OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

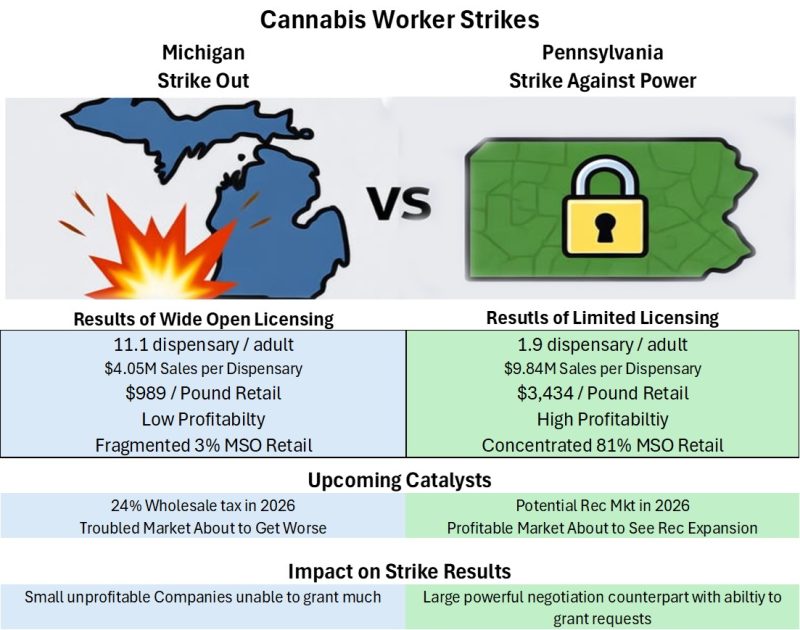

- The ongoing cannabis worker strikes in Michigan and Pennsylvania represent the longest work stoppages in U.S. cannabis history, surpassing a previous 13-day record from 2023.

- In Michigan, four employees at Exclusive Brands have been on strike since August 28 over the company’s refusal to recognize the results of a union election. Despite the operator’s social equity branding, the company remains open, with claims of over 200 workers on the job.

- In Pennsylvania, eight unionized workers at Gren Thumb’s RISE dispensary in York have been on strike since September 1, demanding a starting wage of $18/hour (up from $16-17.65) and better benefits after stalled contract talks.

- It’s hard not to sympathize with the plight of entry-level cannabis workers. Paying for their participation in an industry they are devoted to with low wages and little job security. But these workers are also up against powerful industry forces. The two settings of Michigan and Pennsylvania could not be more different in key ways that impact the strikers’ negotiating power.

- Michigan workers are battling state conditions as much as their employer. Wide-open licensing has led to an explosion in cultivation capacity and the number of stores. Michigan’s 840 dispensaries represent 11.1 stores per 100k adults, higher than any other top ten market except Colorado. Sales per dispensary average only $4M per year, a level that is suboptimal for operating profitability. Market pricing reflects this overcapacity. The average retail price for September 2025 is less than $1,000 per pound. The bottom line is that Michigan operators have limited options; many are struggling to make ends meet. And things might be getting worse; the Michigan legislature has just passed a 24% wholesale tax that, if not reversed, is likely to reduce cross-border traffic to Michigan stores and drive sales back to the illicit market. MSOs are generally absent from the market, and only around 2% of retail stores are now operated by MSOs

- Things could not be more different in Pennsylvania. PA is a tightly regulated medical state with only 191 dispensaries, averaging around $10 million in revenues. Retail prices have decreased slightly, but they remain attractive at around $3,400 per pound. MSOs are more dominant IN PA than in any other state we can point to, with over 81% of the stores operated by MSOs. The state is doing well and looks to gain another bump in revenues and profits if plans to go adult rec materialize. Workers here are striking against power rather than economics. Big MJSOs don’t want to give concessions in PA because they fear they will face similar demands in all their other markets. But it’s not that they couldn’t afford to raise workers’ wages a bit; it’s more that they don’t feel that they need to.

- The cannabis industry is in a strange situation. Their customers are increasingly saying that their budgets are strained, and increasingly, they are hearing that from their own employees.