OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

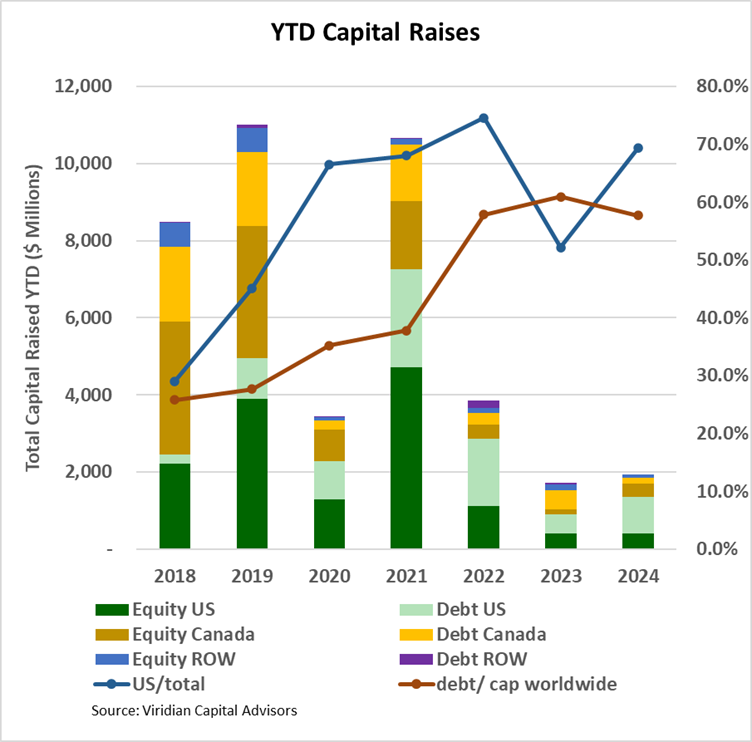

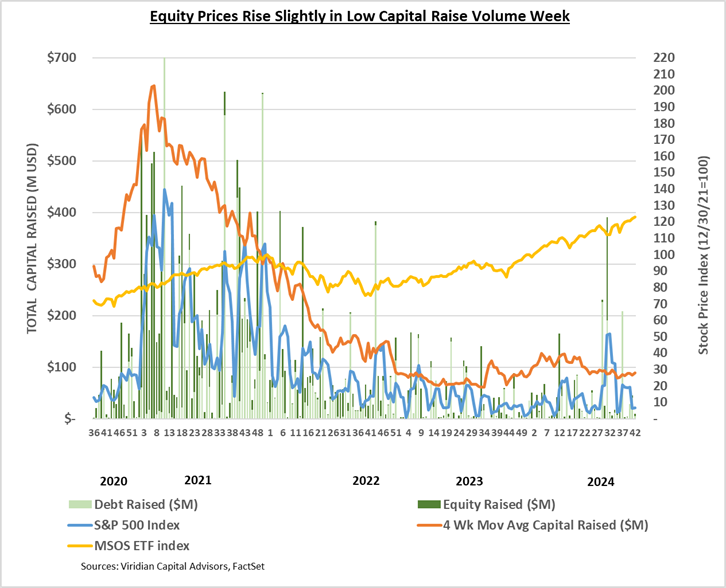

- YTD capital raises totaled $1,970.35M, up 13.7% from the same period in 2023. Debt as a percentage of capital raised dropped to 57.6% from 61.0% in the previous year on a worldwide basis. The U.S. bucked this trend with 70.1% of capital raised in debt compared to 54.8% in 2023.

- U.S. raises accounted for 69.3% of total funds, up from 52.1% at the same point in 2023. Raises from outside Canada and the U.S. represented 5.2% of the total funds raised, which is in line with the average of 5.8% for the six previous years but is sharply lower than the 11.3% achieved in 2023.

- YTD raises by public companies accounted for 75.2% of total funds, the highest since 2021.

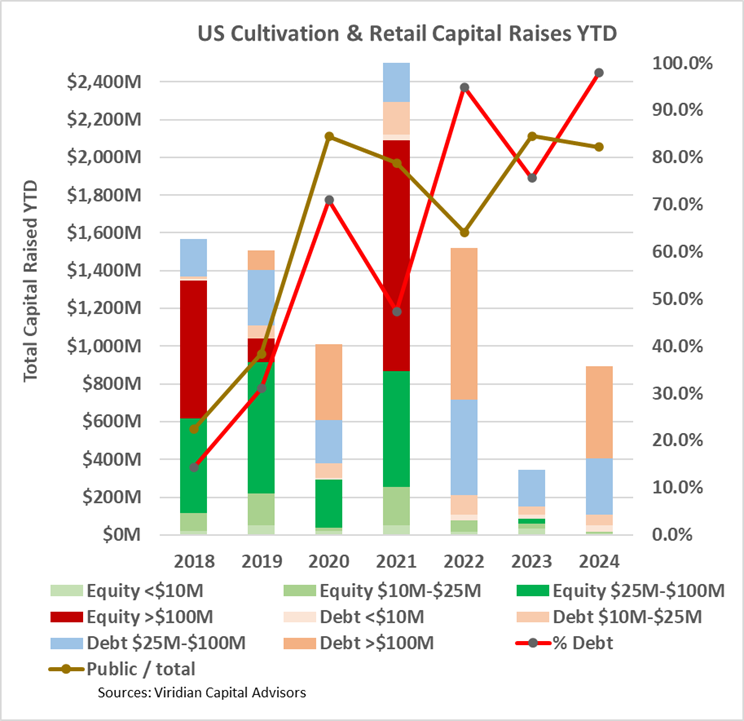

- Cultivation and Retail Sector capital raises are up 159% YTD. Debt accounts for 98% of the $890M raised is earmarked for refinancing of existing debt. Large debt issues (>$100M) bounced back and represented 54.6% of capital raised compared to zero in 2023.

