OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed M&A transactions in the prior week. Our analysis includes:

-

- M&A Market Commentary

- Public and Private Companies

- Buyers & Sellers

- YTD M&A Analysis

- M&A by Industry Sector

- Deal Structure and Valuation Analysis

- Pending Deal Risk Arb Analysis

- Valuation Gap Analysis

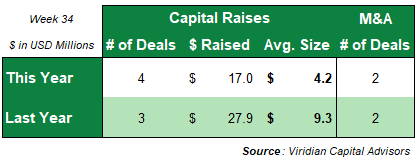

- Two deals closed this week, ended 8/23/24, for a total of $105.0M, compared to two M&A deals closed this week last year.

- YTD, 43 M&A transactions have closed with a total disclosed value of $418.44M, down sharply from the 82 deals for $1,265.90M in 2023. M&A is off to the lowest start of the last six years.

-

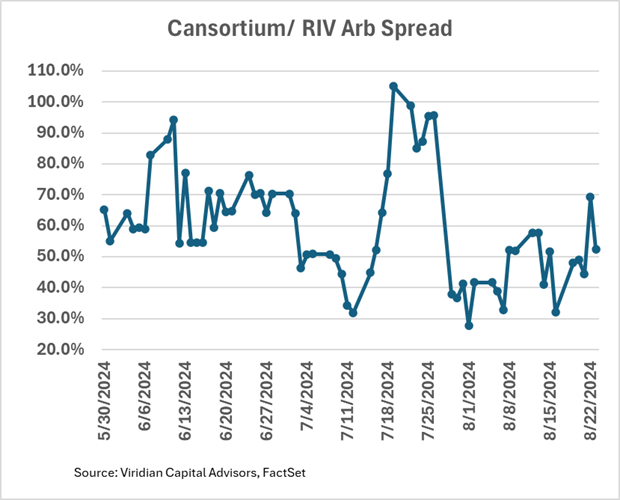

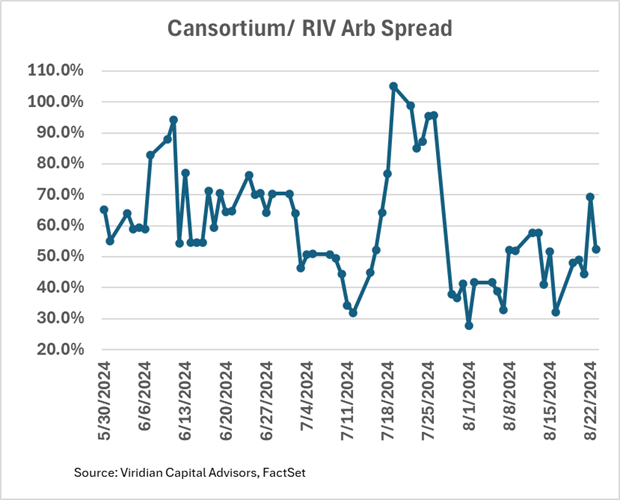

- Cansortium/RIV Arb Spread

- The chart below shows the risk arb spread for the Cansortium/RIV merger announced on May 30, 2024. RIV shareholders are to get 1.245 Cansortium shares for each RIV share owned. The arb ended the week at approximately 52%, a level suggesting only modest confidence about the deal. The company put out a press release this week highlighting the pre-closing integration measures it is taking. However, the news at the end of the week that Cansortium had laid off 50 workers did not engender confidence.

- Shareholder votes on the transaction are coming up soon.

- Cansortium/RIV Arb Spread

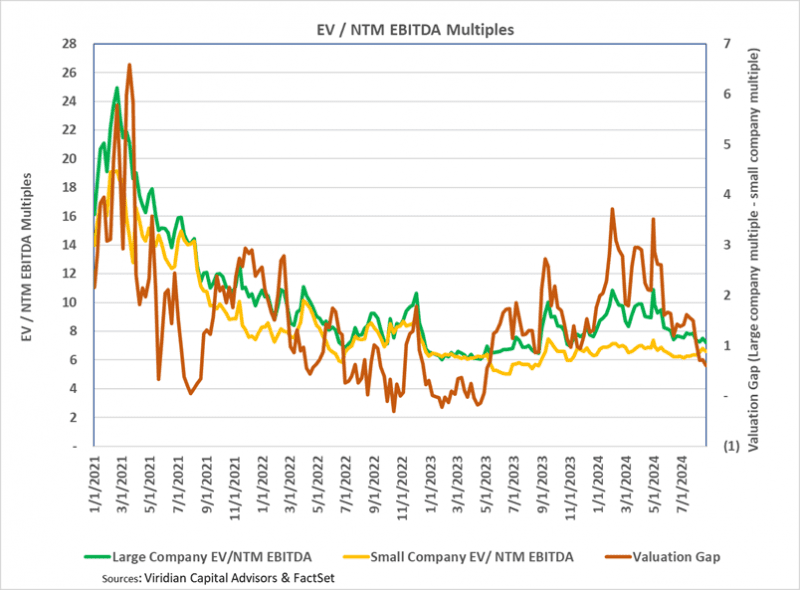

- The Valuation Gap

- The Valuation Gap measures the difference between the EV/ NTM EBITDA multiple for the largest MSOs and the same multiple for the next smaller group. This measure has been a significant driver of M&A activity since a larger gap creates an opportunity for more accretive transactions.

- The companies used in the large-cap index now include Cresco (CL: CSE), Curaleaf (CURA: CSE), Green Thumb (GTII: CSE), TerrAscend (TSND: TSX), Trulieve (TRUL: CSE), and Verano (VRNO: CSE). The small company index now includes Ascend (AAWH: OTCQX), AYR (AYR.A: CSE), Cannabist (CBST: Cboe), Front (FFNT: CSE), Jushi (JUSHF: OTCQX), and Schwazze (SHWX: OTC).

- The gap increased by 10bps to 0.62, the lowest since May 2023. Following the DEA announcement, it reached a recent peak of 3.55 on April 30. At 1.15, the gap indicates that, in the aggregate, the climate is relatively inhospitable for transactions in which Tier 1 MSOs purchase Tier 2 MSOs. This may not be the case for individual combinations, however, as there are broad valuation metric spreads between the companies in each tier. For example, TerrAscend, GTI, and Curaleaf all trade well above the Tier one average, while Ascend trades well below the Tier 2 average.

- Cansortium/RIV Arb Spread

- The chart below shows the risk arb spread for the Cansortium/RIV merger announced on May 30, 2024. RIV shareholders are to get 1.245 Cansortium shares for each RIV share owned. The arb ended the week at approximately 52%, a level suggesting only modest confidence about the deal. The company put out a press release this week highlighting the pre-closing integration measures it is taking. However, the news at the end of the week that Cansortium had laid off 50 workers did not engender confidence.

- Shareholder votes on the transaction are coming up soon.