OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

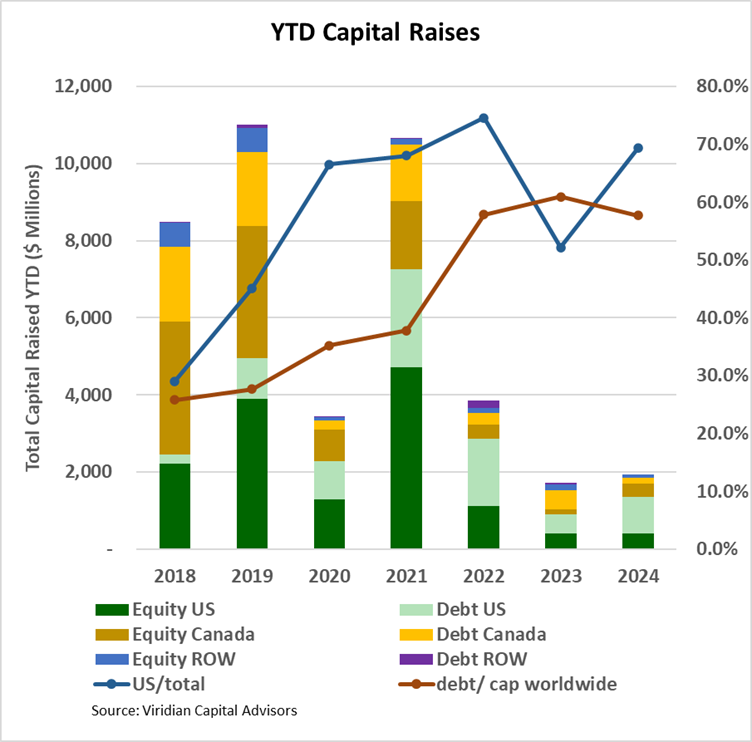

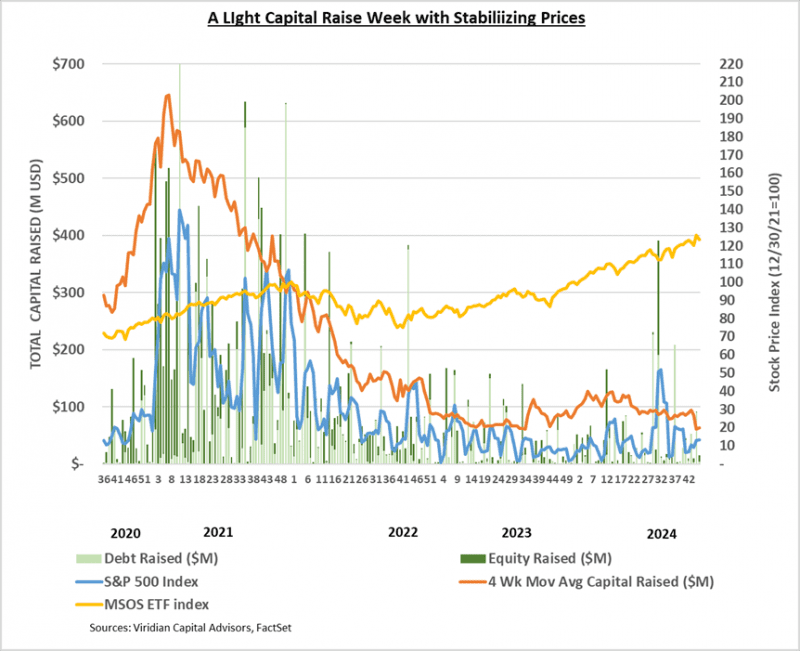

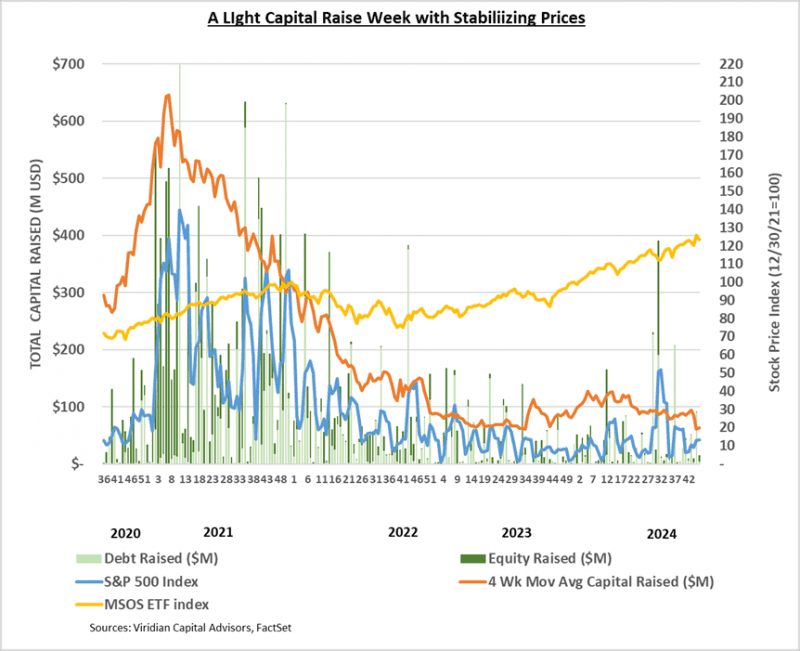

- YTD capital raises totaled $2,073.52M, up 13.7% from the same period in 2023. Debt as a percentage of capital raised dropped to 59.1% from 61.3% in the previous year on a worldwide basis. The U.S. bucked this trend with 71.4% of capital raised in debt compared to 57.6% in 2023.

- U.S. raises accounted for 70.7% of total funds, up from 52.8% at the same point in 2023. Raises from outside Canada and the