OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

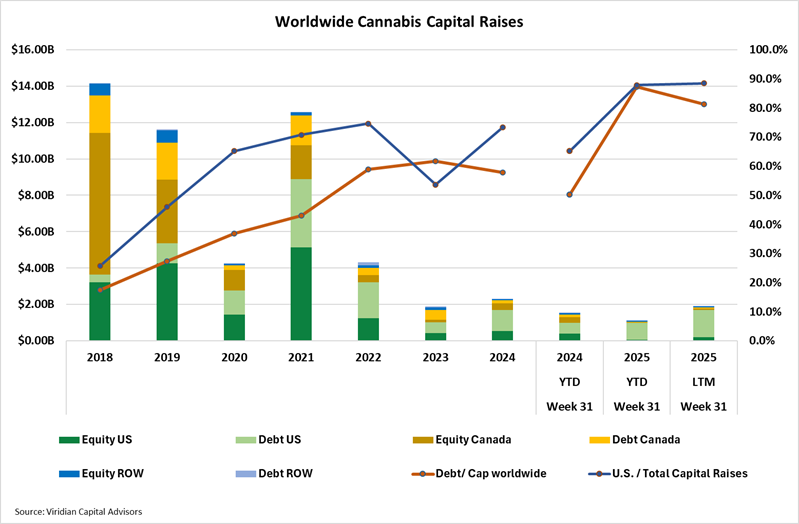

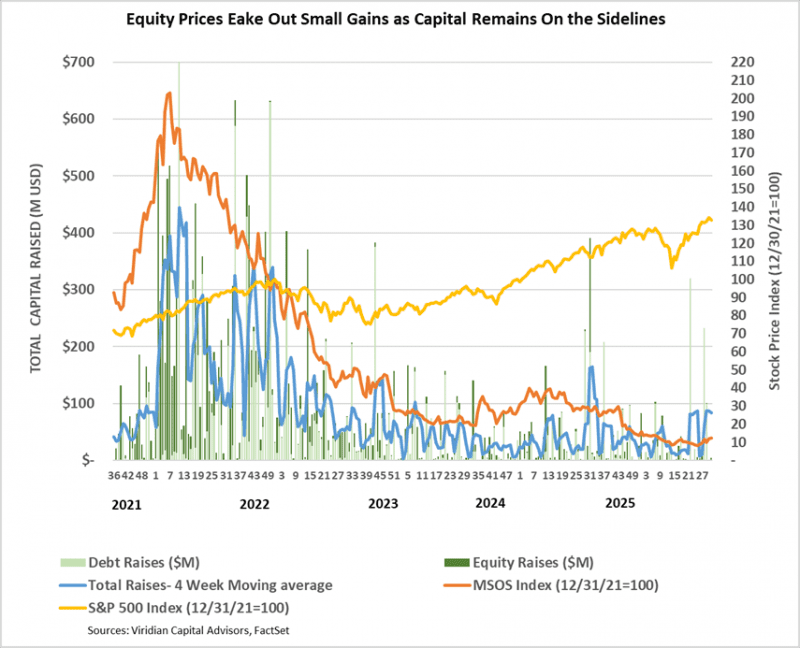

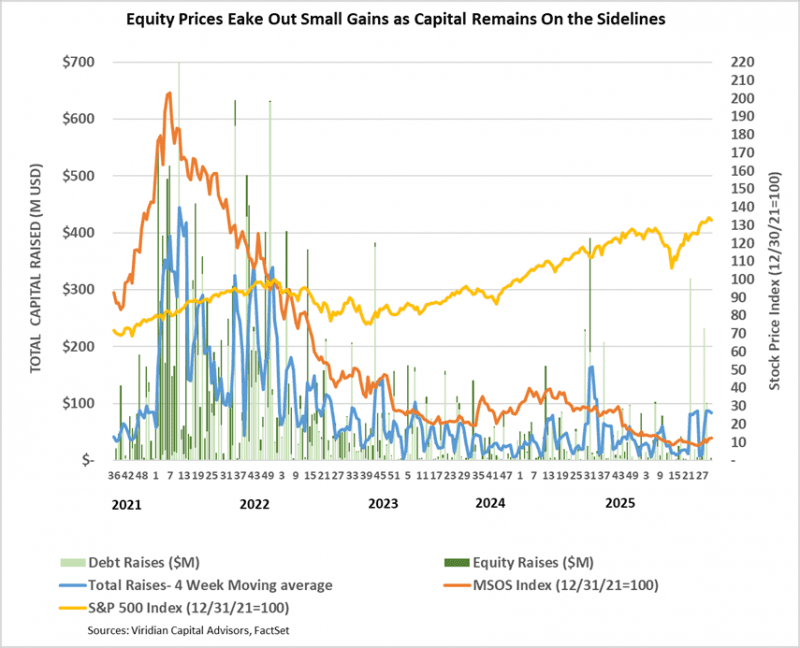

- YTD capital raises totaled $1.11B, down 27.4% from last year’s $1.53B. From an LTM view, capital raises totaled $1.90B, down 18.1% from the same period in 2024. Debt as a percentage of capital raised on a worldwide basis is 87.3%, compared to 50.2% in the previous year. U.S. raises LTM accounted for 88.5% of total funds, up from 20.7% at the same point in 2024. Raises from outside of Canada and the U.S. represented 5.1% of the total funds raised, in line with the average of 5.33% in the six previous years.

- Public company raises accounted for 78.0% of total raises in the LTM period, the highest since 2021.