VIRIDIAN INSIGHTS

- GREEN THUMB TAKES POSITION IN NASDAQ LISTED AG TECH COMPANY AGRIFY (AGFY: Nasdaq)

- On November 5, 2024, Agrify announced Green Thumb Industries had acquired an equity stake in the company through a purchase of common stock and warrants and was further investing up to $20M in a convertible secured note, $10M of which will be drawn at closing.

- AGFY was up around 40% as of 4 pm on Tuesday, as speculation swirled about the intent of GTI.

- As of Monday, November 4, AGFY had a market cap of $4.2M and an enterprise value of $9.95M. GTI’s initial investment provides much-needed liquidity to AGFY, which only had $57K of cash as of its June balance sheet against $5.6M of debt. AGFY has had negative EBITDA for 15 consecutive quarters and, despite some improvement in recent quarters, continues to burn cash.

- The company is too small for GTI to care about. It’s still negative cash flow and dependent on growth in cultivation. None of this makes the deal look like a straightforward investment deal.

- In addition, AGFY’s Chairman and Founder Raymond Chang resigned, and the board appointed Ben Kovler from GTI as chairman.

- It doesn’t take much imagination to see that AGFY’s Nasdaq listing is its most prized asset. Kovler made an end-run attempt at uplisting through his overture to Boston Beer, and it seems clear that this transaction is essentially the purchase of a Nasdaq-listed shell company. Does he have some kind of Canopy-USA-esq structure in mind? We don’t know, but we don’t think S3 gets him to uplisting, assuming it goes through as planned.

- Still, as an entry point, this seems like a pretty good bet. We think the ag tech sector is primed for a rebound, but the pain is still not quite past.

- A SHOCKING RESULT: EARLY POLLING RESULTS APPEAR TO INDICATE THAT FLORIDA REC WILL FAIL TO REACH THE 60% REQUIRED THRESHOLD.

- Florida-centric stocks like AYR and Trulieve were already down sharply at the close of the market and will presumably suffer more tomorrow. The MSOS was reportedly down 10% in after hours trading.

- The failure likely cost the cannabis companies around an incremental $2-3B run rate of revenues. At 30%ish EBITDA margins, this is a $1B EBITDA hit and at 5x somewhere around a $5B potential market cap hit.

- The pressure now falls squarely on S3 to provide a catalyst for incremental investment and capital markets revival.

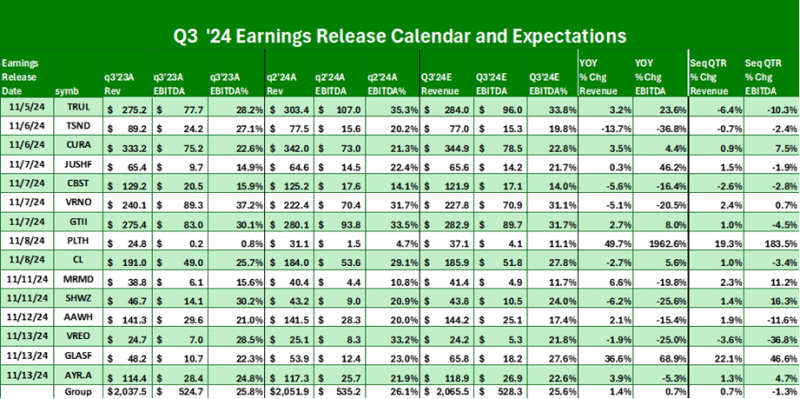

- ANALYSTS’S Q3 ESTIMATES DO NOT PAINT AN ENTHUSIASTIC PICTURE

- The fifteen companies in the table below are arranged in order of earnings release. The table shows actual q3’23 and q2’24 results as well as estimates for q3’24. Overall expectations are for a 1.3% sequential quarter decline in EBITDA (taking into account actual results for Trulieve). Our Chart of the Week decomposes this change into its revenue change and EBITDA margin change components. This analysis shows that margin changes are the driving force behind the differences from q2.

- Trulieve, the first company out of the blocks, missed revenue by .8% but exceeded analyst EBITDA estimates by 10.0%. Despite that beat, the stock was down based on reports of strong Republican voter turnout, which no one really seems to know how to interpret vis a vis Florida Rec. (are they Trump Republicans or DeSantis Republicans?

- CANOPY GROWTH PAYS OFF $100M DEBT WHILE SINGING “DON’T STOP BELIEVING”

- On October 17, 2024, Canopy Growth announced that it had paid off $100M of its Senior Secured Term Loan for $97.5M.

- The company stated that the repayment of the debt would result in annualized interest savings of approximately $14M, implying a 14% rate on the debt.

- The early debt retirement allowed the maturity of the debt to be extended from 3/18/26 to 12/18/26. The maturity of the remaining debt can be further extended to September 18, 2027, if the company makes another $100M payment by March 2025.

- Did the company make the right decision to pay off this debt? The answer is not obvious and demands balancing two opposing needs: Liquidity vs Leverage.

