OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

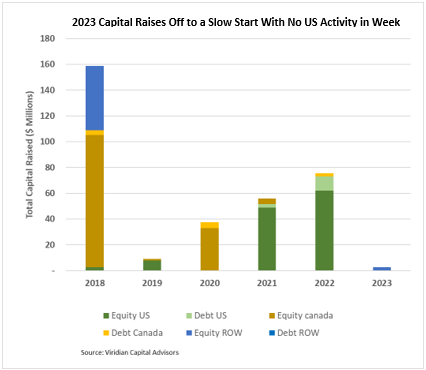

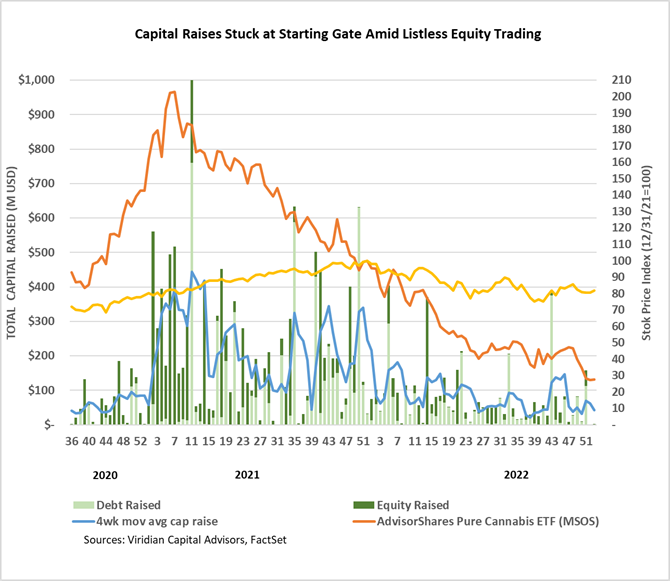

Cannabis capital raises for the first week of 2023 were down 95.7% from W1 2022:

- No debt issues were closed this week.

- Private companies dominated financing in the first week of the year, raising 95.3% of the funds.

- No U.S. Issues were closed in W1 2023.

- Israel represented 95.3% of total capital raises.

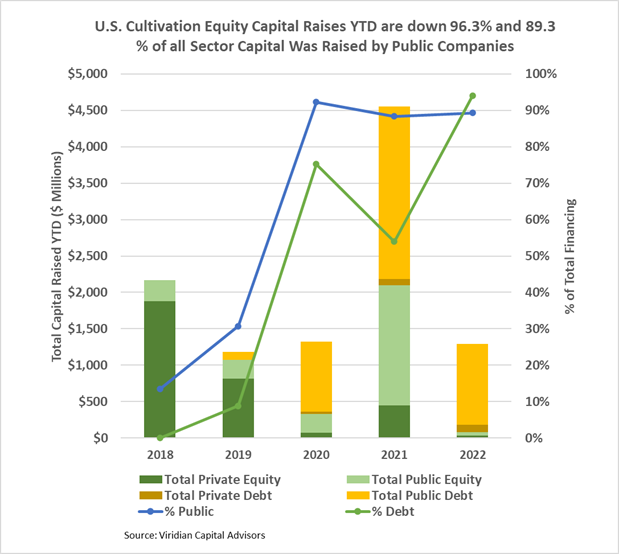

The U.S. Cultivation & Retail sector capital raises are down 71.6% YTD, but equity capital raised is down approximately 96.3%:

- Debt financing is down 50.6% YTD but accounts for about 94.0% of all capital raised; private companies raised 8.7% of it.

- 89.3% of total capital raises YTD were completed by public companies compared to 88.4% in 2021.

- In 2022, there have been no equity deals above $25M.

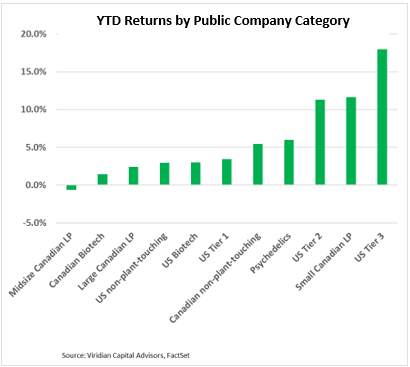

YTD Returns by Public Company Category

- It’s a new year, and returns are positive across most categories of cannabis-related companies.

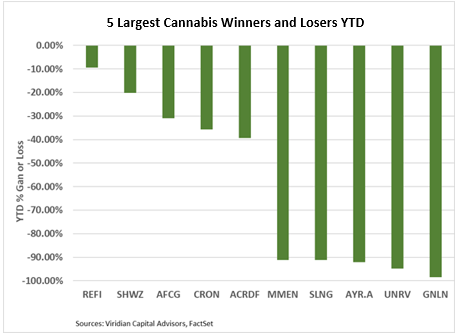

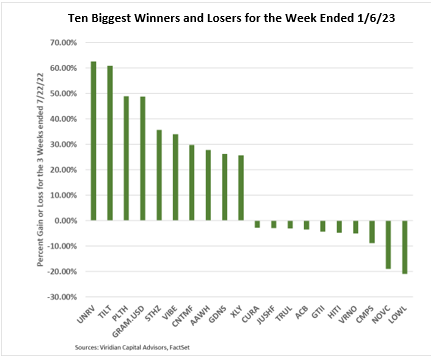

Best and Worst Performers of the last week and YTD

- Unrivaled Brands (UNRV: OTC) was up 62.5% for the week on news that it entered a security placement agreement to sell $2M of convertible preferred stock units to investors, including the company’s CEO, CFO, and CLO.

- Tilt Holdings (TILT: NEO) was up 60.8% on news that the company has retired $33.7M of its $35.8M principal amount of senior secured notes and extended the maturities of the remaining $2.1M to February 2023. Tilt also obtained a fifth amendment to its agreement with Innovative Industrial Properties (IIPR: NYSE), extending the investigational period on the transaction to February 2023.

- Top losers included Lowell Farms (LOWL: CSE) and Nova Cannabis (NOVC: CSE), both on the top gainers list in the previous week.