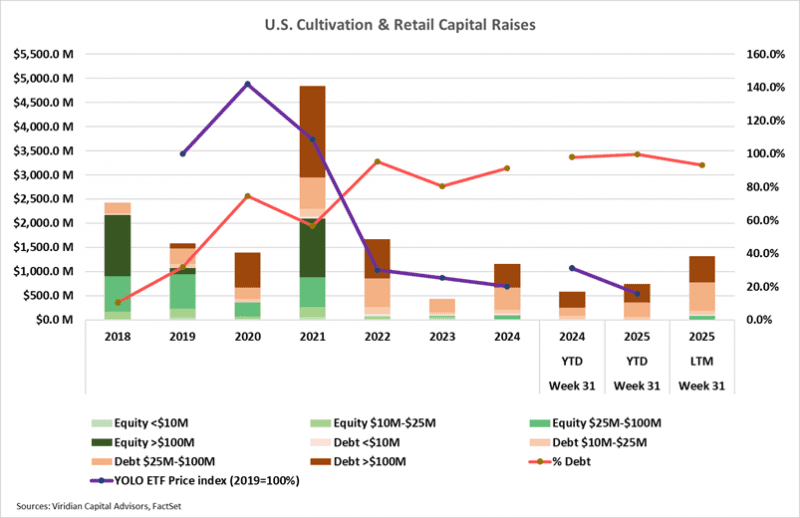

- YTD capital raises for the cultivation and retail sector total $746.2M, up 26.5% from last year’s $589.9M. For the LTM period, the capital raised in the cultivation and retail sector was $1,315.5M, 13.5% higher than in 2024, which in turn was 167% higher than in 2023.

- Debt accounts for 93.3% of the funds raised over the last 12 months (LTM). Large debt issues (over $100M) accounted for 52.3% of capital raised, compared to zero in 2023.

- Cannabis equity prices (as measured by the MSOS ETF) were up 2.59% for the week.

VIRIDIAN INSIGHTS

- NEW YORK – 93 STEPS FORWARD AND 105 BACKWARD?

- New York now has 436 licensed adult-use dispensaries, a gain of 93 since the end of 2024.

- Last week, however, the OCM admitted that it had miscalculated compliance with a law that forbids cannabis dispensaries from being located within 500 feet of a school or place of worship. Sounds simple, but the OCM measured the distance from the entrance of the dispensary to the entrance of the school building, whereas they should have been measuring to the nearest property line of the school or place of worship.

- As a result, 105 granted licenses, including 60 that are operational, were informed that they may need to relocate to comply with the requirements prior to their next license renewal. The ruling also affects an additional 47 pending applicants.

- The state established a $15 million fund, which will offer up to $250,000 to assist with relocation or capital improvements. That amount doesn’t seem nearly enough and may not even cover lease cancellation charges. Another feel-good political measure that doesn’t come close to fixing the problem.

- Will Governor Hochul’s proposal to grandfather the licenses succeed? We hope so, but this is New York, a state that has only very recently begun to get anything right.

- The good news is that if you are up and running and unaffected by the zoning problem, you may have more time to build a competitive moat.

- TEXAS SPECIAL LEGISLATIVE SESSION- THE DIFFICULTY OF HERDING CATS

- We talked a couple of weeks ago about the fact that the two key components of Abbott’s proposals seem sort of reasonable:

- Age Restrictions, including child-resistant packaging, restrictions on sales near schools, and limiting marketing to minors.

- Comprehensive hemp product regulation, including prohibiting synthetic cannabinoids, including D8 & D10, requiring mandatory testing, and limiting potency.

- But it appears that the anti-hemp legislators have grabbed the microphone and have doubled down on House and Senate bills that mirror the original hemp shutdown legislation.

- But just when things seemed dire for the Hemp team, the opposition upped and skipped town to avoid voting on the redistricting proposal.

- It is now unclear whether any hemp legislation will emerge from the special session, or whether Abbott will again veto it if it does.

- One thing is clear, though: Hemp is still under attack, and its opponents do not care how many jobs or how much tax revenue need to be sacrificed to rein it in.

- We talked a couple of weeks ago about the fact that the two key components of Abbott’s proposals seem sort of reasonable:

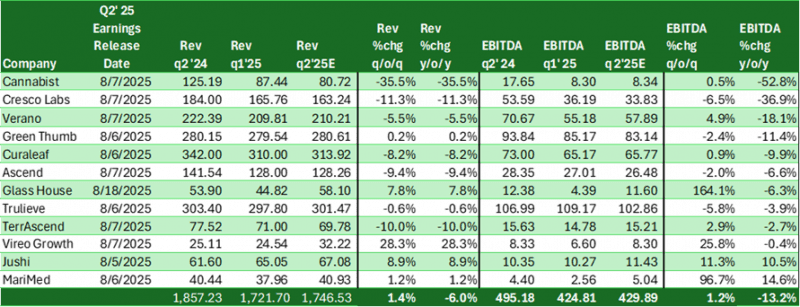

- MOST Q2’25 EARNINGS RELEASES ARE SCHEDULED FOR THIS WEEK.

- The table below (in order of earnings release date) presents updated estimates for revenue and EBITDA (post-coaching). The picture is not pretty: Only two of the twelve companies shown, Jushi (JUSHF: OTCQB) and MariMed (MRMD: CSE), are expected to have higher EBITDA in Q2’25 than in the second quarter of last year. The aggregate EBITDA for the group is expected to be 13.2% below last year’s figure. Note: Jushi reported after the close with a 20.1% EBITDA beat, despite a 3% revenue miss.