U.S. represented 5.0% of the total funds raised, which is in line with the average of 5.7% for the six previous years but is sharply lower than the 10.7% achieved in 2023.

- YTD raises by public companies accounted for 76.6% of total funds, the highest since 2021.

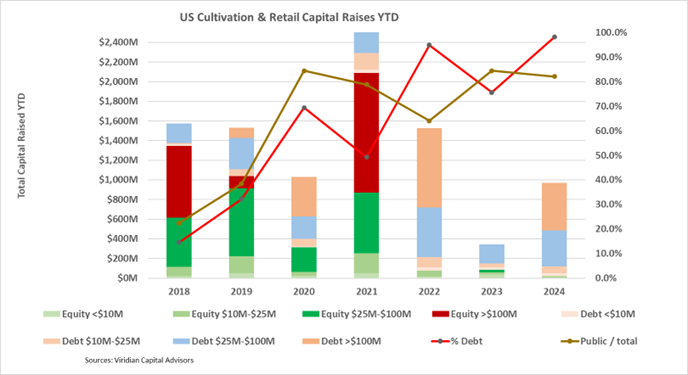

- Cultivation and Retail Sector capital raises are up 182% YTD. Debt accounts for 98.2% of the $971.5M raised YTD, and around 70% of this is earmarked for refinancing existing debt. Large debt issues (>$100M) bounced back and represented 50.1% of capital raised compared to zero in 2023.