- On the leverage front, using cash to repay debt does not change net debt, and therefore, Net Debt/EBITDA is unchanged. On the other hand, our favorite leverage indicator, total liabilities/market cap, goes down. Market cap is unaffected, but total liabilities go down, and that has to be considered a positive.

- Conversely, using cash to pay off a debt that does not mature for seventeen months represents an unambiguous reduction in liquidity.

- To analyze the net impact of the transaction, we used the Viridian Credit tracker model. We expected that the positive effect on leverage would outweigh the negative impact on liquidity. However, we were surprised to find that was not the result.

- Our leverage rankings rely on four metrics: Total Liab/Mkt cap went from .97 before the payment to .79 after the payment, clearly an improvement, but in terms of relative ranking, only a one-notch improvement from #14 to #13. EBITDAR/ Adj net debt was unchanged. Funds from operation to liabilities improved slightly, but FFO is still negative, and the relative ranking did not change. The bottom line is that our leverage ranking for Canopy did not change.

- Our liquidity ranking, however, took a big hit, deteriorating from #10/23 to #19/23.

- There is also a less quantitative impact that is important here: By using cash to pay off debt early, Canopy can signal that it doesn’t think it will have any problem funding operations. The psychology is important. If the equity market believes this, as this week’s share price gains seem to indicate, the company will continue to be able to sell equity to maintain liquidity even as operations remain cash-negative.

- On the whole, we question the logic of spending so much cash and reducing near-term liquidity in order to achieve a marginal debt extension more than a year from now. If Canopy was cash flow positive, we might have a different view.

- CHICAGO ATLANTIC’S $50M DEBT DEAL AT 9% IS A STUDY IN CONTRASTS

- On the one hand, a peek at the debt positions in the company’s recent registration statement makes clear that we would do this trade all day long! Borrow at 9% and lend at 16-19%; What’s not to love about that?

- The contrast comes in when we consider the BBB+ rating from Egan Jones that Chicago Atlantic got for the debt. The ICE BofA BBB Corporate Index of Effective Yield is now at 5.29%. This implies a spread of nearly 500bps over similarly rated non-cannabis-related corporations. Witness also the recent Green Thumb transaction at 500 over SOFR, which swaps to a 9.06% fixed rate. So, is an unsecured bond implicitly backed by a portfolio of cannabis credits priced right on top of the debt of the best cannabis credit?

- One thing we speculate: Investors buying the Chicago Atlantic Debt would love to be able to directly lend to the space or purchase cannabis debt in the market, but they cannot, chiefly for reputational, listing, or custody reasons. So they are, in essence, lending to cannabis one step removed, giving up a lot of the direct lending yield while still achieving a highly attractive credit spread. Let’s split the difference, and all go home happy! Cheers!

- CANSORTIUM AND RIV RISK ARB SPREAD SEEMS TOO WIDE

- On October 10, 2024, RIV Capital and Cansortium received New York State Cannabis Control Board approval for a change of control.

- The only other significant transaction which must be completed prior to closing is the Smith Transaction.

- The risk/arb spread is down to 40%, but that still seems quite wide, given the stated intent to close the transaction before year-end.

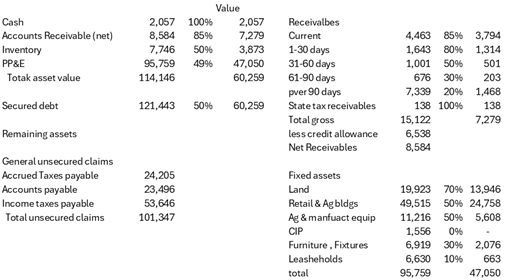

- IS IT POSSIBLE THAT STATEHOUSE SECURED DEBT IS ONLY WORTH 50% OF FACE VALUE?

- The Receivership and bankruptcy proceedings seem likely to signal the breakup and sale of the company to satisfy creditors. The very rough liquidation analysis below comes up with around 50% recovery on secured debt. We hope we are wrong, but this analysis does indicate why cannabis lenders seem to be willing to lend good money after bad: When the music stops, it gets pretty ugly.

- We have assumed no net value for net assets held for sale, prepaids, or notes receivable. We have also been draconian in evaluating receivables over 90 days past due as worth only 20%.

-

- Note that we have not made any adjustments for the time value of money, which would further reduce valuations. As far as we can tell, these assets are not yet on the block. It is brutally challenging to break out of the “extend and pretend” mindset.

- We anticipate that the eventual sale of the StateHouse assets will put further pressure on asset values in California.

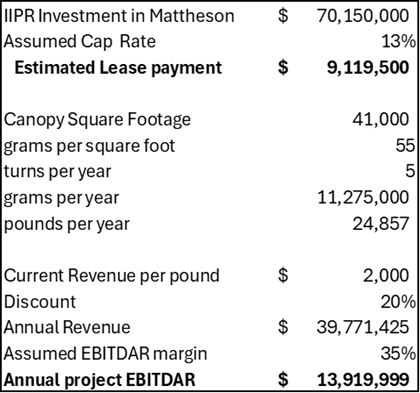

- DOES 4FRONT NEED MORE THAN A BRIDGE?

- The prevailing assumption in the market has been that if they can just get their monster grow facility in Illinois fully up and running, the rest will work out.

- But what if the base rent is relatively high? Just how much additional cash flow is the facility likely to produce?

- The Viridian estimates below indicate that the facility will likely produce around an incremental $5M cash flow to the company after paying lease expenses. It’s profitable but not fortune-changing. Bottom line? Canaccord will still be earning their fees.