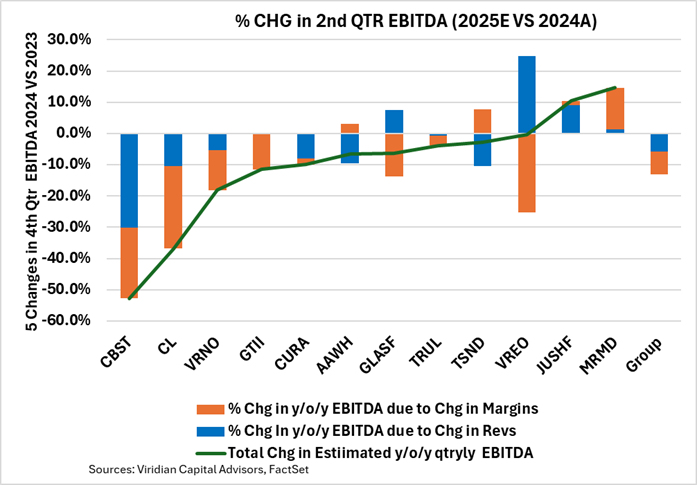

- The chart below the table decomposes the year-over-year percentage change in EBITDA into its components: revenue growth (blue bars) and EBITDA Margin change (orange bars). The aggregate EBITDA decline of 13.2% was composed of a 5.8% portion attributable to lower revenues an

- NO MORE AYR IS LEFT

- On July 30, 2025, Ayr Wellness (AYR.A: CSE)(AYWRF: OTCQX) entered into a Restructuring Support Agreement (RSA). Under the RSA, the company will support an Article 9 UCC sales process commenced by its senior secured noteholders.

- The Noteholders have agreed to purchase, using credit bids, AYR assets in Florida, Ohio, Pennsylvania, Nevada, New Jersey, and Virginia at a consensual public disposition of the Senior Note collateral.

- In exchange for cancellation of the credit bid portion of the Senior Notes, Senior Noteholders will receive their prorated portion of 100% of the new equity. The remaining portion of the Senior Notes not used in the credit bid will remain outstanding and be entitled to a cash distribution from the sale of the company’s remaining assets, which appear to be its Massachusetts, Connecticut, and Illinois properties. Noteholders will have a high incentive to utilize their full positions in credit bids on assets.

- Few details of the auction process have been released; however, the ability to credit bid for assets gives a high incentive for the Senior Noteholders to acquire assets, as they will essentially be bidding with 50 cents on the dollar debt..

- Current equity holders are wiped out in the deal.

- Why not adopt the simpler and arguably less costly plan that we proposed several months ago in this column, which primarily involved using debt-to-equity swaps for approximately $130 million of the Senior notes and utilizing around $30-50 million of asset sales to reduce the debt further? We can think of only a few reasons.

- Pesky minority shareholders left behind. Our plan would have diluted the current equity holders’ ownership to around 10%. We proposed giving them substantial amounts of deeply out-of-the-money warrants, which would have given them some upside upon a big catalyst, such as rescheduling or SAFER. The current plan avoids dealing with them in the future by eliminating them now. The new owners will entirely capture upside catalysts.

- Perhaps the creditor group begrudgingly accepted the fact that it would end up owning a substantial portion of the company’s assets, but wanted the flexibility of only bidding on some of them.

- Perhaps the intent is to avoid public company expenses by keeping the remaining pieces as private companies, and this is facilitated by eliminating the public float.

- At any rate, it is clear that the AYR as we now know it will no longer exist.

- The businesses that remain will only have the $50M bridge note as debt, resulting in well-capitalized entities.

- WHAT HAPPENED TO “IT WILL BE “ONE OF MY FIRST PRIORITIES AFTER TAKING OFFICE?”

- That’s what Cole said about cannabis rescheduling in his April 2025 Senate Judiciary Committee hearing.

- However, after taking office, Cole released a strategic priorities document that completely omitted cannabis rescheduling.

- We hope he is just waiting for marching orders from Trump, but this is cannabis politics, and there are absolutely zero rules.

- We have always thought that Cannabis would be a natural issue for Trump.

- First off, Cannabis is the ultimate in States’ rights issues. The very existence of the industry owes to the willingness of the states to thumb their nose at the federal government. Trump is no anarchist in that regard, but he is still a big supporter of states’ rights

- Next, cannabis reforms can add billions to the economy by fostering job growth, increasing tax revenues, and reducing significant expenses in police, courts, and jails, among others. This goes along well with his pro-business and cost-cutting leanings.

- Promoting Cannabis is consistent with his tough stand on opioids, fentanyl, and drug gangs. Some states, like Utah, have explicitly stated that they believe their medical cannabis program can be the off-ramp for opioid abuse. Trump is skilled enough to make the point that being hard on hard drugs and pro-cannabis are consistent positions.

- Cannabis is an immensely popular issue favored by a strong majority of voters. With midterms coming up fast, Cannabis is an issue that Trump can steal from the Democrats and use to solidify his base.

- Nonetheless, Trump has studiously avoided any direct comment on the matter.

- In the absence of anything definitive, the cannabis rumor mill has shifted into overdrive. The MSOS is up 21% over the last five days on essentially no news. Everyone wants to believe.