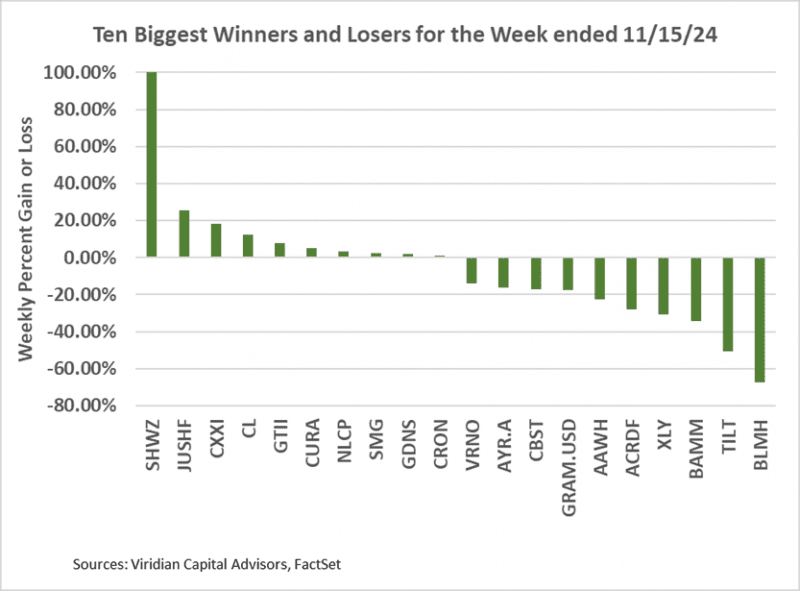

- Cannabis equities (as measured by the MSOS ETF) ended down 3.48% for the week, which is not much consolation after last week’s largest decline in the ETF’s history (since September 2020). The market was encouraged by the Matt Gaetz nomination for attorney general.

VIRIDIAN INSIGHTS

- WILL THE PROPOSALS FOR THE NEW FARM BILL QUELL THE “GROWTH PANIC”

- We believe one of the reasons for the recent sharp decline in cannabis stocks is that without FL, PA, or VA, it is difficult to point to the next catalyst for a growth spurt.

- The problem is exacerbated by the continued price compression experienced in nearly every market once it gets past its first 12-18 months of adult use. New Jersey is an example of price compression that is beginning to be felt. Developed markets like Michigan, which have already experienced severe price declines, continue to see even more.

- Nearly perfect competition from the illicit market and hemp-derived cannabinoids further reduce growth potential.

- Finally, a firmer outline of the new Farm Bill is beginning to take shape, and it is not kind to hemp cannabinoids. Some variants actually take the allowed THC to zero, although we do not believe this can stand due to the “hot hemp” issue, which would make this standard impractical. Nonetheless, the Bill is receiving rave reviews from cannabis corners and is likely to firm stock prices.

- OUR CHART OF THE WEEK ON OPTION-BASED VALUATION FOR CANNABIS DISTRESSED CANNABIS EQUITIES SUGGESTED A CHANGE IN THINKING

- The counterintuitive idea that option pricing suggests is that investors in distressed equities need to embrace volatility and risk. In fact, if you want to invest in distressed equities, you should focus on the riskiest and most volatile industries you can find, such as cannabis.

- And as an owner of such a company, you should want gunslingers as managers, not careful conservative Ben Kovler look-alikes.

- Why? Your stock has a negative liquidation value, and it can’t get much worse. So, damm the torpedoes, swing for the fences; you have nothing to lose. If you get lucky, you might come from behind, and if not, the debtholders will take most of the hit.

- Of course, debtholders don’t see things quite that way. You are, after all, essentially rolling the dice with their money. This is one reason why debtholders want receivers in control: to prevent management from doing the absolutely rational thing – going all in.