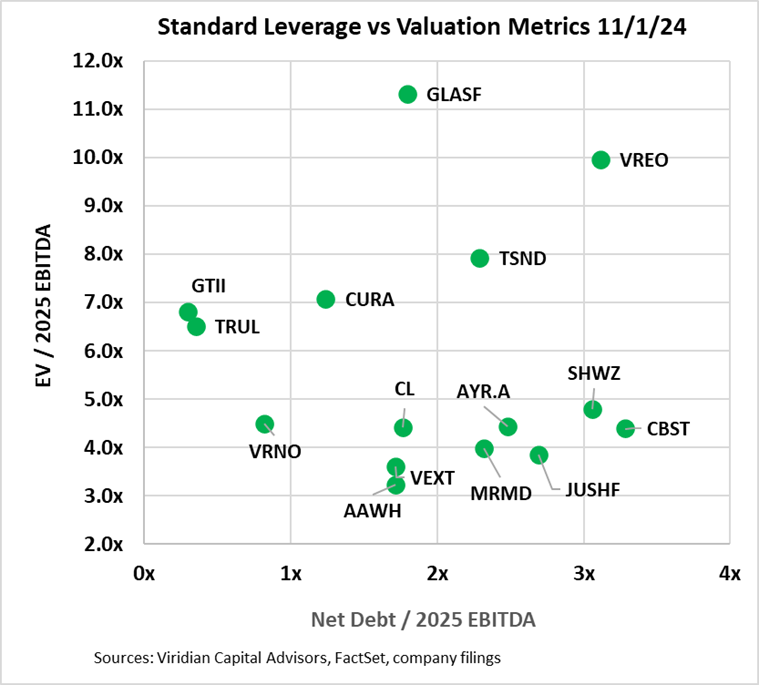

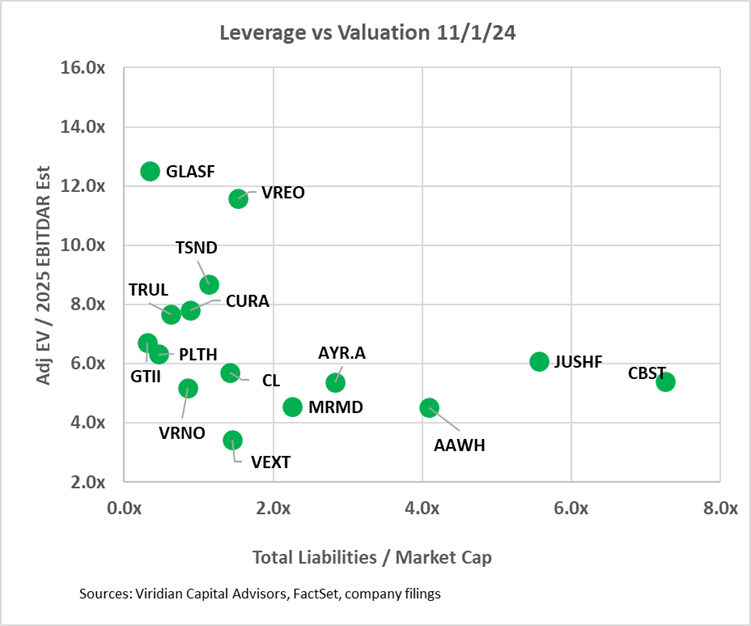

- MSO FINANCIAL FLEXIBILITY DEPICTED BY FOUR GRAPHS FEATURING OUR NEWEST VALUATION AND LE

- MSO FINANCIAL FLEXIBILITY DEPICTED BY FOUR GRAPHS FEATURING OUR NEWEST VALUATION AND LEVERAGE METRICS

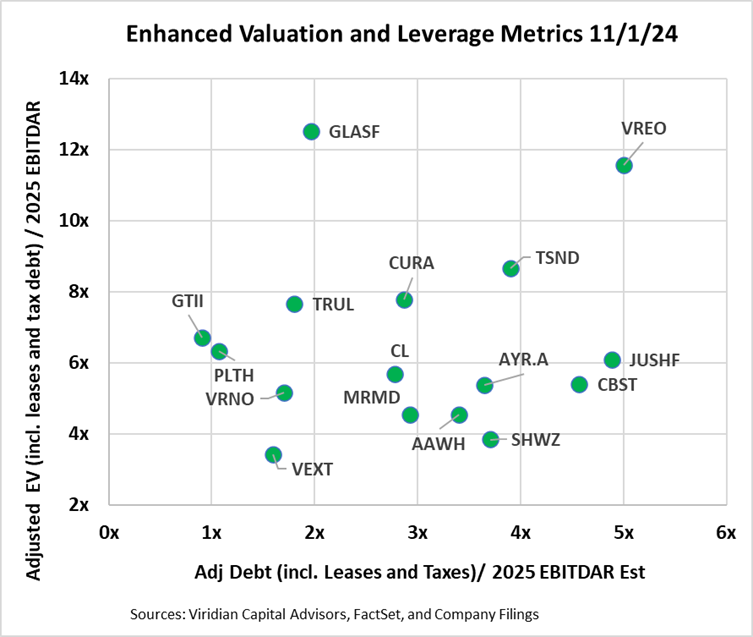

- The three graphs below seek to map the financial options available to eighteen of the largest MSOs based on their Valuation, Leverage, and Liquidity. We have updated our measures to look at 2025 EBITDAR estimates as we believe most investors are now looking to these values in their valuations.