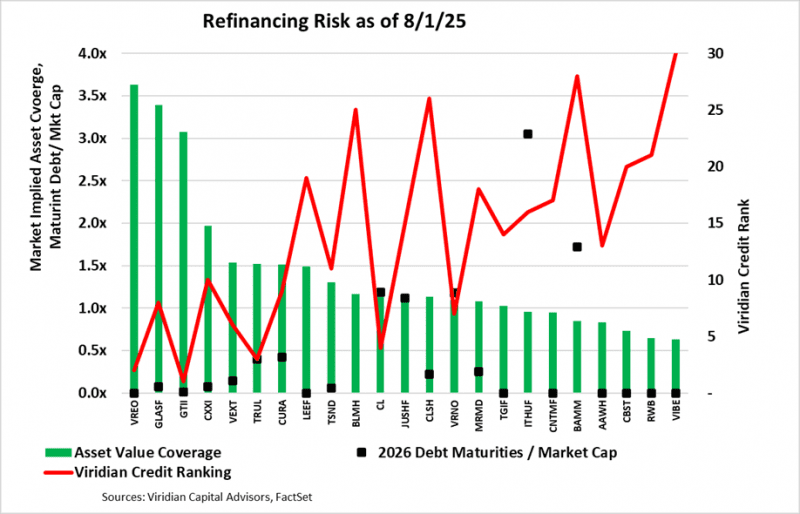

- GAUGING THE RISK OF THE 2026 DEBT MATURITY BUBBLE

- Much has been made of the upcoming wave of cannabis debt maturities in 2026. The sheer size is undoubtedly intimidating. The companies pictured on the graph below collectively have approximately $1.9 billion of debt maturing in 2026. (IAnthus maturities are actually in 6/27, but close enough!). Putting that figure into perspective, $1.9B is greater than the total capital raised for the cultivation & retail sector for any year since 2018, except for 2021.

- Viridian is generally more constructive about the issue than most other industry observers. We observe that in the high-yield bond market, it is virtually never the case that debt is paid off in cash. It is generally refinanced, OR the company is forced to restructure. Obviously, given the lack of prepackaged bankruptcy (or any bankruptcy, for that matter), restructuring is rightfully a prospect to be feared in the Cannabis Industry.

- We note that some of the original problems we discussed back in April at MJUNPACKED have gone away. Cannabist employed a classic ‘amend, extend, and pretend’ tactic, and both 4Front and AYR have gone the other way, facing receiverships or liquidations.

- So, how do we gauge the risk of something going wrong in 2026? Refinancing risk is a peculiar mixture of market psychology and financial realities.

- The green bars show the 8/1/25 market-implied asset coverage of total liabilities. We arrive at this by viewing the equity as a call option on the asset value of the firm, with a strike price equal to its liabilities, and assuming maturities of 2026, as well as volatility of 40% and a risk-free rate of 4.25%. This provides us with all the elements of the Black-Scholes option pricing formula except for the current asset value. By iterating on the solution of the BS model, we can find the market’s assumption for asset value. The importance of this data point should be obvious. For companies with less than 1x asset coverage of liabilities, debt providers are effectively making an equity bet. They do not have adequate asset value coverage to fall back upon.

- The red line represents the Viridian Capital credit ranking, which considers four key credit factors: Liquidity, Leverage, Profitability, and Size. Refinancing will be more difficult for weaker credits (higher numbers). Companies with ranks of under 16 are in the top half of the Viridian-ranked universe of credits.

- The black dots represent the multiple of market cap that the 2026 debt maturities represent. Clearly, the larger the debt maturities relative to the market cap, the more difficult we would expect refinancing to be.

- The seven companies from IAnthus (IAN: OTC) to the right side of this graph represent higher risk. They have less than 1x asset value coverage, generally poor Viridian Credit Ranks, and several, such as IAnthus and Body & Mind, have maturing debt that is a multiple of their market capitalization. Companies in this position represent only about $160M of the maturing debt.

- Conversely, the sixteen companies on the left-hand side of the graph represent lower refinancing risk. They have solid asset coverage, strong Viridian Credit Ranks, and maturing debt that is less than 1.25x times their market capitalization. These companies represent $1.73 billion of the $1.9 billion total (70%), and we believe they should all be able to refinance their maturities without undue hardship. There is always the possibility of an “accident” where negative psychology meets illiquid funding markets, and refinancings that appear favorable on paper fail to materialize.

- However, the bottom line is that the great debt “tsunami” is likely to be a non-event by the time we reach late 2026.