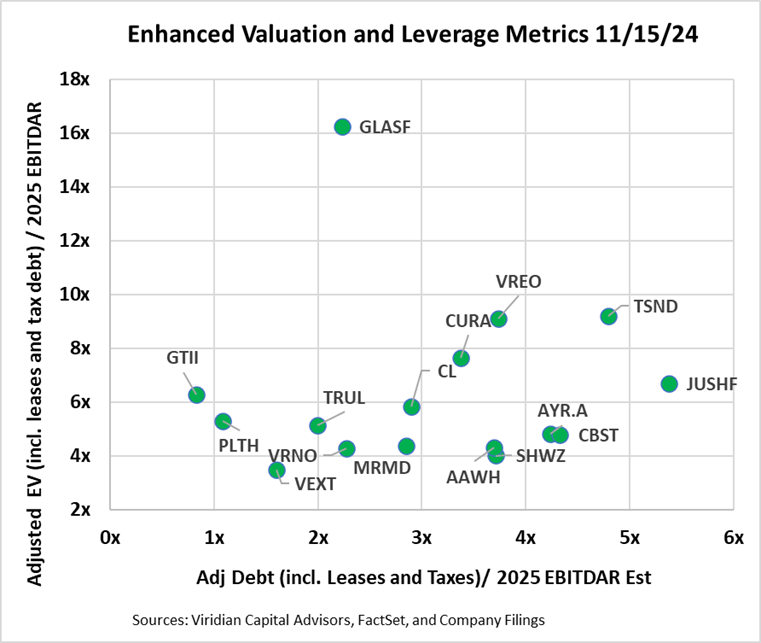

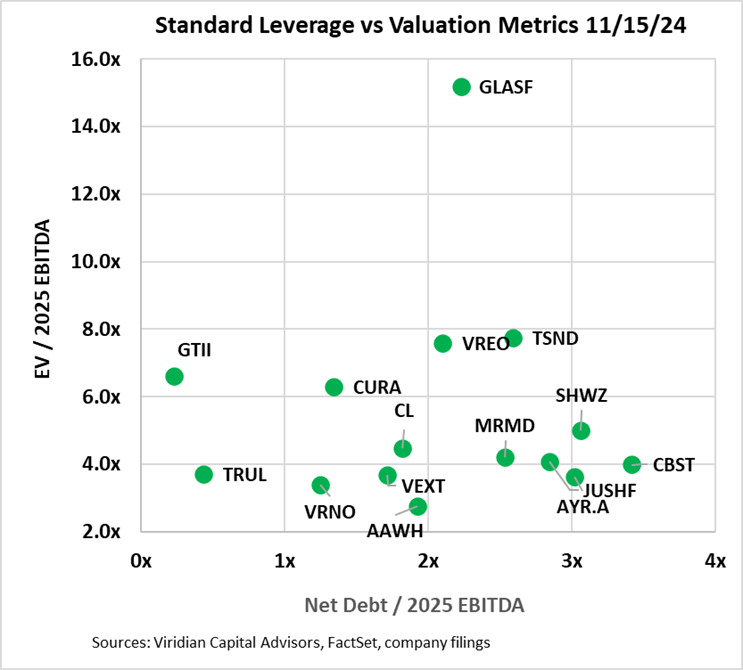

- MSO FINANCIAL FLEXIBILITY DEPICTED BY FOUR GRAPHS FEATURING OUR NEWEST VALUATION AND LEVERAGE METRICS

- The three graphs below seek to map the financial options available to eighteen of the largest MSOs based on their Valuation, Leverage, and Liquidity. We have updated our measures to look at 2025 EBITDAR estimates as we believe most investors are now looking to these values in their valuations.

- The first two graphs present different versions of EV/EBITDA on the vertical axis and Debt/EBITDA on the horizontal axis.

- The first graph presents our latest view of the most appropriate valuation and financial statement-based leverage metrics: Adjusted E.V. / 2025 EBITDAR and Adjusted net debt / 2025 EBITDAR. In calculating Adjusted Net Debt, we make several key assumptions: 1) Leases that are included on the balance sheet are considered debt. We view most leases in the cannabis space as equivalents to equipment loans or mortgage loans. While it is true that a lease default does not necessarily trigger a cascade of events leading to bankruptcy, the distinction is often meaningless in cannabis due to the mission-critical nature of many long-term leases and the absence of bankruptcy protection in cannabis. 2) We consider any accrued taxes (including uncertain tax liability accounts listed as long-term liabilities) in excess of the most recent quarterly tax expense to be debt. Our calculation of enterprise value is now market cap plus debt plus leases plus tax debt minus cash. We now use EBITDAR rather than EBITDA since lease expense is taken out prior to EBITDA.

- The second graph utilizes EBITDA and employs the traditional calculations of both debt and enterprise values, leaving out leases and taxes.

- Our adoption of new metrics tends to make the companies look less cheap and more leveraged.

- Surprisingly, eight of the companies on the enhanced metric chart are still above 3x leverage, which we have identified as the boundary of sustainability in a 280e environment. Four companies now exceed 4x leverage, which we believe will be close to the maximum sustainable post 280e.

- Valuation metrics can be deceiving when a company is just achieving positive cash flow status. Glass House, for example, has enormous valuation multiples. Still, it is based on small EBITDAs that are likely to expand significantly in the next several years.

