $700M.

-

- No Cultivation and Retail sector capital raises closed in the first few weeks of 2024, and we expect capital markets to remain tight until more clarity arises regarding rescheduling. The graph below shows annual cultivation & retail trends over the last few years.

- Cannabis equities (as measured by the MSOS ETF) were up 11.95% for the week to close at post-HHS announcement highs on continued market belief in a near-term DEA announcement.

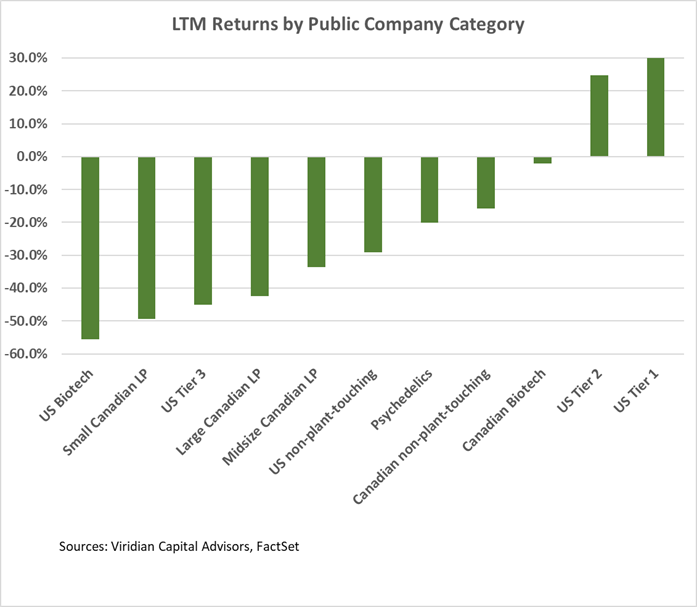

Trailing 52-Week Returns by Public Company Category:

- Unsurprisingly, U.S. Tier One MSOs continue performing best out of our eleven categories. Our Tier 3 basket continues to show negative 52-week returns dragged down by losses by MedMen, Tilt, Red White & Bloom, StateHouse, and Unrivaled.

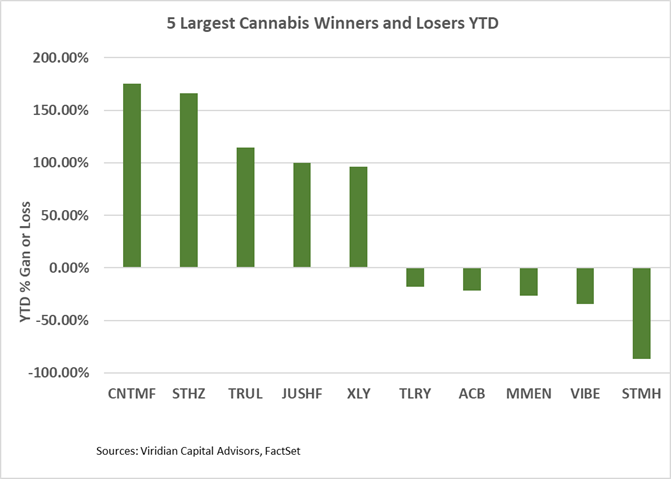

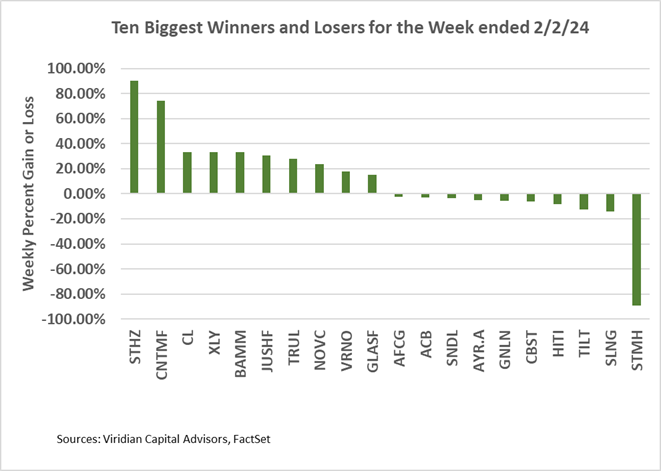

Best and Worst Performers of the last week and YTD:

- The week’s top gainers included Cansortium (CNTMF: OTCQB) and Trulieve (TRUL: CSE), both of which stand to gain from adult rec making it to the Florida ballot box. There are still significant hurdles to overcome, including the Florida Supreme Court and the 60% vote requirement, but based on the Governor’s statements, the issue will be on the ballot.

- Cannabist (CBST: CBOE) continued on the losers list this week because of its announcement to repurchase $25M of its 6% senior secured convertible notes due June 2025 using stock at discounts to the market price. The transaction illustrates a theme we expect will recur in 2024 unless rescheduling happens quickly: shareholders taking near-term pain to stabilize over-levered balance sheets. Cannabist credit rankings have been improving while its stock has been punished.