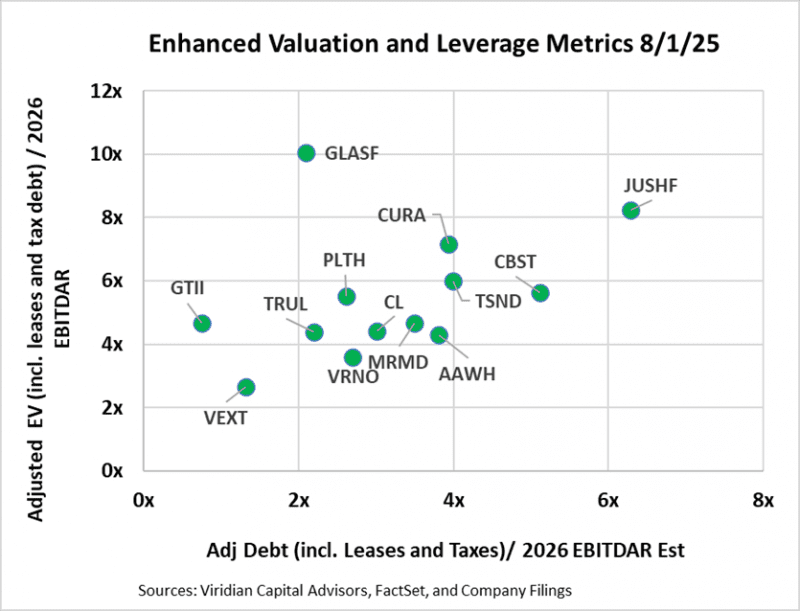

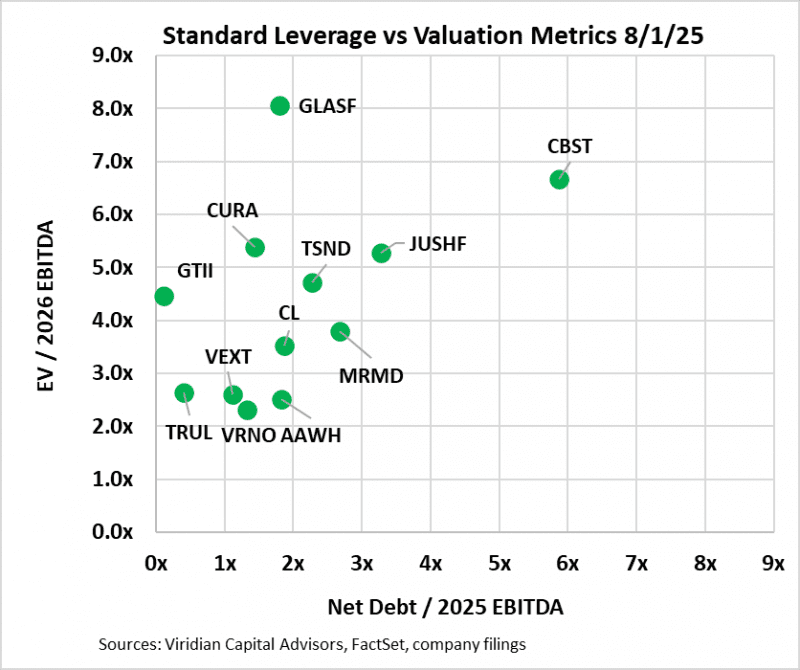

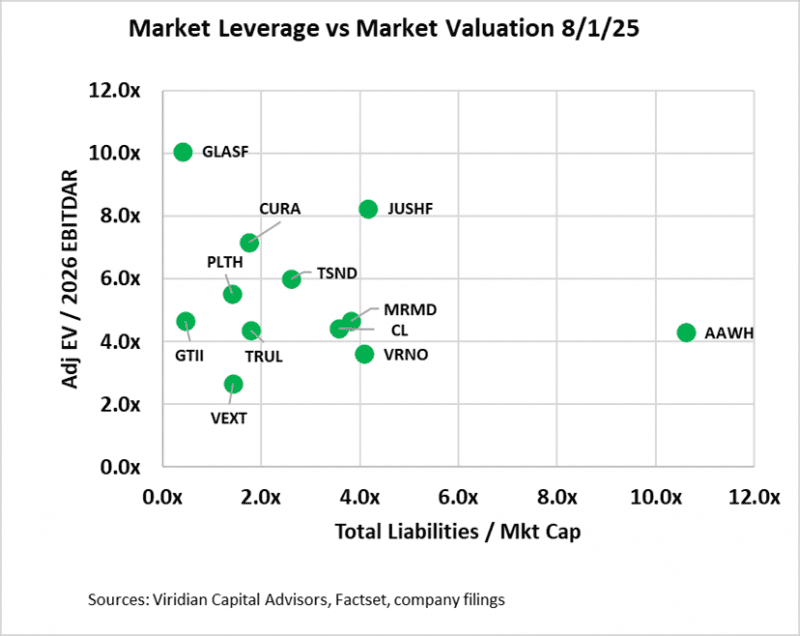

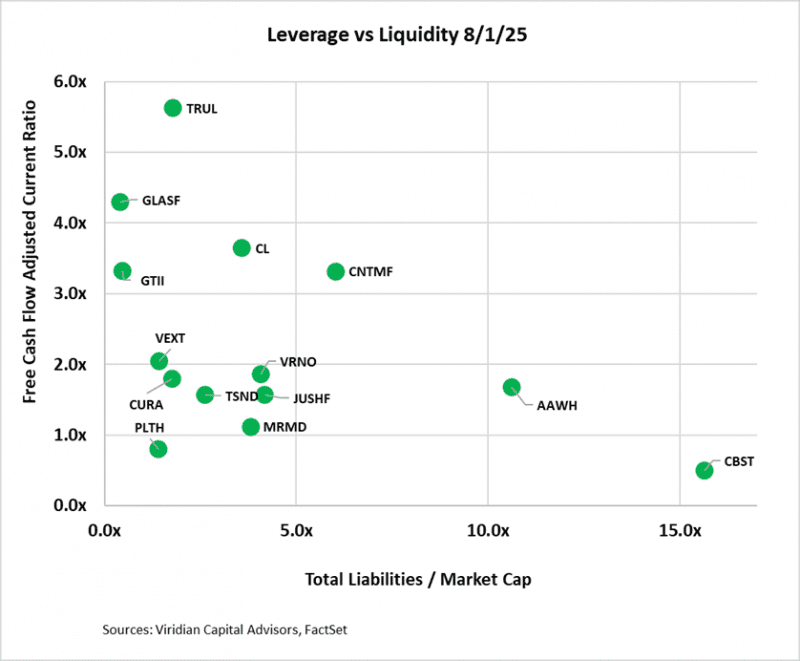

- FOUR KEY GRAPHS THAT SEEK TO MAP THE OPTIONS AVAILABLE TO THE MSOs BASED ON THEIR VALUATION, LEVERAGE, AND LIQUIDITY

- The first two graphs present different versions of EV/EBITDA on the vertical axis and Debt/EBITDA on the horizontal axis.