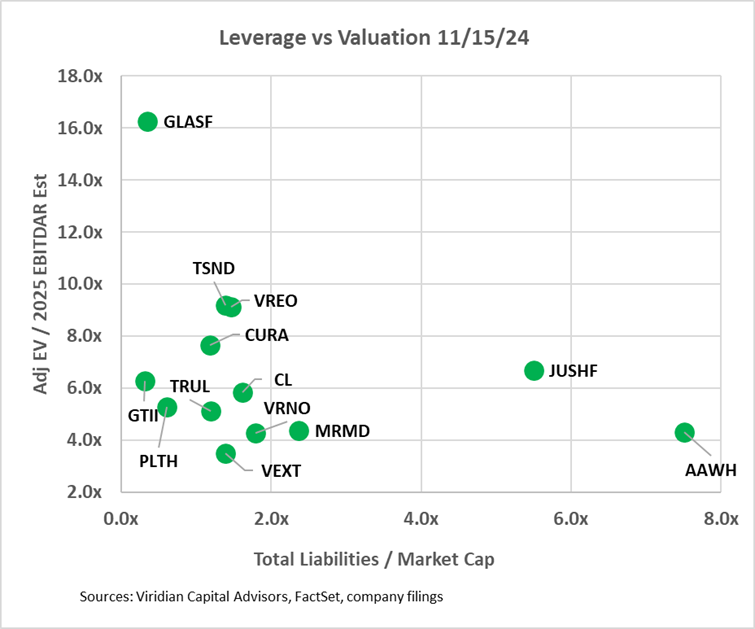

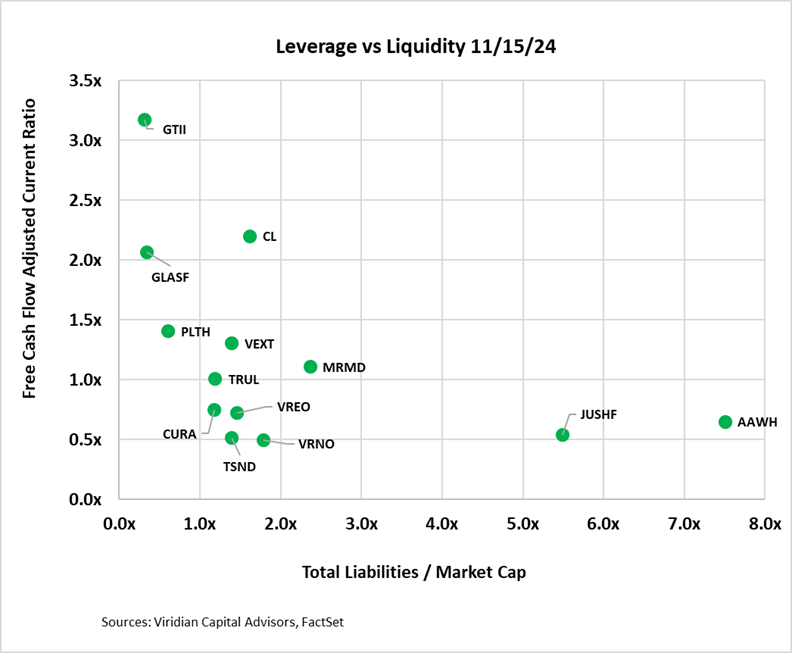

- The third graph looks at leverage through the lens of total liabilities to market cap. We believe this is the single best measure of leverage because it is a direct reflection of the market’s assessment of the value of a company’s assets in excess of its liabilities and is sensitive to changes in market perception of a company’s future.

- On the bottom left are companies with Adj E.V./2025 EBITDAR of under 7x and total liabilities to market cap under 2x. The group includes Vext, GTI, PLTH, Verano, and Cresco. Companies in this quadrant are right to consider stock repurchases or using cash in acquisitions. They can afford some additional debt and can take advantage of the ongoing dislocation in equity prices.