- The first two graphs present different versions of EV/EBITDA on the vertical axis and Debt/EBITDA on the horizontal axis.

- The first graph presents our latest view of the most appropriate valuation and financial statement-based leverage metrics: Adjusted E.V. / 2025 EBITDAR and Adjusted net debt / 2025 EBITDAR. In calculating Adjusted Net Debt, we make several key assumptions: 1) Leases that are included on the balance sheet are considered debt. We view most leases in the cannabis space as equivalents to equipment loans or mortgage loans. While it is true that a lease default does not necessarily trigger a cascade of events leading to bankruptcy, the distinction is often meaningless in cannabis due to the mission-critical nature of many long-term leases and the absence of bankruptcy protection in cannabis. 2) We consider any accrued taxes (including uncertain tax liability accounts listed as long-term liabilities) in excess of the most recent quarterly tax expense to be debt. Our calculation of enterprise value is now market cap plus debt plus leases plus tax debt minus cash. We now use EBITDAR rather than EBITDA since lease expense is taken out prior to EBITDA.

- The second graph utilizes EBITDA and employs the traditional calculations of both debt and enterprise values, leaving out leases and taxes.

- Our adoption of new metrics tends to make the companies look less cheap and more leveraged.

- Surprisingly, eight of the companies on the enhanced metric chart are still above 3x leverage, which we have identified as the boundary of sustainability in a 280e environment. Three companies now exceed 4x leverage, which we believe will be close to the maximum sustainable post 280e.

- Valuation metrics can be deceiving when a company is just achieving positive cash flow status. Glass House, for example, has enormous valuation multiples. Still, it is based on small EBITDAs that are likely to expand significantly in the next several years.

- The third graph looks at leverage through the lens of total liabilities to market cap. We believe this is the single best measure of leverage because it is a direct reflection of the market’s assessment of the value of a company’s assets in excess of its liabilities and is sensitive to changes in market perception of a company’s future.

- On the bottom left are companies with Adj E.V./2025 EBITDAR of under 7x and total liabilities to market cap under 2x. The group includes Vext, GTI, PLTH, Verano, and Cresco. Companies in this quadrant are right to consider stock repurchases or using cash in acquisitions. They can afford some additional debt and can take advantage of the ongoing dislocation in equity prices.

- In the middle, between 2x and 5x total liabilities/market cap, we see Ascend, AYR, Jushi, and MariMed. Each of these has significant upside catalysts that could mitigate or exacerbate the excess leverage. For example, Jushi is levered to potential adult rec developments in Pennsylvania and Virginia, and AYR has significant Florida torque.

- On the right lies Cannabist and Schwazze (not pictured). We applaud Cannabist management. They have seen the writing on the wall: too levered to issue equity or debt, its only option was asset sales. We have not yet modeled the announced asset sales into Cannabist’s credit picture as we are not sure how much EBITDA will be lost in the transactions. We will await adjusted equity analyst estimates. Note that Schwazze now has total liabilities to market cap in excess of 28x, a level that generally indicates deep distress. The uncertainty is heightened by the company’s failure to file 2nd quarter financial statements and the potential for significant revisions to prior statements.

- At the top left are companies with high valuation metrics and low leverage. These companies should look to do an equity issuance depending on their positioning in the liquidity graph below.

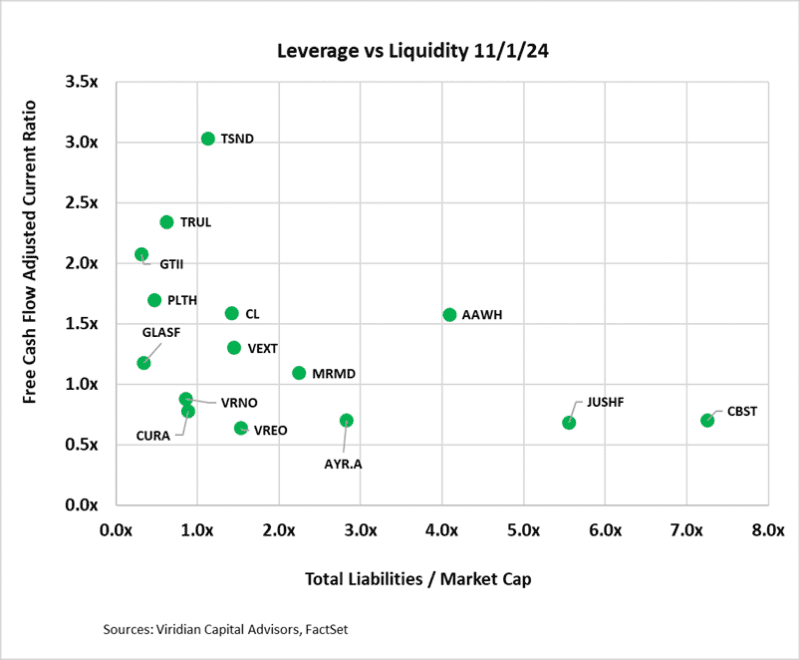

- The fourth graph introduces the free cash flow adjusted current ratio liquidity measure into the mix. Companies with less than 1x on this measure will likely have to raise capital next year. Surprisingly, eight of the companies fall into this bucket (including Schwazze, not pictured).

- The bottom left group, including Curaleaf, Verano, and Vireo, has low leverage but is below the critical 1x liquidity level. This suggests that Curaleaf and Verano should take advantage of the robust debt market to augment their liquidity. Vireo is a more challenging call. Their adjusted net debt/ EBITDAR is relatively high, which makes them an unlikely net debt issuer and suggests asset sales.