- The first graph presents our latest view of the most appropriate valuation and financial statement-based leverage metrics: Adjusted Enterprise Value (EV) / 2025 EBITDAR and Adjusted Net Debt / 2025 EBITDAR. In calculating Adjusted Net Debt, we make several key assumptions: 1) Leases that are included on the balance sheet are considered debt. We view most leases in the cannabis space as equivalents to equipment loans or mortgage loans. While it is true that a lease default does not necessarily trigger a cascade of events leading to bankruptcy, the distinction is often meaningless in the Cannabis Industry due to the mission-critical nature of many long-term leases and the absence of bankruptcy protection in This Sector. 2) We consider any accrued taxes (including uncertain tax liability accounts listed as long-term liabilities) in excess of the most recent quarterly tax expense to be debt. Our calculation of enterprise value is now market cap plus debt plus leases plus tax debt minus cash. We now use EBITDAR rather than EBITDA, as lease expense is deducted prior to calculating EBITDA.

- The second graph utilizes EBITDA and employs traditional calculations for both debt and enterprise values, excluding leases and taxes.

- Our adoption of new metrics tends to make the companies look less cheap and more leveraged.

- Surprisingly, nine of the companies on the enhanced metric chart are still above 3x leverage, which we have identified as the boundary of sustainability in a 280e environment. Four companies now exceed 4x leverage, which we believe will be close to the maximum sustainable post-280E.

- Jushi appears as a leverage outlier using the new metrics relative to AYR, which seemed more leveraged using standard measures.

- Glass House is a valuation outlier. We have been positive on Glass House for quite a while, but the multiple spread to the nearest competitor is straining our resolve. We note GLASF’s $25M at the market equity issuance facility as another factor likely to restrain price appreciation. Finally, the unpredictability of the resolution of the matter regarding the recent raids.

- The third graph examines leverage through the lens of total liabilities to market capitalization. We believe this

- The third graph examines leverage through the lens of total liabilities to market capitalization. We believe this is the single best measure of leverage because it is a direct reflection of the market’s assessment of a company’s assets in excess of its liabilities, and it is sensitive to changes in the market’s perception of a company’s future prospects.

- On the bottom left are companies with an Adj. EV/2025 EBITDAR ratio of under 6x and total liabilities to market cap of under 2x. The group includes GTI and Trulieve. Companies in this quadrant are right to consider stock repurchases or using cash in acquisitions. They can afford some additional debt and can take advantage of the ongoing dislocation in equity prices.

- Between 2x and 5x total liabilities to market cap, we find Verano, Curaleaf, Cresco, and MariMed. Verano, Curaleaf, and Cresco all have significant 2026 maturities; however, we do not believe they are likely to face difficulties refinancing their debt.

- On the right lies Jushi and Ascend, both between 6x and 12x, a range that signals stress if not distress.

- AYR, 4Front, Cannabist, and Schwazze are now off the chart to the right, signaling profound credit risk. Our recent work, which utilized option modeling of equity prices, showed that the market believes each of these companies has significantly less asset value than its liabilities.

- The fourth graph introduces the free cash flow adjusted current ratio liquidity measure into the mix. Note that we have recently modified our treatment of this ratio by removing uncertain tax liabilities from current liabilities, where they were previously placed. The result is that no company is currently significantly below 1x free cash flow adjusted current ratio.

- On the top left, we find companies with adequate liquidity and low market leverage, including both GTI and Planet 13.

- Companies in the lower middle-to-right generally have constrained liquidity and high leverage, a potentially dangerous combination in a capital-constrained environment. Five, including Schwazze, Cannabist, Ascend, MariMed, and 4Front. These companies are characterized by high market leverage and low liquidity, making them high-risk. Note: SHWZ, CBST, AYR, and 4Front are now off the chart to the right, with extreme market leverage indicating significant distress.

- VALUATION METRICS SUGGEST STRONG UPSIDE POTENTIAL FROM ANY REGULATORY REFORM, BUT CONTINUING MARKET SKEPTICISM

- Despite recent rallies, cannabis stocks continue to trade at lower multiples than before the HHS announcement. Granted, there are a host of industry-specific problems that extend beyond regulatory reform, including slowing growth, wholesale pricing pressure, and a weary consumer.

- We continue to believe that at current levels, U.S. MSOs have enormous upside potential. We are not Pollyannish about the issues and recognize that the industry faces several deep-seated problems, including competition with Hemp, wholesale price compression, and a reliance on new markets for growth.

- Moreover, we have been “Schumered” a few too many times to buy into the newfound optimism in the market fully. We would rather miss the first 50% gain than get suckered again. We will know it’s real when the big dog speaks. There is more than enough gain to be had; we will be patient.