- In the middle, between 2x and 5x total liabilities/market cap, we see Ascend, AYR, Jushi, and MariMed. Each of these has significant upside catalysts that could mitigate or exacerbate the excess leverage. However, several upside catalysts seem to be neutralized in the short run. Florida rec is indefinitely delayed, PA rec does not seem to be happening this year, and VA rec is probably on hold until 2026.

- On the right lies Jushi, AYR, Ascend, and Schwazze (not pictured). AYR has moved into our danger zone, but its metrics are not nearly as troublesome as the Schwazze. At the top left are companies with high valuation metrics and low leverage. These companies should look to do an equity issuance depending on their positioning in the liquidity graph below.

- The fourth graph introduces the free cash flow adjusted current ratio liquidity measure into the mix. Companies with less than 1x on this measure will likely have to raise capital next year. Surprisingly, eight of the companies fall into this bucket (including Schwazze, not pictured).

- The bottom left group, including Curaleaf, Verano, and Vireo, has low leverage but is below the critical 1x liquidity level. This suggests that Curaleaf and Verano should take advantage of the robust debt market to augment their liquidity (note that Curaleaf just did this). Vireo is a more challenging call. Their adjusted net debt/ EBITDAR is relatively high, which makes them an unlikely net debt issuer and suggests asset sales.

- On the top left, we find companies with adequate liquidity and low market leverage, including both GTI and TerrAscend, due to their recent refinancings.

- Companies in the lower middle-to-right generally have constrained liquidity and high leverage, a potentially dangerous combination in a capital-constrained environment. Cannabist’s liquidity is understated in the graph and is likely to be OK based on announced asset sales. 4Front and Schwazze, despite making moves to restructure their debt, continue to have inadequate liquidity and excess leverage and should be watched carefully. We note that FFNT has no consensus on 2025 EBITDA estimates, but a full year of Illinois cultivation will probably make leverage look significantly better.

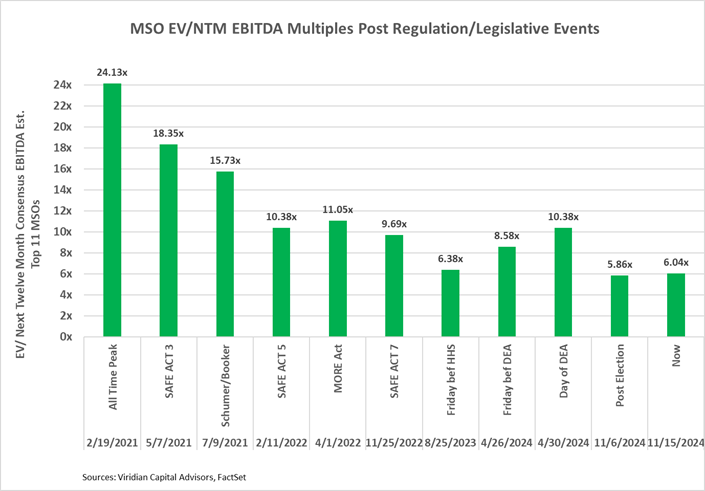

- EV/LTM MULTIPLES ARE NOW LOWER THAN BEFORE THE ORIGINAL HHS RESCHEDULING ANNOUNCEMENT ON 8/30/23

- We continue to believe that at current levels, U.S. MSOs have enormous upside potential. The graph below shows the multiples reached after a number of past legislative/regulatory events. It makes clear that a doubling of prices is a reasonable assumption. We recommend a balanced portfolio that leans toward the companies in the top half of the Viridian Credit Tracker model ranking.

- Despite the challenges to growth discussed above, we believe that many companies have become stupidly cheap. We recommend a “don’t step in the doggy do do” strategy. With refinancing risks made worse by cratering stock prices, this is no time to be a hero. Focus on building a diversified portfolio of companies ranked in the top 10 in our credit rankings. Put them in your portfolio and follow the total liabilities to market cap indicator that we recommended several weeks ago, as well as the credit tracker rankings. And resist the urge to look at the stock prices every day!