- On the top left, we find companies with adequate liquidity and low market leverage, including both GTI and TerrAscend, due to their recent refinancings.

- Companies in the lower middle-to-right generally have constrained liquidity and high leverage, a potentially dangerous combination in a capital-constrained environment. AYR has significant optionality based on the Florida vote. If things go the company’s way, they will probably have significantly lower market leverage, allowing for more financial flexibility. Cannabist’s liquidity is understated in the graph and is likely to be OK based on announced asset sales. 4Front and Schwazze, despite making moves to restructure their debt, continue to have inadequate liquidity and excess leverage and should be watched carefully. We note that FFNT has no consensus on 2025 EBITDA estimates, but a full year of Illinois cultivation will probably make leverage look significantly better.

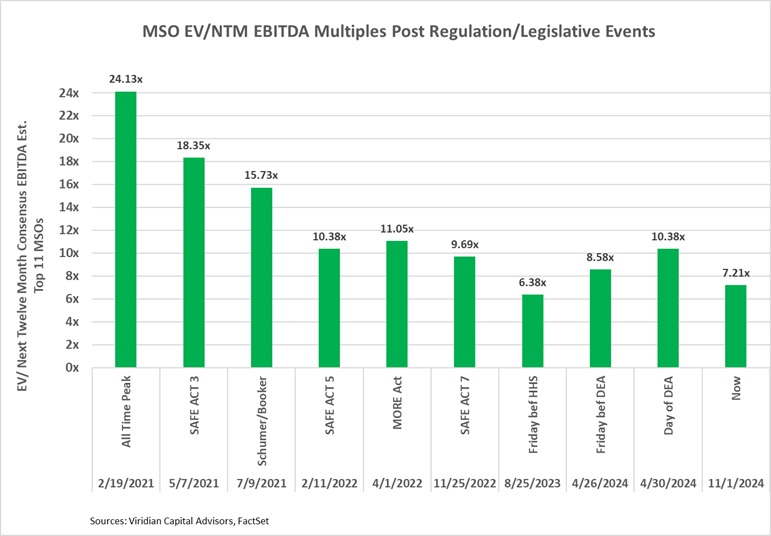

- A DOUBLING STILL POSSIBLE FOR INVESTORS PATIENT ENOUGH TO WAIT FOR THE NECESSARY CATALYSTS. STILL THE TIMELINE KEEPS EXTENDING

- We continue to believe that at current levels, U.S. MSOs have enormous upside potential. The graph below shows the multiples reached after a number of past legislative/regulatory events. It makes clear that a doubling of prices is a reasonable assumption. We recommend a balanced portfolio that leans toward the companies in the top half of the Viridian Credit Tracker model ranking.

- Notably, the discussion of SAFER has begun again. We hesitate to put much stock in such debate in an election year. Still, the ongoing talks do point to another critical catalyst, one that many institutional investors believe is more important than S3.

-

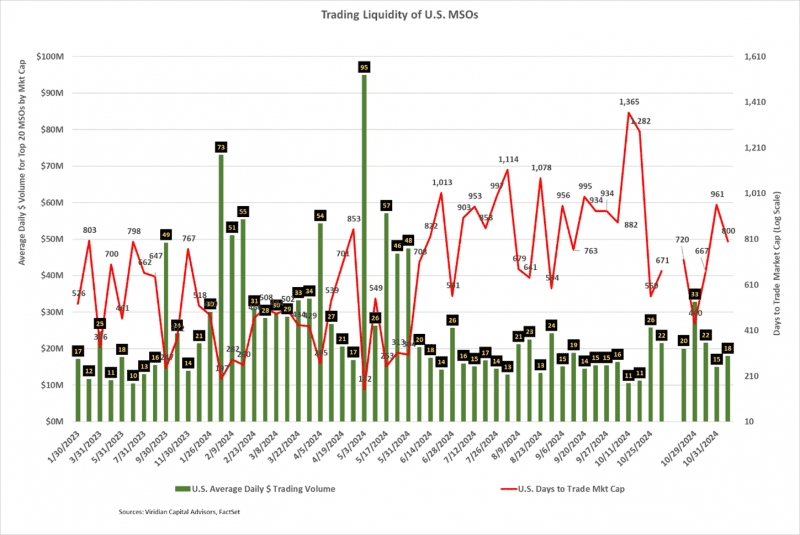

- TRADING VOLUME REMAINS ELEVATED ON NEWS OF DEA HEARING DELAY

- The average daily dollar volume of $22M for the week ending 11/1/24 was well above the $17M trailing 12-week average but down $4M from last week’s figure.

- The Days to Trade Market Cap (DTTMC) series depicts the number of days it would take to trade the market cap of a stock or group of stocks. The current DTTMC of 671, up from 559 last week, implies that an investor who acquired a 5% position in the stock, assuming he wanted to be less than 25% of the average daily dollar volume, would require 134 days to trade out of his position.

- As the presidential election cycle accelerates, we expect more trading volume and price volatility.