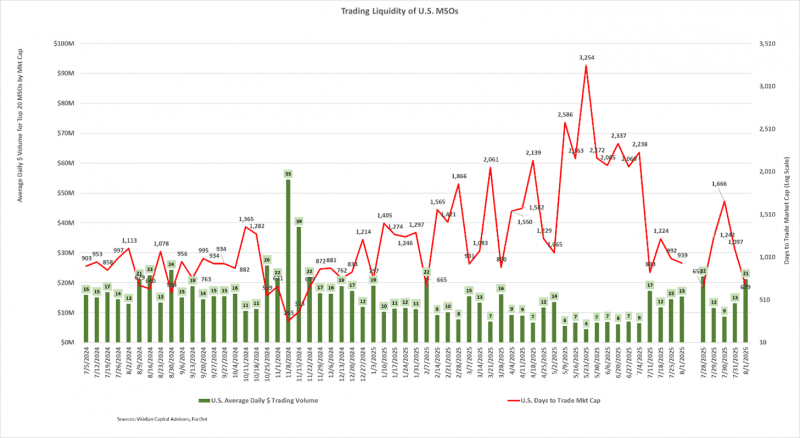

- CANNABIS STOCK VOLUME AND LIQUIDITY REMAIN BETTER THAN ANY PERIOD SINCE FEBRUARY

- The average daily dollar volume of $15 million for the week ending August 1, equalling the reading from last week. Volume continues to run higher than in any 4 weeks since the beginning of the year. The current Days to Trade the Market Cap (DTTMC) of 939 similarly represents a reversal of the downward trend in liquidity that has been in play since the election. A DTTMC of 939 implies that an investor who acquired a 5% position in the stock, assuming they wanted to be less than 25% of the average daily dollar volume, would require 188 days to trade out of their position, a figure that almost seems acceptable only because recent readings have greatly exceeded a year. Will this spike in liquidity continue? We doubt it, but would love to be proven wrong.

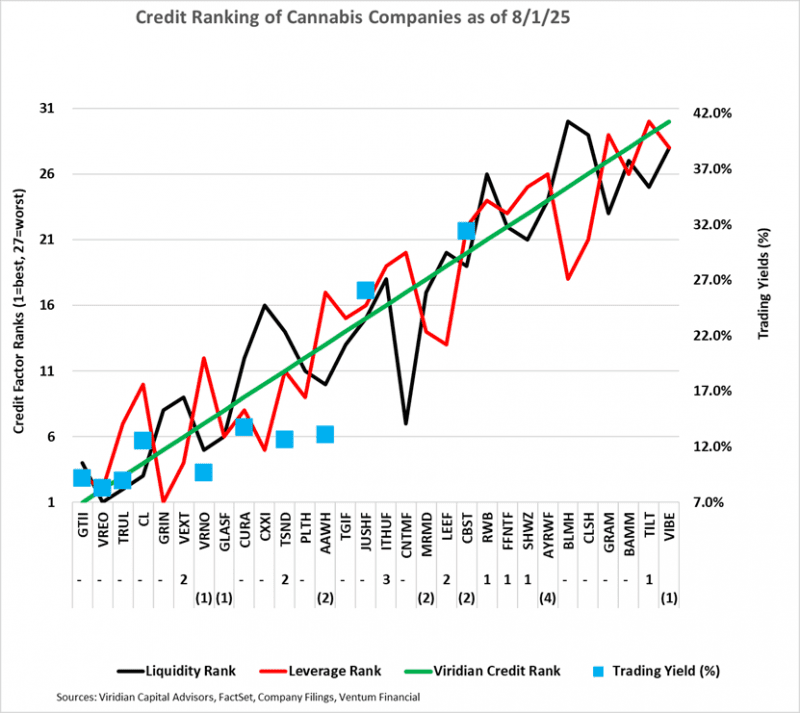

- GIVING CREDIT WHERE CREDIT IS DUE

- The chart below displays our updated credit rankings for 31 U.S. cannabis companies as of August 1, 2025. The number below the ticker symbol indicates the change in credit ranking since last week. A negative number suggests credit deterioration, while a positive number indicates improvement.

- The blue squares show the offered-side trading yields for each Company. Cresco and Curaleaf are both trading at higher yields than their credit quality warrants. This suggests several possible trades: sell Ascend and TerrAscend and buy Curaleaf. Sell Verano and buy Cresco. Each of these trades picks up credit quality and yield.

- Note: We have not seen quotes on the AYR senior notes since the announcement of the restructuring plan, but they were offered at around 50 flat in the previous week. When we adjusted our option modeling to reflect a ½-year to maturity option and a near-zero level stock price, we calculated an asset coverage of around 63%.

- Cannabis equity prices (as measured by the MSOS ETF) were up 2.59% for the week.

