OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

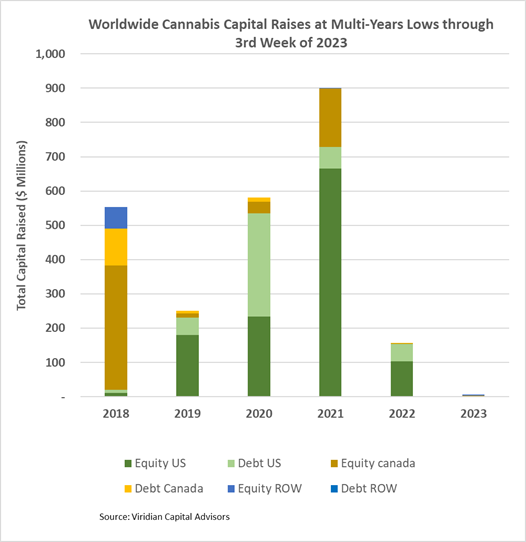

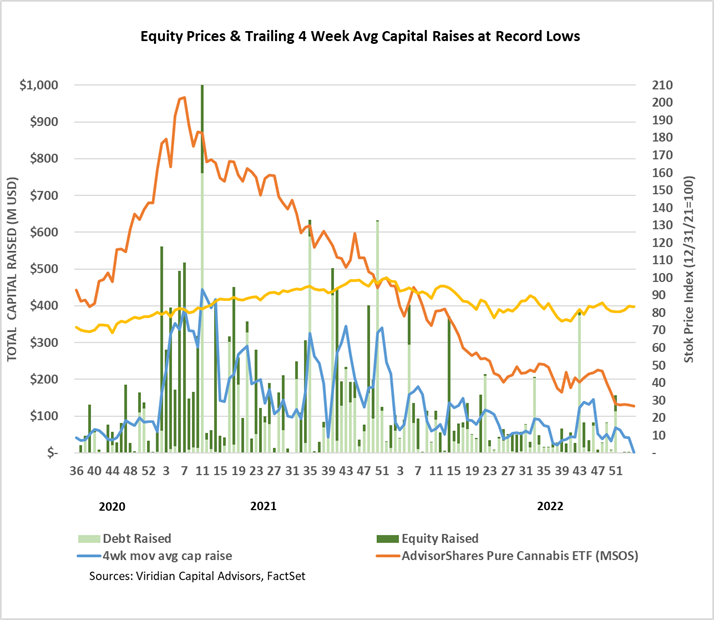

Cannabis capital raises are off to a multi-year low. Only $5.9M has closed through the first three weeks of the year compared to $157.2M last year:

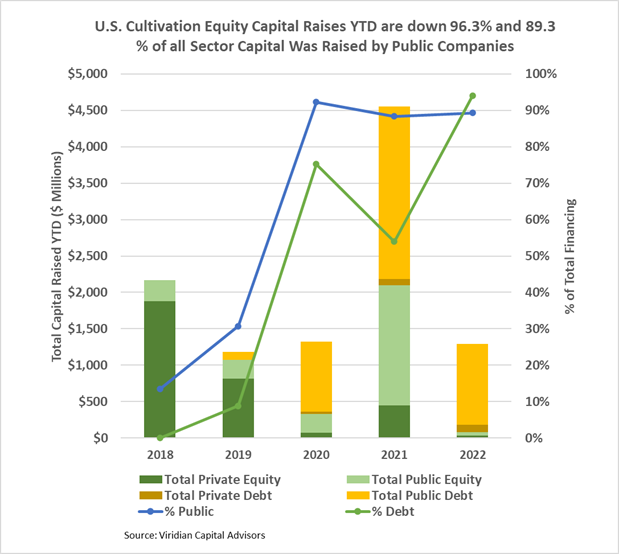

- Public companies have raised 56.7% of total capital YTD.

The U.S. Cultivation & Retail sector capital raises are down 71.6% YTD, but equity capital raised is down approximately 96.3%:

- Debt financing is down 50.6% YTD but accounts for about 94.0% of all capital raised; private companies raised 8.7% of it.

- 89.3% of total capital raises YTD were completed by public companies compared to 88.4% in 2021.

- In 2022, there have been no equity deals above $25M.

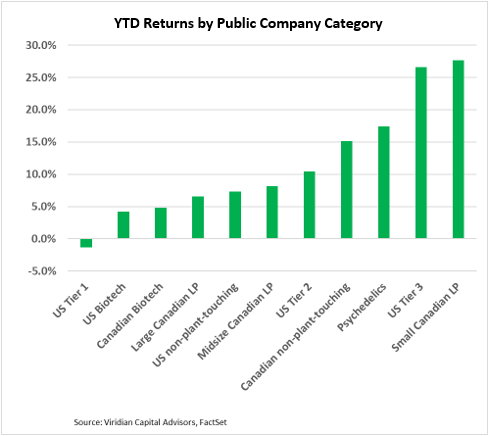

YTD Returns by Public Company Category

- Returns continue to be positive across all public company categories YTD. Tier one U.S. MSOs remain the weakest category, while Tier three U.S. companies have been the best performers. The most significant change from last week is the relatively improving performance of the Psychedelic category, which now ranks as the third-best performer YTD, up from the sixth-best last week.

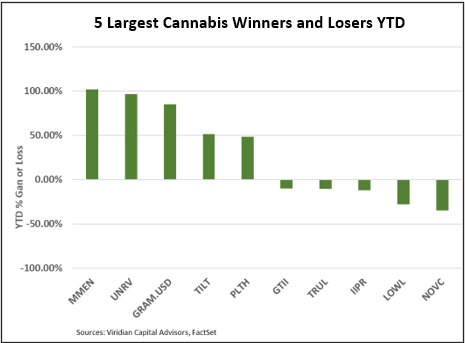

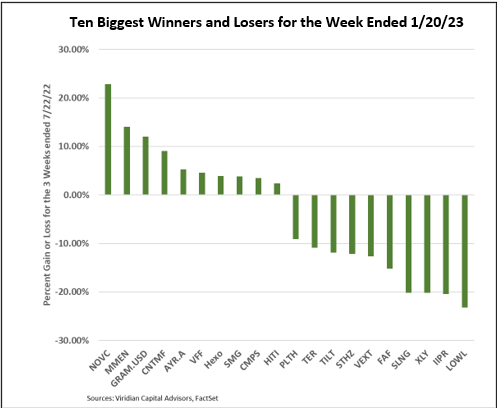

Best and Worst Performers of the last week and YTD

- Nova Cannabis (NOVC: CSE) tops the leader list this week after topping the loser list last week. We are unsure what to make of this except that it begs for a long straddle option position.

- The loser list is much more understandable. Lowell Farms was the biggest loser, down nearly 28% for the week. We hope we are wrong, but it strikes us that when you present a long list of “strategic alternatives,” and one of them is restructuring, you have biased the result in that direction. After all, would you want to enter into a long-term brand royalty agreement with a company in trouble? But, as we said in our commentary last week, the brand is undoubtedly valuable, and the apparent stabilization of the California market is hopeful.

- Innovative Industrial Properties (IIPR: NYSE) was the other big loser this week, down 20.5% on the announcement that three of its properties are in default and that it is looking for a non-cannabis tenant for one of the properties it took back this year. Our Friday Tracker wrap-up went into much more detail, but suffice it to say that we are primarily concerned about the chilling effect this may have on the cannabis sales leaseback and debt financing market.