OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

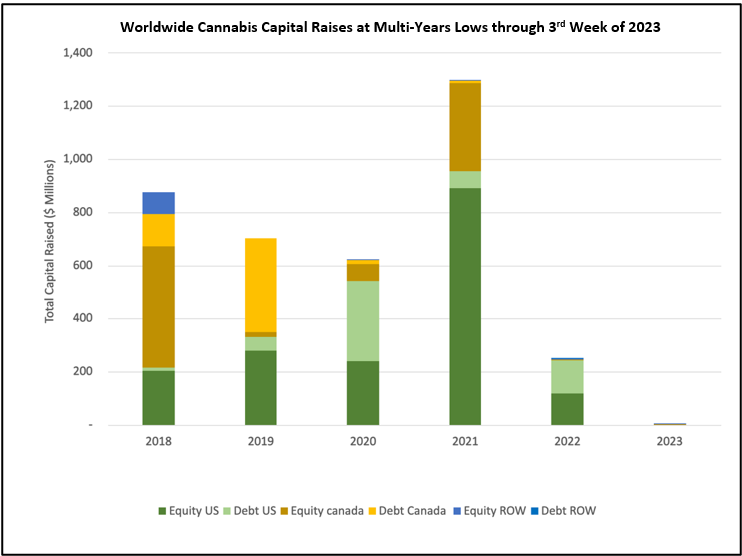

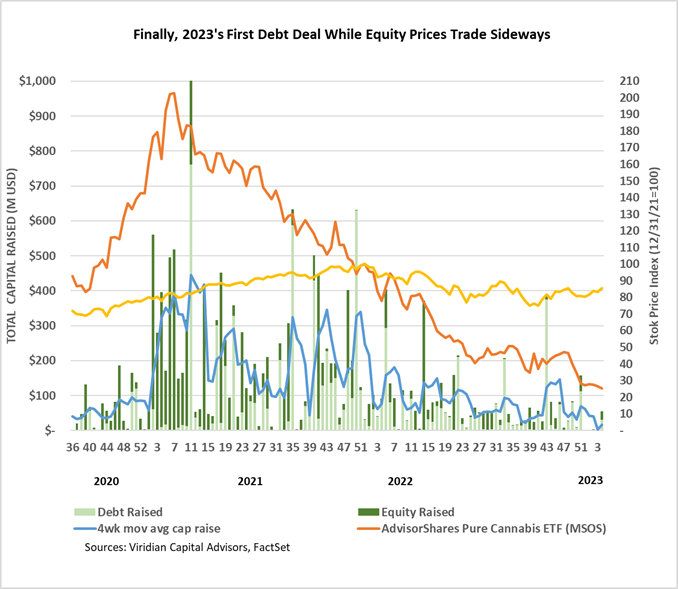

Cannabis capital raises are off to a multi-year low. Only $5.9M has closed through the first four weeks of the year compared to $248.0M last year.

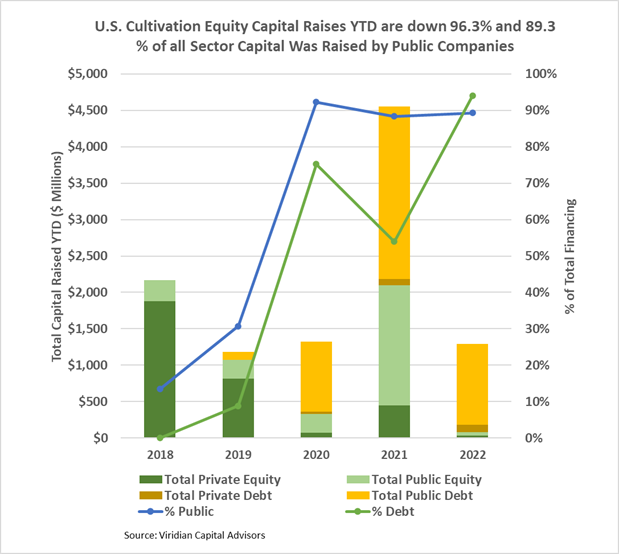

- Public companies have raised 56.7% of total capital YTD.