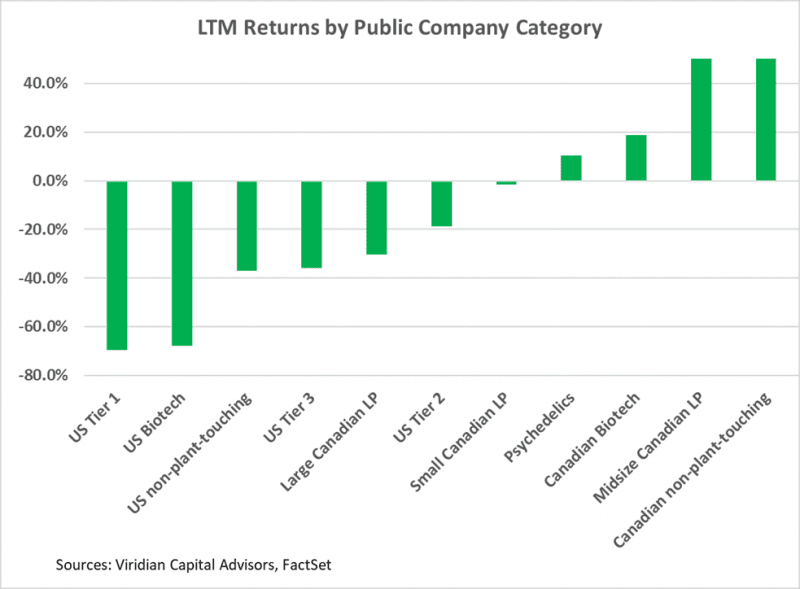

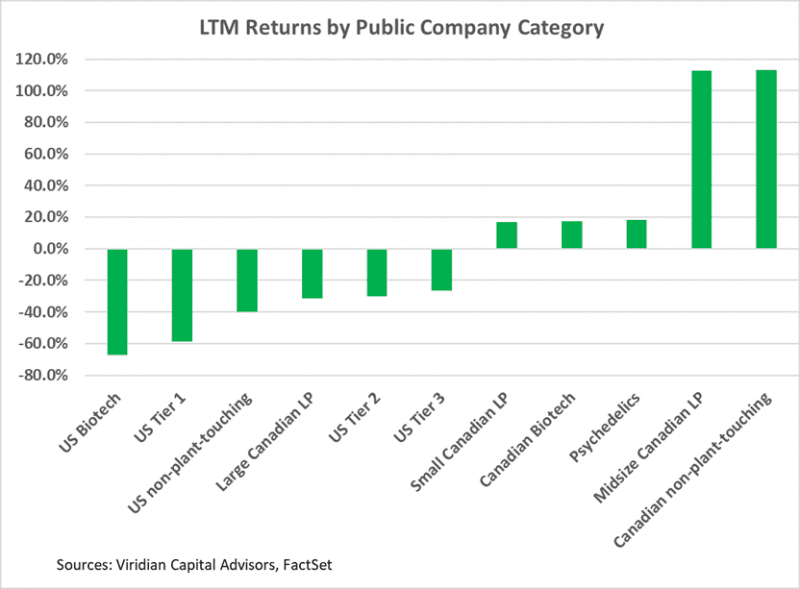

- TRADING RETURNS FOR PUBLIC COMPANIES BY CATEGORY

-

- Plant-touching categories continue to trade at significant LTM losses.

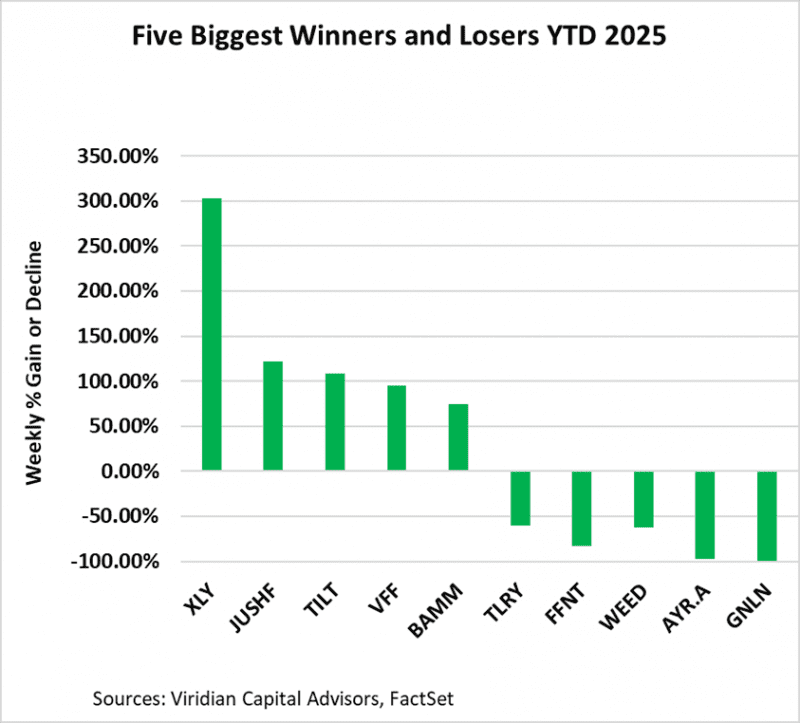

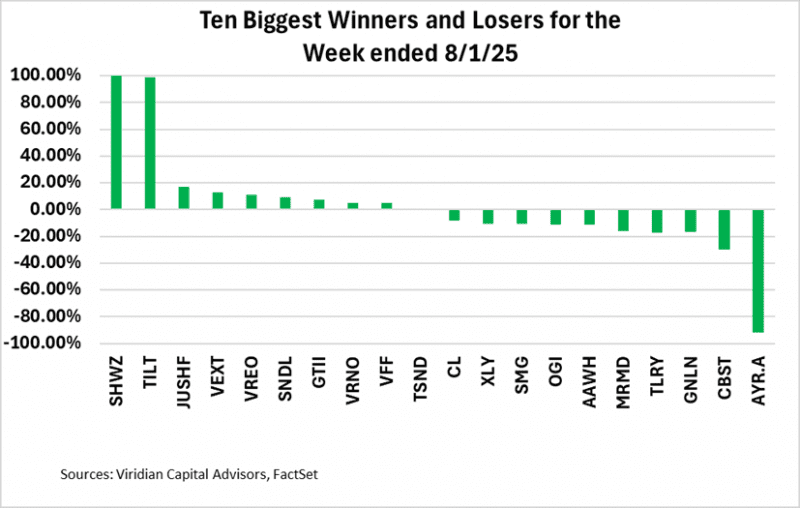

Best and Worst Performers for the week:

- AYR, 4Front, and Schwazze, three companies with significant solvency concerns, continue to exhibit substantial losses in their last 12-month (LTM) stock prices.

- Schwaze and Tilt, two companies trading as out-of-the-money options, were the largest gainers. At the same time, AYR was the biggest loser, with a near wipeout of share value corresponding to the zero recovery in the company’s recently revealed restructuring plan.