OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Improved Leverage and Valuation Metrics for Cannabis MSOs

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 09/20/2024

Viridian Capital Chart of the Week: Improved Leverage and Valuation Metrics for Cannabis MSOs

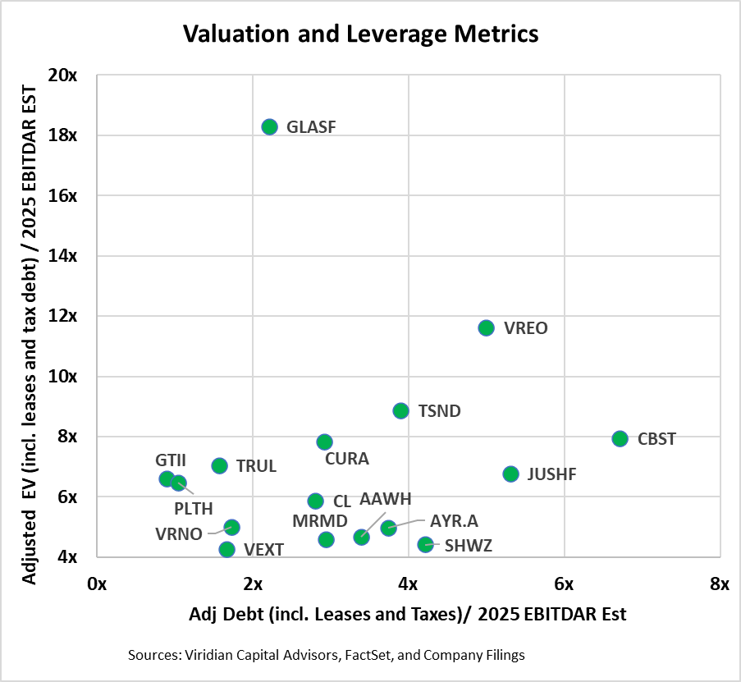

What’s the right way to measure Cannabis company leverage?

- The standard answer is Debt/EBITDA; however, Viridian believes the single best valuation measure is Total Liabilities / Market Cap, which reflects the market’s estimation of the asset value above liabilities. It is immune to accounting manipulations and reacts instantly to news that changes investors’ views of company value.

- Some investors, however, are more comfortable with an accounting-based measure, and Viridian also makes use of these ratios in the Viridian Capital Credit Tracker model. We are in the process of incorporating a new measure into the model utilizing several core principles:

- Leases make up a large portion of the capital of many cannabis companies and should be treated as debt. Lease liabilities make up 82% of combined debt and leases at Planet 13 (PLTH: CSE), 63% at 4Front (FFNT: CSE), 47% at Green Thumb (GTII: CSE) and Ascend (AAWH: OTCQX), and 46% at Curaleaf (CURA: TSX). They represent long-term fixed obligations, often on “mission critical” facilities, and they frequently contain cross-default clauses to other obligations. Defaulting on a lease cannot technically trigger bankruptcy, but there are no bankruptcy protections afforded cannabis companies anyway.

- Cannabis companies have recently been failing to pay their taxes and are basically borrowing money from the government, often at rates that are better than they could get in the market. Viridian considers accrued tax liabilities in excess of one-quarter of tax expense as debt, irrespective of whether the company classifies these liabilities as current or long-term.

- Viridian calculates adjusted net debt by adding leases and excess taxes to total debt before subtracting cash.

- But, since operating lease payments reduce EBITDA, it is not fair to include leases as debt without also adjusting EBITDA. Viridian adds lease expenses to EBITDA to calculate EBITDAR. Since analysts generally do not project forward lease expenses, we annualized the most recent quarterly rent in our estimates.

Shouldn’t the standard EV/EBITDA valuation metric be similarly adjusted?

- Yes, although Viridian calculates these standard ratios as part of our valuation work, we believe a more sophisticated metric is also warranted. We calculate Enterprise Value by adding our adjusted net debt measure to market cap. We then use EBITDA as the denominator in the EV/EBTIDAR ratio.

- The graph shows baseline values for the new leverage and valuation metrics. The inclusion of leases and taxes generally produces higher leverage and valuation metrics. This week’s tracker will investigate some of the relative impacts on both leverage and valuation of these metrics, which we believe are more representative of financial reality.