The U.S. Cultivation & Retail sector capital raises are down 71.6% YTD, but equity capital raised is down approximately 96.3%:

- Debt financing is down 50.6% YTD but accounts for about 94.0% of all capital raised; private companies raised 8.7% of it.

- 89.3% of total capital raises YTD were completed by public companies compared to 88.4% in 2021.

- In 2022, there have been no equity deals above $25M.

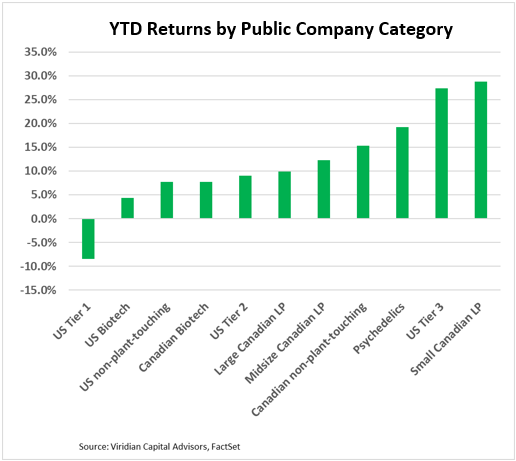

YTD Returns by Public Company Category

- Tier 1 MSOs continue to be the only category with negative YTD returns. The sector was weighed down this week by abysmal performances by Cresco (CL: CSE), Columbia Care (CCHWF: OTC), and TerrAscend (TER: CSE), all down between 8.5-10% on the week.

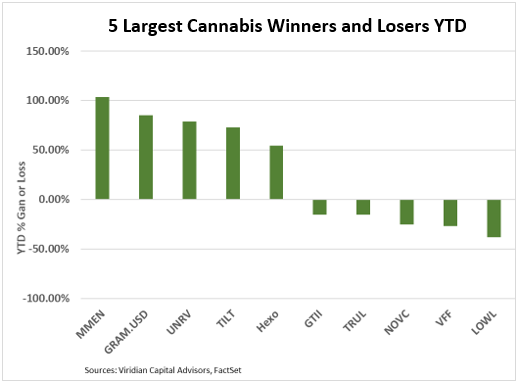

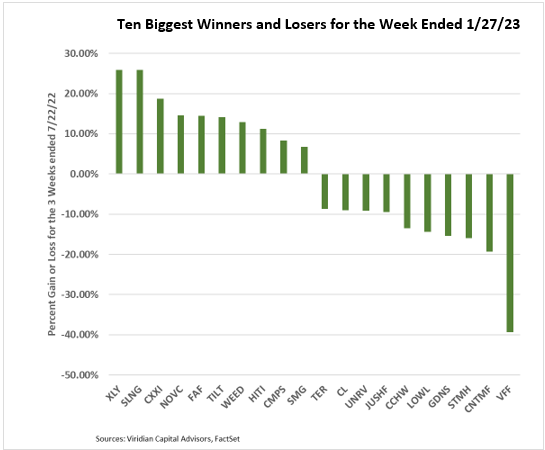

Best and Worst Performers of the last week and YTD

- Several of this week’s top gainers, including Auxly (XLY: CSE), Slang (SLNG: CSE), Fire & Flower (FAF: CSE), and Tilt (TILT: CSE), were bounce-backs from the loser list last week. The volatility is extreme, with several of these names up 10-20% this week after being down similar amounts last week.

- Lowell Farms (LOWL: CSE) repeats on the loser list, down 14.4% this week after a decline of 28% last week. The longer things go on without any news on the company, the more negative the market assumes the outcome will be. The reasoning is that everyone knows the company is for sale, and if there was buy-side interest, wouldn’t we have heard something by now? The argument is a bit too simplistic, but we have heard it from several respected sources this week.

- We are happy to report that our fears of contagion in the cannabis lender sector have proved unfounded. IIPR, AFC Gamma, NewLake Capital, and Chicago Atlantic all performed in the context of the market this week. The ability to book transactions like this week’s Chicago Atlantic/ MariMed deal is undoubtedly positive for the sector’s ability to raise funds.