OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

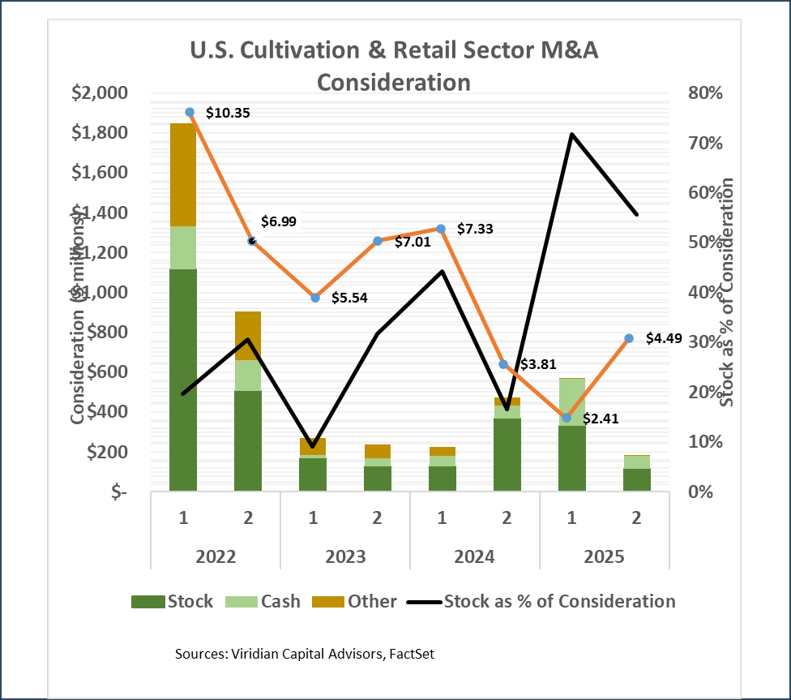

- M&A activity targeting the U.S. Cultivation and Retail sector (as shown by the stacked bars aggregating the components of consideration) plunged after the first half of 2022. One contributing factor was the cratering of equity prices (represented by the MSOS ETF price shown by the orange line). Notice the close correlation between the movements of stock prices and the percentage of stock used as consideration. Another factor was the tightening of the capital markets. The plant-touching equity market, in particular, has been in a virtual lockdown.

- Still, transaction volume has picked up modestly, with 2024 and YTD 2025 running far ahead of the dismal showing in 2023.

- The black line on the graph shows the percentage of merger consolidation paid in stock. The rise in 2025 is largely due to the all-stock deals completed by Vireo in their acquisitions of Wholesome, Proper, Deep Roots, and the majority of the senior convertible notes of Schwazze.

- Rescheduling is likely to Re-Ignite M&A activity.

- Equity prices are likely to increase faster than new capital inflows, as banking reform and uplisting activity are hindered by legislative paralysis. It will become increasingly advantageous to utilize equity in M&A deals rather than raising capital in the capital markets.

- Our weekly Valuation Gap chart shows that in rising markets, Tier 1 valuations rise relative to those of Tier 2, Tier 3, and private competitors, making acquisitions more accretive than they are currently.

- The bargaining power of tier-one MSOs will continue to rise relative to their smaller and generally private targets as the cost of capital differentials begins to increase.

- A significant number of smaller competitors are “tired” of the battle they have been forced to wage over the last two years and are now candidates for sale.

- We do not anticipate many large public/public consolidations, but expect the larger MSOs to become more willing to use their re-rated stocks in pursuing consolidation in markets where they already have a strong presence.

- Rescheduling will initially have a larger impact on M&A than on capital raises, meaning that stock is likely to rise as a percentage of M&A consideration. Sellers holding out for cash deals will need to be patient. Strong inflows from institutional investors are likely to require at least some version of the SAFER Act, and in the meantime, cash will remain tight.