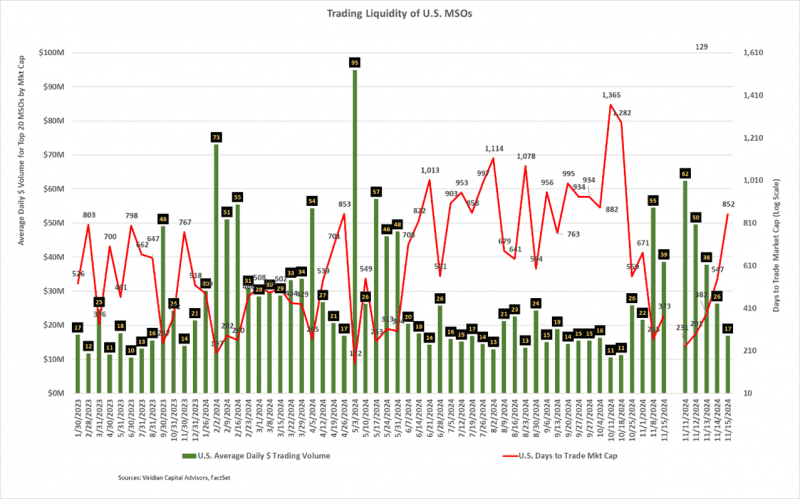

- TRADING LIQUIDITY REMAINS BRISK AMIDST UNRESOLVED UNCERTAINTIES

- The average daily dollar volume of $39M for the week ending 11/15/24 was well above the YTD average of $29M but considerably off record pace.

- The Days to Trade Market Cap (DTTMC) series depicts the number of days it would take to trade the market cap of a stock or group of stocks. The current DTTMC of 373, up from the election week spike of 265, implies that an investor who acquired a 5% position in the stock, assuming he wanted to be less than 25% of the average daily dollar volume, would require 75 days to trade out of his position.

- We expect volumes to recede as the holidays approach and the significant news items become more scarce.

- GIVING CREDIT WHERE CREDIT IS DUE

- The chart below shows our updated 11/15/24 credit rankings for the 31 U.S. cannabis companies with over $3M market cap. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement.

- We have made recent upgrades to our credit model to more accurately treat lease liabilities and account for non-payment of taxes as a financing source.

- The blue squares show the offered-side trading yields for each Company. Trading yields have declined significantly since the HHS rescheduling announcement. We are expecting the round of recent refinancings to re-rate the landscape of cannabis debt. Note: The prices shown were obtained prior to the election, as well as some of the recent earnings releases. We consider them to be only indicative, as we expect updated pricing to reflect the dislocations observed in the equity market.

- There have been significant ranking changes since last week, spurred by new earnings releases, the Florida debacle, and the election, as well as what we discuss elsewhere as a “growth panic.”

- Glass House was one of the biggest gainers, picking up two more ranking slots based mainly on the fact that its stock has suffered far less than the MSOs. Verano gained back one notch but is continuing to hold a significantly worse position than its pre-election ranking.

- AYR’s yield doesn’t look nearly as cheap as it did pre-Florida. We expected the revenue gains for the company in Florida to fuel solid cash flow gains since much of the spending for cultivation improvements has already occurred. There are no near-term debt triggers because the company’s maturities have substantially been pushed out to December 2026. However, the approximately $300 million of 2026 maturities now represent 3.6x the company’s market cap, compared to 1.1x on 11/1/24. The 3.6x exceeds the level of maturities AYR faced at the end of 2024 before it conducted a somewhat disastrous restructuring/refinancing deal. We see asset sales as a possibility to close that gap, and the company’s new Virginia license jumps up as a prime possibility. Verano just paid $90M for a combination of Cannabist cultivation and retail facilities, which evidently require some refurbishment. So, what would a license in VA bring?

- Curaleaf debt is overvalued. Investors can pick up stronger credit and extra yield from Cresco.

![]()

- Cannabis equities (as measured by the MSOS ETF) ended down 3.48% for the week, which is not much consolation after last week’s largest decline in the ETF’s history (since September 2020). The market was encouraged by the Matt Gaetz nomination for attorney general.