- TRADING VOLUME REMAINS ELEVATED ON NEWS OF DEA HEARING DELAY

-

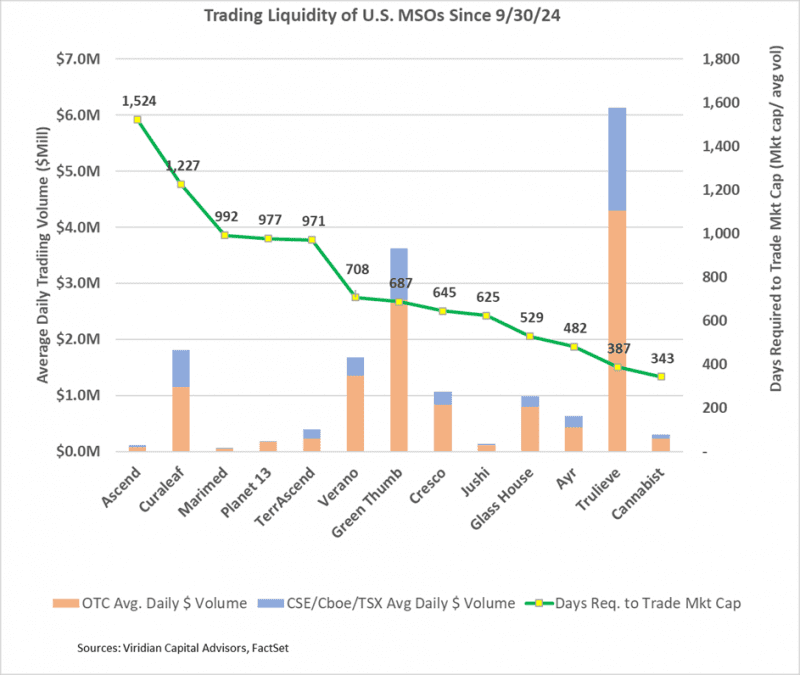

- The graph below shows the liquidity of 14 prominent MSOs/SSOs. The stacked bars show the total average daily dollar volume broken into the two exchanges that the companies trade on. The green line shows the Days to Trade Market Cap (DTTMC) using the average daily dollar volume since 9/30/24. AYR and Trulieve, two companies with high Florida torques, were among the most liquid stocks this week.

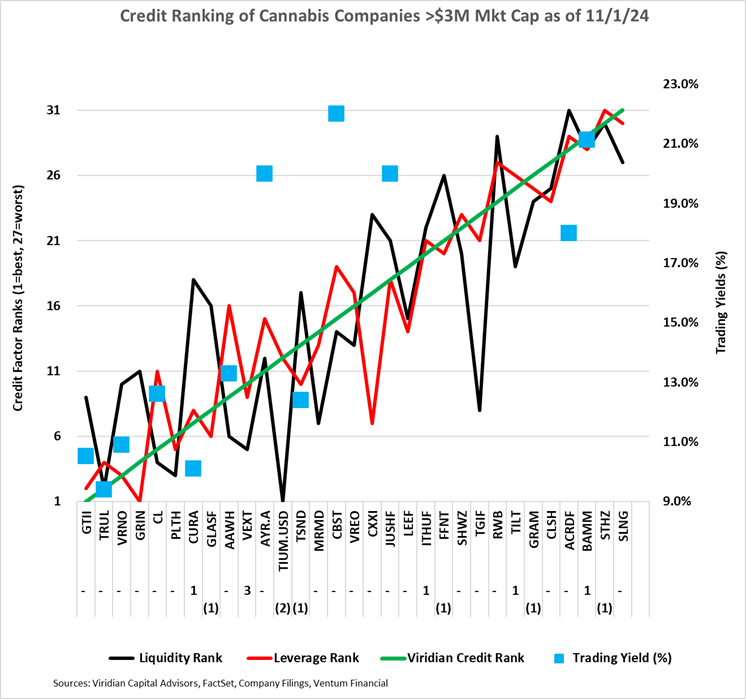

- GIVING CREDIT WHERE CREDIT IS DUE

- The chart below shows our updated 11/1/24 credit rankings for the 31 U.S. cannabis companies with over $3M market cap. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement.

- We have made recent upgrades to our credit model to more accurately treat lease liabilities and account for non-payment of taxes as a financing source.

- The blue squares show the offered-side trading yields for each Company. Trading yields have declined significantly since the HHS rescheduling announcement. We are expecting the round of recent refinancings to re-rate the landscape of cannabis debt. Note: The prices shown are now two weeks old and should only be considered indicative.

- AYR is still significantly undervalued, having recently obtained a Virginia license and having one of the highest Florida torques. The risk is that the company has one of the more difficult refinancing tasks coming up in 2026. The company’s projected fixed charge coverage is under 2x for 2026, absent any uptick from Florida.

- Curaleaf debt is overvalued. The company ranks between Cresco and Ascend, and investors can pick up stronger credit and extra yield from either Cresco or Verano.

- Body & Mind (BAMM: CSE) improved one notch as it received a much-needed bridge to asset sale proceeds.

- We are showing Acreage debt at its issue yield but are unaware of any market for this debt. At 18%, we would advise selling and moving into AYR or Cannabist. All have significant risks, but we view the risk/reward as better than the other names. For example, this week’s Body and Mind issue, priced to yield 21.14%, represents a better risk/reward trade-off in our view.

- Cannabis equities (as measured by the MSOS ETF) ended down 9.22% for the week.

