OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

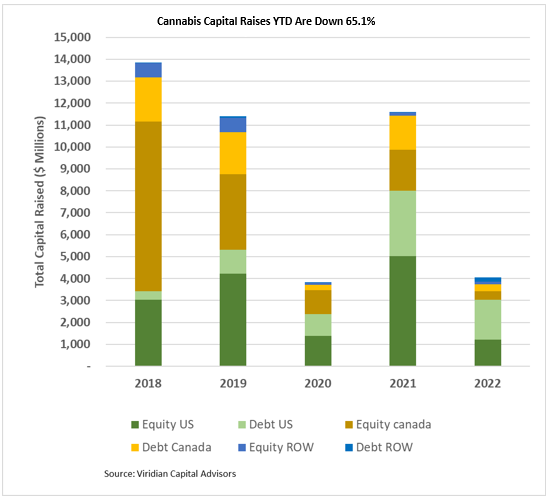

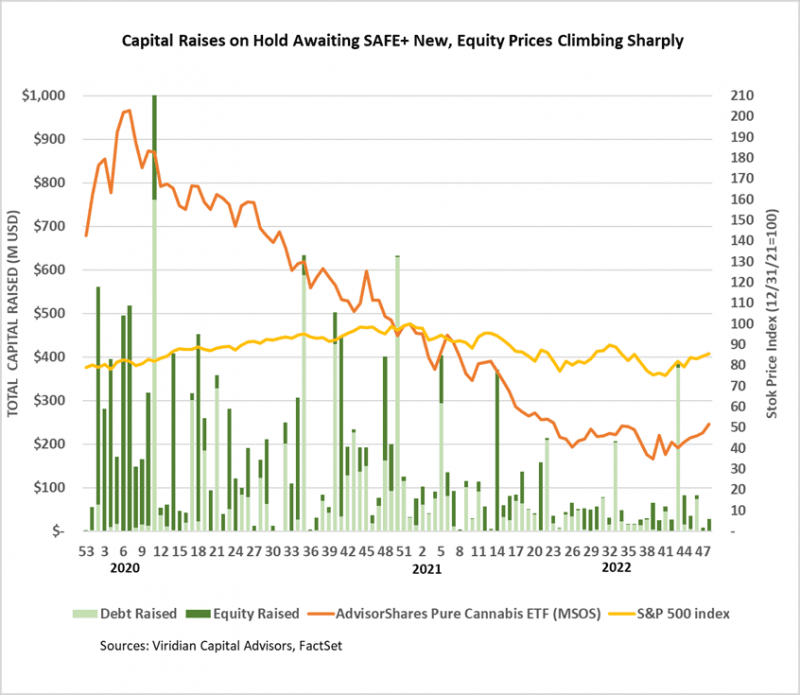

Cannabis capital raises are off 65.1% YTD:

- Total Equity issuance is off 75.3%, and total debt issuance is down 49.2%.

- U.S. debt is down only 38.7%, while Canadian debt is down a more significant 75.8%.

- At 57.1% of total capital raised, debt remains the highest in history for comparable periods.

- Public companies accounted for 74.5% of total financing YTD, down from 79.6% in 2021.

- The graph below shows that U.S. activity dominated capital raises for the first forty-eight weeks of 2022, with 75.2% of all capital raised.

- International capital raises of $318.7M represented 7.9% of total capital raises, exceeding the previous record of 6.3% in 2019.

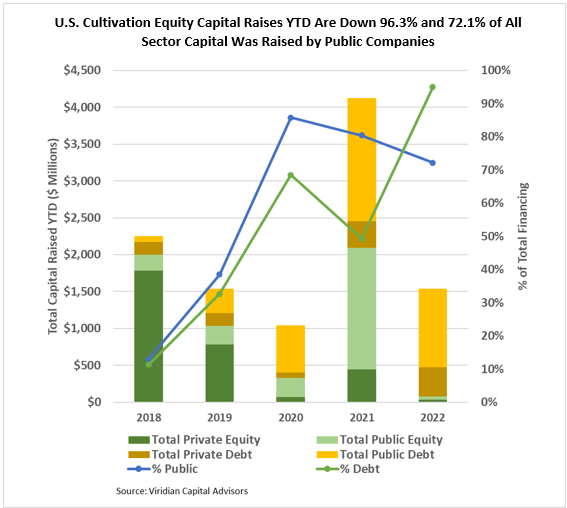

The U.S. Cultivation & Retail sector has experienced a similar change in capital raise activity, although the components have changed significantly:

- Total capital raised is down 62.7%, but equity capital raised is down approximately 96.3%.

- Debt financing is down 28.1% YTD but accounts for about 95.0% of all capital raised; private companies raised 25.7% of it.

- 72.1% of total capital raises YTD were completed by public companies compared to 80.4% in 2021.

- In 2022, there have been no equity deals above $25M.

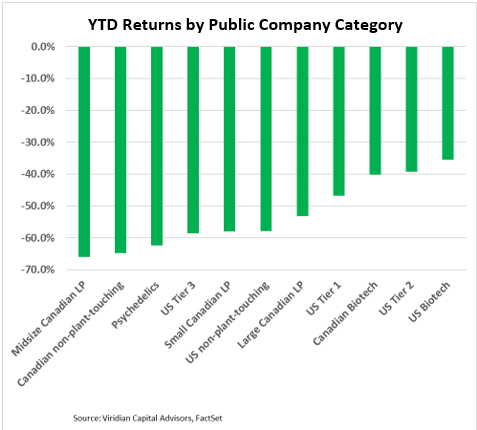

YTD Returns by Public Company Category

- Psychedelics recovered one ranking position in our listing of YTD performance by category.

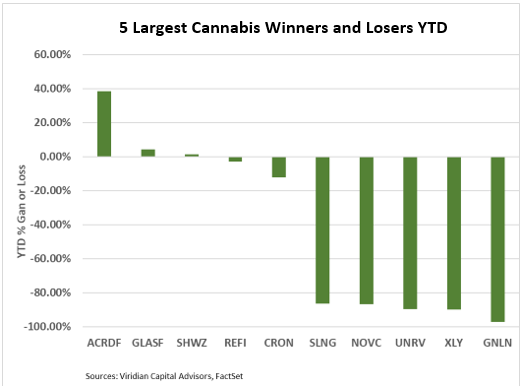

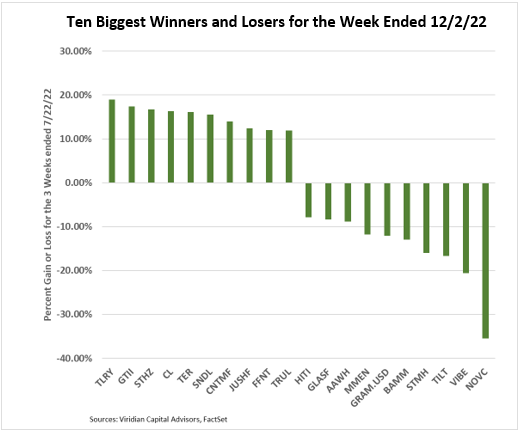

Best and Worst Performers of the last week and YTD

- Green Thumb (GTII: CSE), Cresco Labs (CL: CSE), Trulieve (TRUL: CSE), and TerrAscend (TER: CSE) were all on our top ten gainers list based entirely on the swirling SAFE rumors.

- Nova Cannabis (NOVC: CSE) and Tilt Holding (TILT: NEO) were sharply lower after being on last week’s biggest gainer list. We saw no particular news to explain the swing.