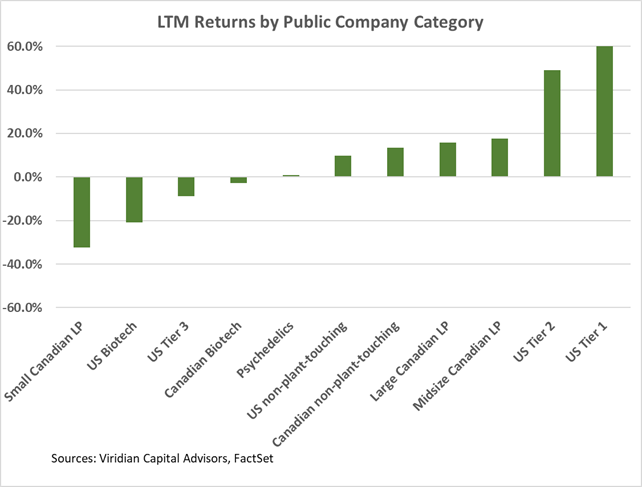

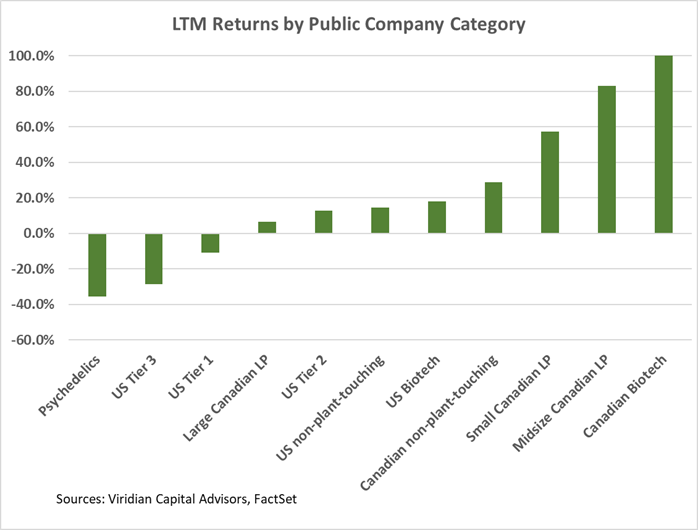

Trailing 52-Week Returns by Public Company Category:

-

- Tier one operators, especially those that have significant exposure to Florida, gained sharply in this week’s LTM rankings relative to last week’s.

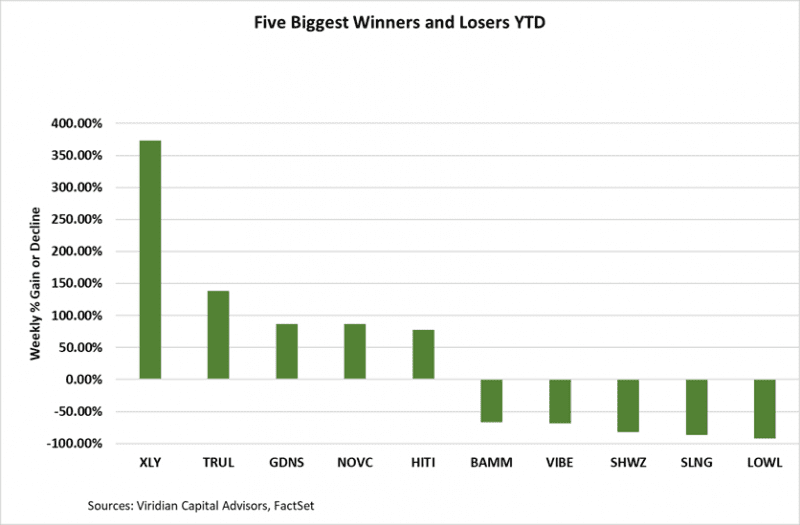

Best and Worst Performers for the week:

- Five of the biggest losers of the week, AYR, Curaleave, Trulieve, Verano, and Cansortium, have above-average exposure to Florida.

- Winners of the week had modest gains.