OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

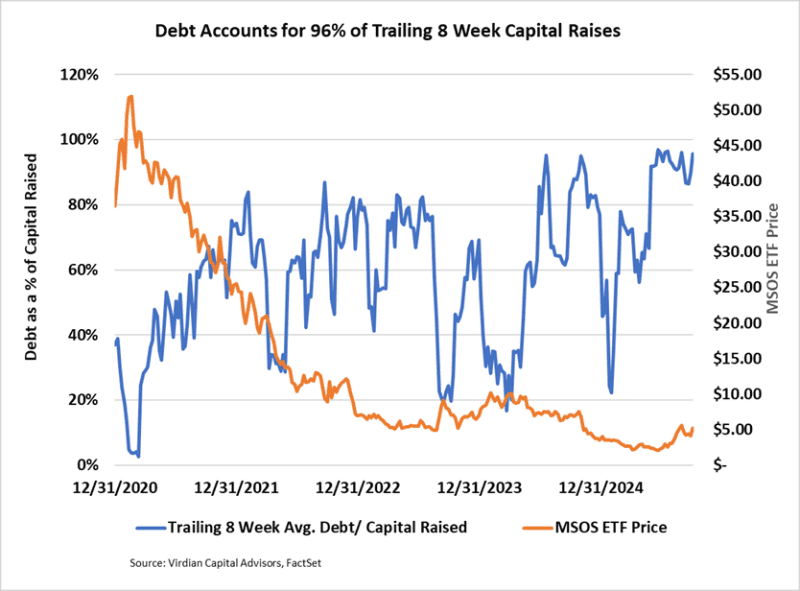

- Debt accounted for 96% of trailing 8-week capital raises. The ratio may increase if companies can utilize favorable regulatory-induced stock price rises to complete equity issues. We believe that a successful move to S3 will increase the likelihood of other near-term regulatory moves, such as the SAFER or STATES. The real question is what kind of price increase will it take before cannabis companies are willing to issue equity? Will the change to S3 result in a lasting price pop that could lead to re-equitization?

- The Week’s Debt Transactions

- On October 1, 2025, Verano Holdings (VRNO: CSE)(VRNOF: OTCQX), the seventh largest U.S. MSO by market cap, closed a $75M credit agreement agented by Chicago Atlantic with participation from a regional bank

- Verano drew down $50 million of the facility at closing to pay down $50 million of its existing, higher-cost facility with no prepayment penalty.

- The new agreement, secured by selected real estate, provides Verano with a revolving credit facility, which is uncommon in the cannabis industry. Typical American companies maintain standby revolver lines as their source of emergency liquidity. Without access to such facilities, cannabis companies must maintain higher-than-optimal levels of cash on their balance sheet, which is clearly suboptimal in a capital-constrained industry.

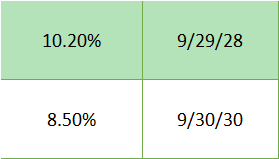

- The facility carries a floating interest rate set at SOFR plus 6% with a 4% SOFR floor. The current rate of 10.2% appears somewhat high in relation to our assessment of Verano’s credit quality; however, the flexibility of this facility, combined with the advantageous prepayment provisions, makes this a solid deal for the company.

- The facility matures on September 29, 2028, and no amortization payments are required during the term.

- The revolver has an interest-only make-whole provision if repayments are made within six months of the funding date. This may be a crucial feature if rescheduling reduces funding costs, as we believe it will.

- On September 30, 2025, Ascend Wellness (AAWH: CSE)(AAWH: OTCQX), the ninth largest U.S. MSO by market cap, closed on a $9.34M mortgage loan with CF Bank on real estate in Cincinnati, Sandusky, and Piqua, Ohio.

- The loan matures in September 2030 and carries an attractive rate of 8.5%—Ascend’s 2029 maturity debt trades at around 12.8%, demonstrating the value of the mortgage financing.

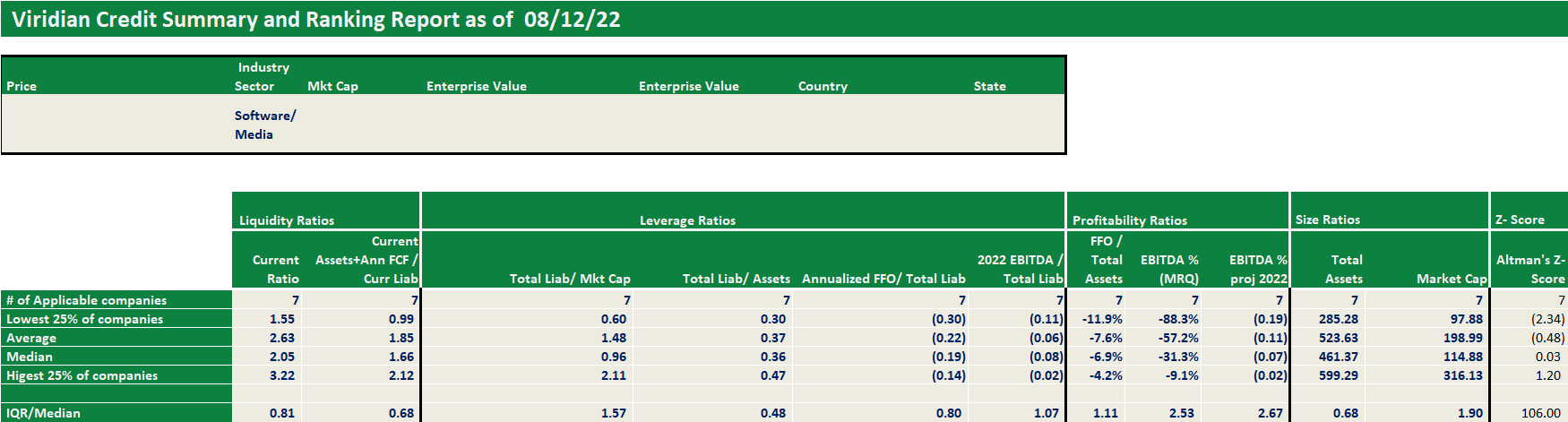

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.