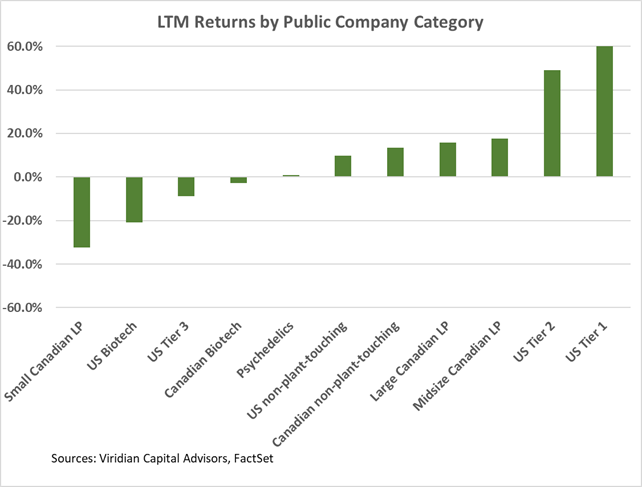

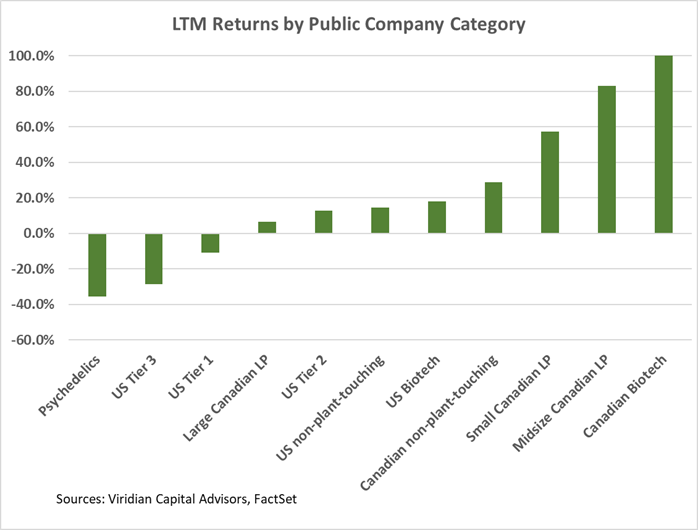

Trailing 52-Week Returns by Public Company Category:

-

- Tier one operators, especially those that have significant exposure to Florida, gained sharply in this week’s LTM rankings relative to last week’s.

Best and Worst Performers for the week:

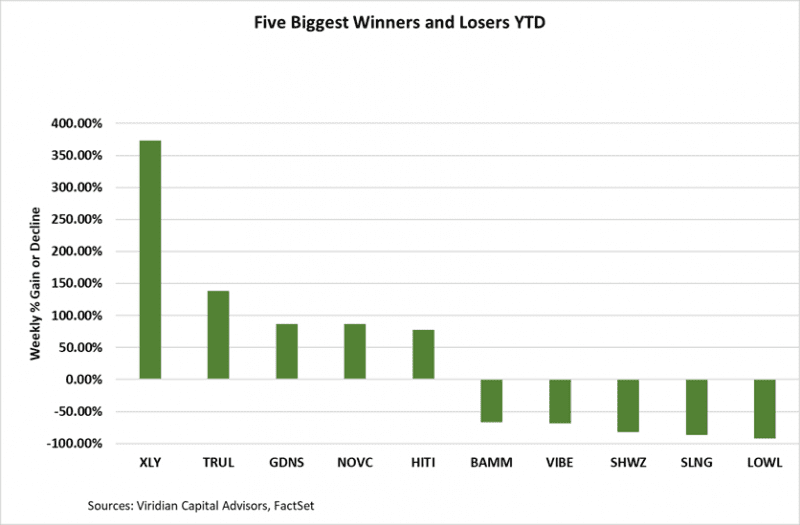

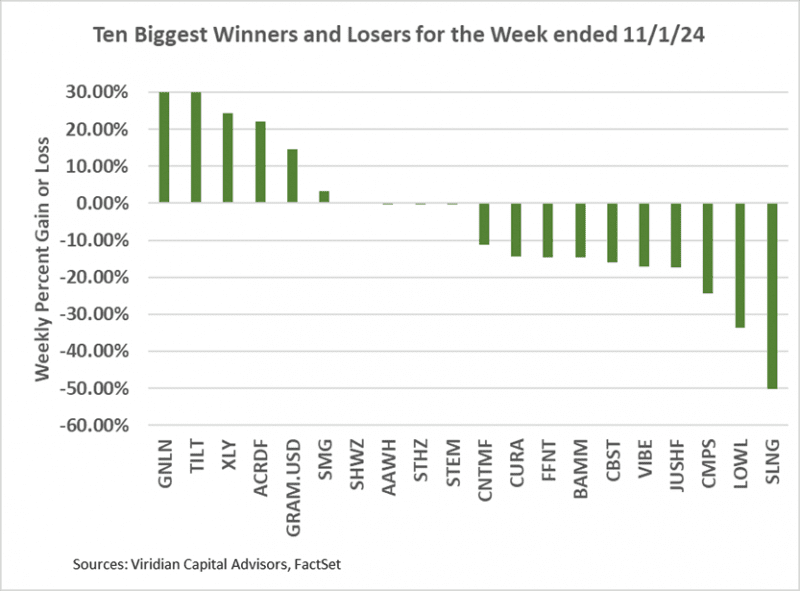

- Greenlane (GNLN: Nasdaq) and Auxly (XLY: CSE) are among the top ten gainers after heading the losers list last week.

- Similarly, Lowell (LOWL: CSE) and Slang Worldwide (SLNG: CSE) were among the week’s worst performers after being amongst the best last week. More out-of-the-money call option trading in all four of these names.

- Acreage Holdings (ACRDF: OTCQX) has been on the top gainers list for two weeks in a row. However, we saw no news to account for the gain.